Tagged: EPFO

NTH :: Should EPFO subscribers hike their ETF investments?

The whole theme of EPFO providing these choices to increase and reduce equity exposure is a case of duplication of effort and design. Financial experts are advising investors to leverage existing options.

Hiral Thanawala | May 02, 2018 11:28 AM IST | Source: Moneycontrol.com

There is good news for over five crore subscribers of retirement fund body EPFO. Soon they may have an option to increase or decrease investments of their provident fund into stocks through exchange-traded funds (ETFs) in the current fiscal. In its last meeting, the Central Board of Trustees decided to explore the possibility of granting an option to increase or reduce equity allocation to subscribers contributing through ETF above the 15% cap.

The Employee Provident Fund Organisation (EPFO) had started investing in ETFs from investible deposits in August 2015. In FY16, it invested five percent of its investible deposits, which was subsequently increased to 10 percent in FY17 and 15 percent in FY18. However, subscribers were not at all pleased with this increase in exposure to equities. There were some who didn’t want to risk their retirement corpus built through the EPF route. While other subscribers were keen to increase exposure to equities for better returns in the long-term.

So, what advice do financial experts have for EPFO subscribers looking to increase their exposure to equities through the ETFs route when the option is opened up?

Who should increase or reduce investments in ETFs?

Several investors are not reasonably patient with their active investments and panic when they see volatility in the market. Chenthil Iyer, a Sebi registered investment adviser and author of ‘Everyone Has an Eye on Your Wallet! Do You?’ said these investors generally invest only in fixed deposits and post office schemes. “For such investors, increasing the equity exposure through EPF route may be a good option as it is a passive mode of investing and ensures a long-term commitment.”

For investors who manage their active investments and have a well-diversified portfolio, Iyer recommends a minimum equity exposure.

Arvind Laddha, Deputy CEO, JLT, Independent Insurance, has a word of caution. “In the past, there have been negative returns for consecutive two-to-three years or even more from equity markets and this could compromise the savings of EPFO subscribers which they are not used to.”

As not all investors understand the risk of equities and their volatile nature of returns, Kalpesh Mehta, Partner at Deloitte India, feels an investor should also consider one’s age, risk appetite, financial obligations and total net worth before increasing exposure to equities through ETFs.

Benefits of increasing investments in ETFs

Here are the benefits of increasing investments in ETFs through EPF contribution as explained by Amit Gopal, Senior Vice President, India Life Capital: 1) Regular monthly SIP because of mandatory contributions; 2) Inexpensive as employees (contributors) don’t have to pay fund management fees in the current model of EPF; and 3) Tax advantages on contributions. To this, Colonel Sanjeev Govila, CEO, Hum Fauji Initiatives lists institutional framework taking care of selection and research of equities while investing.

Drawbacks of increasing investments in ETFs

Gopal highlights drawbacks such as insufficient administrative track record, illiquidity associated with a retirement fund product, absence of choice in fund manager and products.

To this, Iyer cautions, “Putting the responsibility of equity exposure of this fund on the individual may expose it to the vagaries of the individual’s risk perception, leading to possible over-exposure.”

Make EPF more investor friendly

EPF needs to be investor friendly with additional facilities of enhancing and reducing equity allocation which is likely to be made available in the coming two-to-three months. Iyer feels periodic electronic statements should be mailed to the subscribers which clearly mentions the amount and number of units available in ETF.

“Further an automatic mode of distributing the contribution into equity and debt should be made available based on the age of the individual just like NPS.” This, he feels, will ensure minimum manual intervention in decision-making with regard to equity exposure.

According to Goyal, while EPFO have described some methods of passing on returns, nothing concrete has been implemented. “It is unclear how they will ford the system and governance challenges that could arise.”

It would therefore be good if these issues are resolved before increased allocation and employee choices are implemented. An investor needs to keep a track of this developments for their own benefit.

Leverage on existing options instead of duplicating efforts

The whole theme of EPFO providing these choices to increase and reduce equity exposure is a case of duplication of effort and design. Financial experts are advising investors to leverage existing options.

“The NPS already provides the same structure and benefit. Integrating it with the EPFO and permitting portability is a more efficient way of enhancing employee choice. NPS already has the architecture and track record of administering an employee choice model,” Gopal added.

Source: https://bit.ly/2IdyOMu

ATM :: Planning to invest in home? Here is how you can raise your down payment

With interest rate-cuts and increased liquidity with banks following the demonetisation, loan products have more accessible.

Adhil Shetty | Published: May 11, 2017 4:02 PM | Financial Express

Consumers with healthy credit scores today would be receiving loan offers aplenty. With interest rate-cuts and increased liquidity with banks following the demonetisation, loan products have more accessible. Yet availing a home loan for the very first time remains a complex experience that loan seekers view with trepidation.

There are often misconceptions about what a home loan can do, and what it costs. For instance, you may be of the belief that the loan granted will match the property price. That is untrue, as financial establishments expect you to pay the margin amount.

The margin amount is another term for down payment for your new home. It could be anything between 15% and 20% of the home’s net value. For a first time home buyer, it is no easy task raising this money.

Here are some ways to help.

1. Strategic savings

Nothing beats strategic savings and for this you need to start your planning early. It involves you visualizing your long-term fund needs—including the need to buy a home—and beginning to save and invest accordingly. Begin with simple and accessible investment tools such as mutual funds or recurring deposits. Slowly and surely, you’ll be able to build your deposit over time. You can be efficient at this by locking in your savings at the start of the month. The earlier you start, the sooner you build this fund for your down payment.

2. Take loans but exercise restraint

There could be a situation where you are in urgent need of funds for the down payment. You could consider taking a personal loan to meet the need. Yet, you need to do this in a controlled manner. Having an existing loan will reduce your ability to take on, and repay, additional loans such as a home loan. You would find your finances stretched as you attempt to pay two EMIs at once. This isn’t an ideal situation to be in and is recipe for a financial disaster, in case you were to temporarily lose your ability to generate income. Therefore any loans for down payments need to be taken thoughtfully, and settled as soon as possible to reduce monthly EMI liabilities.

3. Mortgage another property

If you are confident that your current income can take care of EMIs of more than one loan, you could consider a loan against property. You can claim this loan against several options. For example, an existing property or home could be mortgaged. You could also claim it against assets such as shares, jewelry, PPF account, and LIC policies. There also exists the option of taking a loan against rent.

4. Withdraw from your PF account

As per the new EPFO norms, you are now allowed to withdraw up to 90% of your EPF corpus. Not just that, you could also withdraw from this corpus to pay for your EMIs. This scheme was recently implemented keeping in line with the Housing For All initiative of the central government. A word of caution: your PF corpus is meant to help you generate a pension income in retirement, so if you intend to redeem it for a property purchase, you must replenish it soon, or create a backup pension fund to meet your future needs.

5. Deferred down payment

You have the option of requesting a deferred down payment when purchasing a house from a well-known property developer. Under this, you will have the choice of dividing the down payment into multiple instalments. These instalments can be paid over a jointly agreed period of time. Let us say that you have to make a down payment of Rs. 10 lakh. Ask the builder for a time frame of five months to pay Rs. 2 lakh per month.

6. Liquidate your investments

Before you decide to make a property purchase, take stock of your savings, investments and assets. Anything from a vehicle to a part of a property you own can be liquidated for a down payment. Bank deposits, gold, mutual funds, shares etc. can be disposed. This should be carefully done so as to not disturb other financial objectives.

7. Approach an NBFC/ HFC

Non-Banking Financial Companies (NBFCs) and House Finance Companies (HFCs) provide loans that can help you cover a larger part of your fund requirement. For example, they may provide a loan to cover your registration and home repair costs as well. The entitlement of the loan, of course, will be calculated on the basis of your ability to repay.

Always remember to not act in a hurry. Think long and wise about the route you are taking to raise the down payment for your house. It is also advisable to wait and let an offer go if you cannot make the down payment, as there will always be another good offer in the future.

(The writer is CEO, BankBazaar.com)

Source : https://goo.gl/8ixiEW

ATM :: How to withdraw 90% of your provident fund to buy a house

May 12, 2017 | 11:39 IST | SOURCE : Economic Times | Retrieved from Timesnow.tv

In an effort to make its ‘Housing for all by 2022’ a success, the government has allowed for EPFO members to withdraw up to 90 percent of their provident fund (PF) accumulations to make down payments to purchase a house and to pay housing loan EMIs.

Pre-requisites for PF withdrawal

In order to dip into the provident fund saving, the new rule highlights that the PF holder will only be eligible if he/she has been a contributing PF member for at least 3 years, and is buying property in a registered housing society that has at least 10 members.

Further, the property has to be purchased in the member’s name and cannot be purchased jointly with anybody else, except your spouse.

How the money can be used

The money withdrawn can only be used for an outright purchase, as a down payment for a home loan, for buying plots or for the construction of a house. The transactions can be made through central government, state government and even from a private builder, including promoters or developers.

Can the money be used to buy resale flats as well?

Unfortunately no, EPFO will only make payments directly to a cooperative society, the state government, central government, or any housing agency under any housing scheme, or any promoter or builder, in one or more installments. The rule will not apply to real estate purchases in the secondary market or resale transactions.

Can you withdraw both employee and employer contribution?

An EPFO member can withdraw his own share of PF contribution plus interest as well as the employer’s share of contribution plus interest.

Can you EMI payment through PF?

A PF member can use his PF contribution to pay full or part EMIs for a home loan taken in the member’s name. The EMI will be directly paid by EPFO to the government, housing agency or the bank.

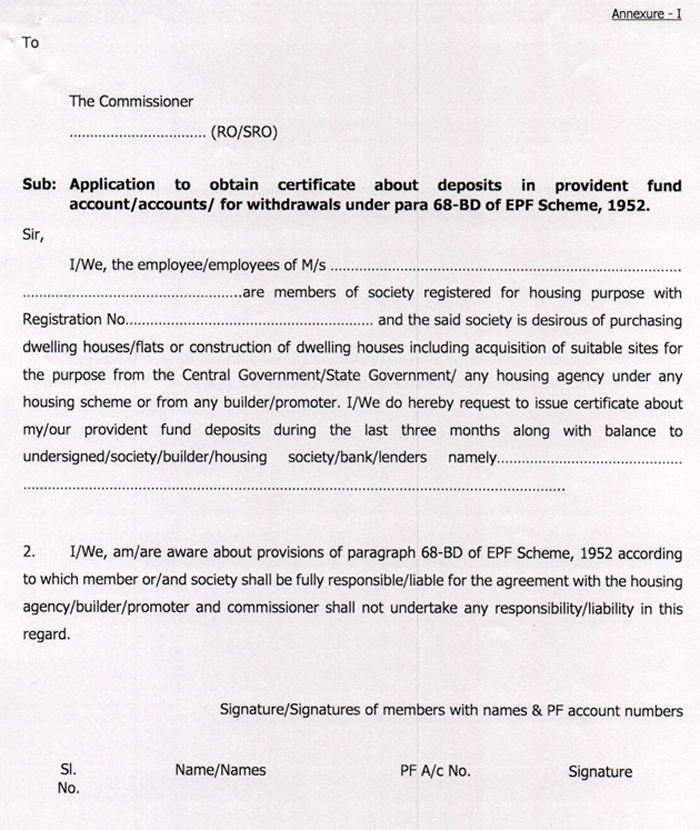

How to apply

A PF member can apply individually or jointly through a housing society to get a certificate from the EPFO.

Through Annexure I form, an employee can ask for the balance and the deposits made in the last three months before applying. This will help the EPFO determine how much EMI can be arrived at.

Also, the employee has to mention the name and details of the bank or housing society to whom such certificate is to be issued.

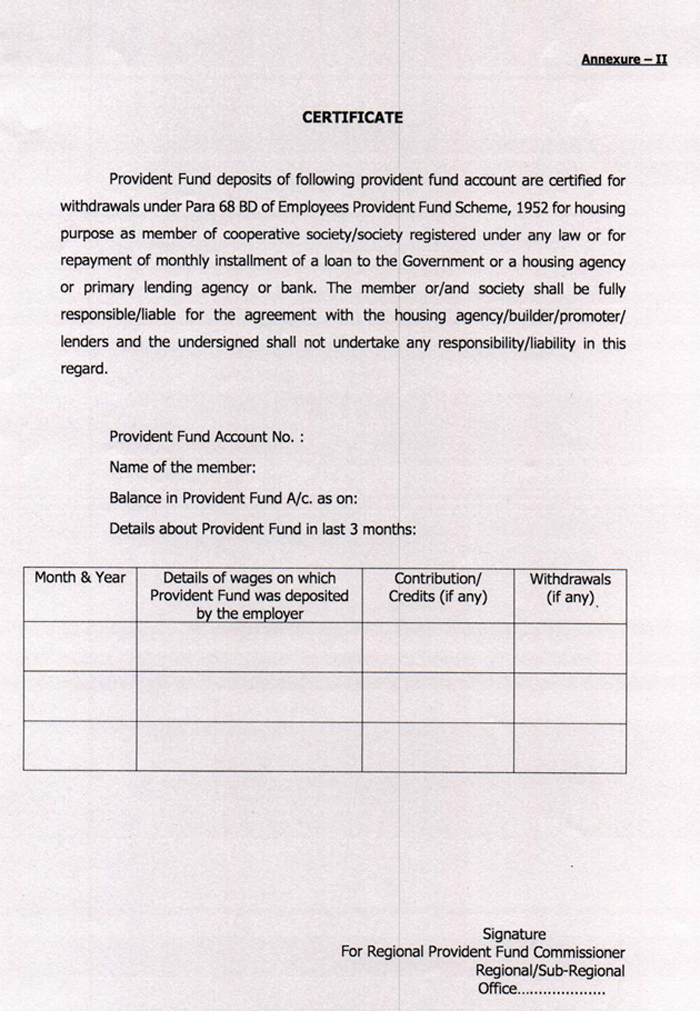

The EPFO then issues a certificate showing the outstanding balance and last three month’s deposit in the account. Alternatively, members can take printouts of their PF passbook downloaded from the EPFO website and submit it to housing agencies or banks.

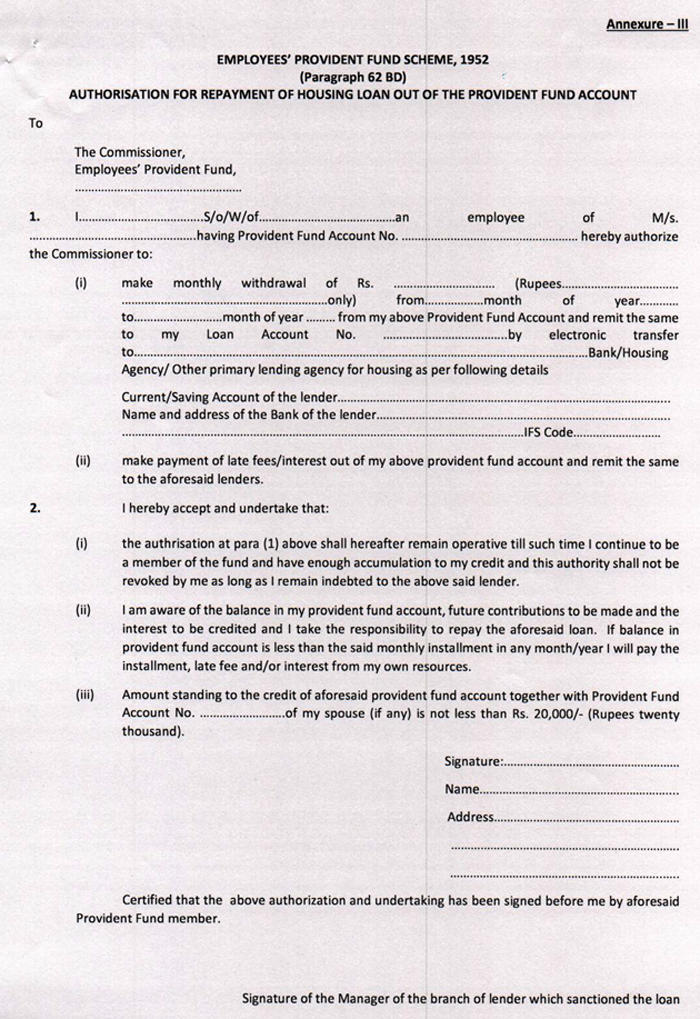

If a member wishes to use PF money to meet EMI’s, then in addition to Annexure I, an authorisation by the member is to be filled in a prescribed format. It will carry details such as PF amount, PF and loan account number, lender name, address etc. One has to get this form authorised from the lender i.e. branch manager of the lender who has sanctioned the loan. Once approved, EPFO will start transferring EMI’s online to the lender’s account.

What if an employee leaves his/her job?

The EPFO has made it clear that under no circumstances would it be liable for any default of payments to the lender. The EPFO will not be party to any agreement made between an EPFO member and a society or builder.

In case a member quits his job, the responsibility of repaying the loan would rest with the employee and not the EPFO.

Conclusion

While dipping into your PF account to make a down payment makes your life easier, it is important to remember, your PF is meant to take care of your post retirement needs, and depleting it may jeopardise your retirement.

So make sure you have a backup plan to meet postretirement needs through equity mutual funds or PPF.

Source: https://goo.gl/egUXjH

NTH :: Should you withdraw 90% from EPF account or take a home loan for buying your dream home?

The government has decided to allow Employees’ Provident Fund Organization (EPFO) subscribers to withdraw up to 90% from their EPF account for the purpose of purchase and construction of their homes. However, would it be a wise decision to withdraw money from your EPF account to buy a home or availing a home loan would be a better option?

By: Sanjeev Sinha | Updated: March 17, 2017 5:02 PM | The Financial Express

The government has decided to allow Employees’ Provident Fund Organization (EPFO) subscribers to withdraw up to 90% from their EPF account for the purpose of purchase and construction of their homes. However, would it be a wise decision to withdraw money from your EPF account to buy a home or availing a home loan would be a better option?

Experts say that buying your first home is rarely an easy task. Now the amendments to the EPFO suggested by the government would certainly allow more individuals to raise the funds needed for their home purchase. In that sense, it is a welcome move since it allows EPFO members access to their own funds in order to achieve a vital financial objective.

However, allowing the EPFO subscribers to withdraw up to 90% from their EPF account for the purpose of purchase and construction of their homes has its share of merits and demerits. “The use of EPF to fulfill these purposes would depend upon the quantum of provident fund deposits which would have accumulated over the years. Buying or constructing a home would require a lot of cash to be spent on as the costs to undertake the said activities can be very high. So, you must check how much EPF balance you have,” says Rishi Mehra, CEO of Wishfin.com.

On the basis of the balance, you can take a calculative decision. If the balance is on the higher side, say in lakhs, and you have more than a decade of the professional journey left before the retirement, you can use the reserve. But make sure not to consume the entire 90% as you can have a challenging post-retirement life to live.

For instance, if 70% of the retirement corpus is sufficient to buy or construct a house, you should consume only 20%-30% and opt for an attractive home loan deal to pay the remaining amount as required to buy or construct a house. This will allow the unused portion of the EPF balance to accumulate and enable you to lead a comfortable life post-retirement besides having a home.

However, “if 20%-30% of the EPF reserves is enough to serve your purpose of home buy or construction, then you can avoid paying the interest that comes with a home loan offered by the banks and housing finance companies (HFCs). If that is not the case, you can either avail a home loan or use both EPF and home loan. The latter option can reduce the interest liability to a considerable degree,” says Mehra.

For example, you have a PF balance of Rs 12 lakh and require a sum of Rs 20 lakh to pay to the property dealer to buy a house. You can then take out Rs 2.5 lakh-Rs 4 lakh from the PF deposits and avail a home loan of Rs 16 lakh-Rs 17.5 lakh. Now, look at the savings you could have using both deposits and loan over the option of loan alone through the calculation in the below table.

In the table, you can see the saving of Rs 2,250-3,599, Rs 2,89,836-4,63,737 and Rs 5,39,837-8,63,737, in EMI, interest payout and the overall payment, respectively, by preferring the combined option of PF and home loan over home loan only.

Pros of EPF Option

# It allows you to buy or construct a home without or paying a lower amount of interest.

# Beneficial for those who need few bucks to fulfill the purpose of buying or constructing a home.

Cons of EPF Option

# Retirement corpus gets used up for an expensive deal of home buy & construction.

# You are left with a very little or virtually nothing to enjoy post-retirement.

# Availing the PF option without having other savings could prove doomsday for your financial health.

Who Should Avail EPF & Who Should Avoid?

As far as who should use the provident fund deposit and who should avoid would depend upon the overall EPF contribution, the financial state and the goals of an individual. “Retirees, who have a huge bulk of EPF balance even after using a portion of the same for a home deal, would like this option. But for some who are in the middle of their professional life can’t go solely with the EPF option. These individuals would have to avail a home loan alongside EPF to find the key to their dream home. With this, they can enjoy an affordable home loan journey while securing their future at the same time. Newcomers would have to wait for a fair length of time before they can think of using the EPF for the home purpose,” says Mehra.

You should also note that the EPF’s primary purpose is to ensure income in retirement for its members. If you withdraw from this fund, you’ll miss out on the benefits of the great returns EPFO provides along with compounded growth over the long term. You’ll then have to find another way to regenerate your retirement fund, which is a challenging proposition. Also, “if you have a large EPF corpus, you can let it earn a handsome 8.65% per annum at the moment (with the possibility of earning higher in the years to come), and take a home loan which you can avail at interest rates around 8.6%. Taking a home loan also allows you additional tax savings through principal and interest repayments up to Rs. 350,000 per annum,” says Adhil Shetty, CEO, BankBazaar.com.

However, if we look at the development thoroughly, the government is also looking to allow EPFO subscribers to use their PF deposits as a mean to repay the home loan EMIs. Well, “to ensure you save for the future and at the same time reduce your interest liability, you should partly use the PF deposits towards the payment of the home loan EMI. The option of paying the EMIs partly through PF deposit could appeal to the most,” informs Mehra.

Source: https://goo.gl/hH2F5v

NTH :: EPFO may invest up to 15% of investable amount in equity markets

Sun, 19 Mar 2017-12:14pm | PTI | DNA India

Buoyed by the surging stock markets, the Employees Provident Fund Organisation (EPFO) may propose to invest up to 15 per cent of its investable amount in equity markets during the next fiscal, Union Labour Minister Bandaru Dattatreya said.

“We are proposing to invest up to 15 per cent during the next year. Central Board of Trustees (CBT) meeting will be held on March 30. We will seek its opinion. So far, during the past one-and-half year we have invested Rs 18,069 crore. We are getting good yield. It is encouraging,” Dattatreya told

Source: https://goo.gl/xcxAk6

NTH :: Centre to invest more PF money in equities

SPECIAL CORRESPONDENT | Updated: July 9, 2016 00:13 IST | Hindu Business Line

The Employees Provident Fund Organisation (EPFO) has earned 7.45 per cent returns from its equity investments since August last year due to an uptick in the capital market, Union Labour Minister Bandaru Dattatreya said.

A status report on equity investments has been sent to financial, investment and audit committee of EPFO and a final call on increasing equity investments will be taken in the next central board of trustees meeting to be held later this month.

“World over, the investments in exchange traded funds are going up. The investment in exchange traded funds will benefit in the longer run and lead to an increase in the rate of return we offer to our subscribers,” Mr. Dattatreya said at a press conference after the 213 Central Board of Trustees (CBT) meeting of the EPFO. He said the EPFO has invested around Rs.7,000 crore in exchange traded funds since August 2015.

Labour Secretary Shankar Aggarwal said the yield on investment in equity till date is “almost equal” to return on government securities investment. “Soon, we will take a decision on how much the equity investments should be increased,” the labour minister, who is also the Chairman of the CBT, said. He said a special CBT meeting may be held between 18 and 22 July to discuss the various proposals including increasing equity investments.

The EPFO started investing five per cent of its corpus in equities beginning August last year. It can invest up to 15 per cent in equity and its related instruments such as exchange traded funds.

Trade unions were not in favour of equity investment as they feared higher risk being involved due to market fluctuations. “We should not look at fluctuations. Ultimately, the interest rate in the long-term will be gainful. We are keeping the workers’ interest in mind but we are not going ahead in a hurry. We are moving forward cautiously,” Mr. Dattatreya said.

UTI to manage equity

UTI will manage the equity investments of Employees’ Provident Fund Organisation (EPFO) along with State Bank of India (SBI), Central Provident Fund Commissioner VP Joy said.

“We have decided to rope in UTI to manage our exchange traded fund investments along with SBI. We have not yet taken a final call on the proportion of funds that each of them will handle,” Mr. Joy said. The finance investment and audit committee of EPFO had proposed that UTI Mutual Fund be allocated 10 per cent of total ETF investments of EPFO and the rest 90 per cent be handled by SBI Mutual Fund.

The asset management companies in the race were: HDFC Mutual Fund, ICICI Prudent Mutual Fund, Reliance Mutual Fund, UTI Mutual Fund, SBI Mutual Fund and Kotak Mahindra Mutual Fund.

“Considering the fact that ETFs as an investment vehicle are relatively nascent in the Indian market, it would be prudent to invest only with asset management companies with majority ownership under public sector,” according to official documents.

Source : http://goo.gl/Q7bqln

NTH :: No tax deduction for PF withdrawals of up to Rs 50,000, says new notification

PTI | May 31, 2016 08:08 IST | First Post

New Delhi – No tax would be deducted at source for PF withdrawals of up to Rs 50,000 from June 1.

The government has notified raising the threshold limit of PF withdrawal for deduction of tax (TDS) from existing Rs 30,000 to Rs 50,000, a senior official said.

“The Finance Act, 2016 has amended section 192A of Income Tax Act, 1961 to raise the threshold limit of PF withdrawal from Rs 30,000 to Rs 50,000 for Tax Deducted at Source (TDS),” the notification stated.

The provision will come into effect from 1 June 2016, providing relief to subscribers of retirement fund body EPFO.

The government had introduced the proposal to deduct TDS on PF withdrawals in order to discourage pre-mature withdrawal and to promote long-term savings.

According to existing provisions, TDS is deducted at the rate of 10 percent provided PAN is submitted. TDS will be deducted at the rate of 10 percent provided PAN is submitted.

However, in case Form 15G or 15H is submitted by the member, then TDS is not deducted. These forms are to declare that their income would not be taxable after receiving payment of their PF accumulations from retirement fund body EPFO.

While Form 15H is submitted by senior citizens (above 60 years of age), Form 15G is submitted by claimants below the age of 60 years.

TDS is deducted at the maximum marginal rate of 34.608 percent if a member fails to submit PAN or Form 15G or 15H. However, there are certain exceptions to deduction of TDS by EPFO.

However, there are certain exceptions to deduction of TDS by EPFO. TDS shall not be deducted in case of transfer of PF from one account to another PF account.

Also, no tax is deducted if employee withdraws PF after a period of five years.

Source : http://goo.gl/smH1ab

NTH :: Seven macro triggers that may move your market today

Nandini Sanyal | May 16, 2016, 08.38AM IST | ECONOMICTIMES.COM

News about progress of monsoon, next batch of quarterly earnings , wholesale inflation data along with outcome of assembly polls in five states and will be key driving factor for the stock market this week.

Here’s a look at seven triggers that may move the market today

Under Mauritius pact, no tax exemption for quasi equity investments: There will be no free ride for those wanting to invest in India through quasi equity investments such as convertible debentures via Mauritius under the recently amended treaty between the two countries, officials said. Those holding such instruments would do well to convert them into shares before April 1, 2017, to enjoy the exemption on capital gains tax, or grandfathering, that’s available until then. There has been some confusion over whether entities making an investment in such instruments before April 1, 2017, can enjoy grandfathering with the full capital gains tax exemption benefit even after the amended India-Mauritius Double Taxation Avoidance Convention comes into effect.

Shareholder base for private banks may be broadened: Wealthy individuals and finance companies can pick up more equity in private banks while non-state lenders struggling to make money could emerge as acquisition targets for those on the hunt, following the Reserve Bank of India’s recent relaxation of rules aimed at shoring up capital and encouraging consolidation. Analysts said lenders of interest may include IndusInd Bank , Yes Bank , Kotak Mahindra Bank , Karur Vysya Bank , Lakshmi Vilas Bank , Tamilnad Mercantile Bank and Dhanlaxmi Bank.

Monsoon over Kerala may be delayed by a week: The onset of the southwest monsoon over Kerala is likely to be delayed from the normal date of June 1, the weather office said, the first negative signal since it forecast above-normal rainfall this season after two years of drought. “The statistical model used by IMD for predicting the onset of monsoon indicates that the southwest monsoon is likely to set over Kerala on June 7, with a model error of ± 4 days,” the India Meteorological Department said on Sunday . Last year, the monsoon arrived six days late on June 5, compared with the forecast onset date of May 30.

FSSAI plans comprehensive recall policy: Almost after a year of no food product being pulled out of the market, The Food Safety and Standards Authority of India (FSSAI) has decided to bring a comprehensive recall policy this financial year. The last big food recall was in June 2015, of Nestle India’s Maggi noodles. In the making for five years, the draft procedure for a food product’s recall was put up for public comment on the body’s website last year by FSSAI. Its latest newsletter lists “final notification of recall regulations” as among the 12 important things it plans for 2016-17.

EPFO may invest over Rs 6,000 cr in equity market in 2016-17: Union Labour Minister Bandaru Dattatreya has said the Employees Provident Fund Organisation (EPFO) may invest more than Rs 6,000 crore in equity market during the current financial year. The minister, however, said a final decision will be taken by the Central Board of Trustees at the next meeting. Last year, EPFO had invested about Rs 6,000 crore through SBI Mutual Fund’s two index-linked ETFs (exchange-traded funds) — one to BSE’s Sensex and the other NSE’s Nifty.

Sebi planning to tighten listing norms: The Securities and Exchange Board of India (Sebi) is planning to attach bank accounts and properties of promoters who repeatedly flout listing and disclosure norms and fail to take corrective steps. The penalty structure may also be changed to deter publicly traded firms from taking listing regulations casually.Sebi’s latest proposals come amid widespread violations of listing and disclosure norms

Employees’ rights to be foremost in Bankruptcy law: The new Bankruptcy Law will fast- track recovery of dues from defaulters and employees will be first in line to get their share from liquidation of assets if a company goes belly-up, says Union Minister Jayant Sinha. Besides, it would also bring down drastically the time taken to wind up a sick company while making the entire process much easier, the Minister of State for Finance said.

Rupee down: The rupee ended weak by 15 paise at 66.77 due to increased demand for the us dollar from importers amid a weak domestic equity market. Rupee sentiment was also hit as the IIP growth plunged to 0.1 per cent in March and retail inflation soared to 5.39 per cent in April.

Bonds: The 7.88 per cent government securities maturing in CG2030 traded value at Rs 300.00 crore at weighted yield of 7.75 per cent, the 7.59 per cent government securities maturing in CG2026 traded value at Rs 225 crore at weighted yield of 7.45 per cent and the 7.72 per cent government securities maturing in CG2025 traded value at Rs. 100 crore at weighted yield of 7.63 per cent. The weighted yield on government securities with a maturity period of 0-3 years, 3-7 years, 7-10 years and more than 10 years was quoted at 7.11 per cent, 7.51 per cent, 7.52 per cent and 7.76 per cent, respectively.

NSE bond auction on May 16: The National Stock Exchange (NSE) will auction investment limits for overseas investors on May 16, for the purchase of government debt securities worth Rs. 3,340 crore. The auction will be conducted on NSE’s ebid platform from 3.30 pm to 5.30 pm, after the close of market hours, the exchange said in a circular today.

Source : http://goo.gl/ntxH8X

ATM :: As govt rolls back EPF withdrawal norms, 5 reasons to stay invested

PF withdrawal norms dropped: There could be good reasons to keep your money with the EPFO unless you need it for a specific purpose and you have no alternative sources to meet those expenses.

By: Sarbajeet K Sen | Updated: April 20, 2016 5:25 PM | Indian Express

Employee Provident Fund members may have won the battle against the government’s move to impose restrictions on EPF withdrawal, but should they rush to take out the money if eligible to do so?

There could be good reasons to keep your money with the fund unless you need it for a specific purpose and you have no alternative sources to meet those expenses.

Here are a few reasons why you should consider staying invested in with the Employee’s Provident Fund Organisation (EPFO).

Provides old-age income security: The main purpose of contributions to EPF is to create a corpus for the golden years of the members. The corpus created through compulsory savings should be looked at as a fund that would provide financial security at old age. It should not be withdrawn unless for specified emergency purposes. Besides, there is provision for pension and insurance under EPFO.

High rate of interest: EPFO has set the interest rate for 2015-16 at 8.8 per cent, which makes it one of the most lucrative fixed-income savings instruments. This is even better than Public Provident Fund (PPF) which now gives an annual interest of 8.1 per cent. Hence, financial advisors often suggest voluntary increase in EPF contributions from the employee side beyond the mandatory 12 per cent of basic.

Compounding for more years builds large corpus: With the money being compounded at a healthy interest rate the fund can help generate a corpus at retirement can be substantial. A quick calculation shows that an average monthly contribution of Rs 5000 for 30 years at 8.8 per ent compounded annually will create a corpus of Rs 82.35 lakhs after 30 years. However, if the same it withdrawn after 25 years, you will get around Rs 54 lakhs and over 20 years the corpus will be substantially lower at Rs 32 lakhs.

Provides tax-free returns: EPF enjoys Exempt, Exempt, Exempt (EEE) status and hence it is not taxed throughout its life including contribution, accumulation and withdrawal. If tax-saving is factored in, the 8.8 per cent interest rate works out effectively to nearly 12.5 per cent interest if you are in the 30 per cent tax bracket. However, if you withdraw the corpus before completing five years as member and the amount is over Rs 30,000, you will have to pay tax as per your income slab.

Interest paid even in dormant accounts: The government has recently taken a decision to resume paying interest on ‘dormant’ EPF accounts. Earlier, if your money with EPFO had no contributions for over 36 months it was being categorized as ‘dormant’ and no interest was paid on it. That was a good reason to withdraw the money and invest it to other productive avenues. Not any longer. You can now retain the accumulation and earn healthy interest till retirement.

Source : http://goo.gl/mKmSU7

NTH :: Planning to withdraw your EPF? All you need to know about new norms

The new Employees’ Provident Fund withdrawal norms, initially notified on February 10, would make it tough to access the entire amount if you do not meet the criteria set out.

By: FE Online | April 6, 2016 1:54 PM | Financial Express

Are you planning to withdraw your Employees’ Provident Fund (EPF) corpus? If you have been without a job for two months and want the entire corpus to come to your kitty in one go, you should apply for withdrawal before April 30. This is because the Employees’ Provident Fund Organisation (EPFO) has recently deferred the applicability of the new withdrawal norms from May 1, 2016. The new norms, initially notified on February 10, would make it tough for you to access the entire amount if you do not meet the criteria set out.

As per EPFO norms, 12 per cent of an employee’s salary goes as contribution to EPF along with a matching contribution from the employer.

The existing withdrawal rules say that a subscriber who has been out of job for two months can apply for withdrawal of the entire accumulated corpus. However, once the new norms come into play this would change.

So, what do the new norms say? And how are they different from the present norms?

Change in retirement age: For starters, the new norms would set the retirement age for provident fund purposes to 58 years against the earlier 55. The revised norms are pegged around this age criteria.

How much can you withdraw? Unlike the present status, the new norms would make it difficult to withdraw the entire corpus (including employer’s contribution, employee’s contribution and the interest accrued) lying against your name. Under the new provisions, if you are below 58 years, and employed, you will be able to withdraw only your own contributions lying in the fund and the accrued interest on that. You will be allowed to withdraw the employers’ contribution only when you attain 57 (one year before the retirement age of 58). Since the earlier retirement age was 55, you could withdraw the entire amount once you reached that age, which will be pushed back year from May 1.

The 90 per cent provision: With the present 55 years retirement provision, the EPF norms says that a subscriber is permitted to withdraw up to 90 per cent of the entire balance (employer’s contribution, employee’s contribution and accrued interest) once you attain 54 years or within a year of actual retirement. Once the new 58 years retirement age provision kicks in, the withdrawal option will be available once you attain 57 years. And the entire corpus, instead of 90 per cent, can be pulled out at one go.

Membership to stay: The new norms would force you to remain an EPFO member till retirement age of 58, or between 57 and 58 if you wish to pull out your money a year before. This is because the employers’ contribution cannot be withdrawn till that time.

Earlier, once an employee withdrew the entire amount at any time citing two months of being without an employment, your EPFO membership would terminate.

Exemption for women: The new norms make it easier for women It stipulates that woman who quit their job for getting married, pregnancy or childbirth will not have to wait for two months to withdraw. They can do so immediately.

Withdrawal before 5 years to be taxed: However, as earlier, if you withdraw your PF money within 5 years of joining as a subscriber, your withdrawal would be subject to Tax Deduction at Source (TDS) if the amount is above Rs 30,000.

Source : http://goo.gl/qzuQM2

NTH :: Dormant PF accounts: EPFO may consider interest payment since April 2011

The Central Board of Trustees of EPFO on Tuesday took a decision to pay interest on dormant accounts from April 1, 2016. However, it could not take a decision on making this applicable retrospectively from April 1, 2011 till March 2016.

By: Sarbajeet K Sen | New Delhi | March 30, 2016 4:33 PM | Financial Express

The Central Board of Trustees of EPFO on Tuesday took a decision to pay interest on dormant accounts from April 1, 2016. However, it could not take a decision on making this applicable retrospectively from April 1, 2011 till March 2016.

After its decision to pay interest on dormant accounts from April 1, 2016, the Central Board of Trustees (CBT) of the Employees’ Provident Fund Organisation (EPFO) is likely to consider payment of interest on dormant accounts from April 1, 2011 to March 31, 2016.

“The trade unions had demanded payment of interest on dormant accounts from April 1, 2011 itself. However, the government has deferred a decision on this and has applicable from April 1, 2016 onwards. We will take up the issue in the next meeting of the Central Board of Trustee (CBT),” D L Sachdeva, CBT Member representing All India Trade Union Congress (AITUC) told FeMoney.

The CBT on Monday took a decision to pay interest on dormant accounts from April 1, 2016. However, it could not take a decision on making this applicable retrospectively from April 1, 2011 till March 2016.

The UPA government had announced that no interest will be paid on dormant accounts with effect from April 1, 2011. Dormant accounts are those where no money has been credited for a period of 36 months.

Sachdeva said with nearly Rs 32,000 crore lying in 9 crore dormant accounts, a rough calculation of 8.5 per cent annual rate of interest, the unpaid interest since April 2011 works out to Rs 12,500 crore. It would be substantially larger if compounded annually. “All union representatives in CBT were unanimous that the interest should be credited in these accounts,” Sachdeva said. He said that they have pressed that these issues should be discussed in the finance and investment committee of the CBT after which it should be placed before the board.

Former, Central Provident Fund Commissioner (CPFC), A Vishwanathan, agreed that the government should pay interest on dormant accounts since April 1, 2011. “The original decision itself is questionable. Since the money is held in trust it is not good to hold back interest for the interim period. This is more so because EPF contribution is made by the subscriber to build a corpus which may be required at retirement or when one does not have a job or is unable to work,” Vishwanathan said.

He pointed out that EPFO was making gains on the investment and it was wrong not to reward subscribers. “EPFO is making gains on investment. It is morally dishonest not to pay the subscribers,” Vishwanathan, who headed EPFO at one time, said.

Source : http://goo.gl/Op0SLi

NTH :: Government may make it mandatory for companies to route share towards retirement savings into EPS

By Yogima Sharma, ET Bureau | Mar 10, 2016, 07.00 AM IST | Economic Times

NEW DELHI: Finance Minister Arun Jaitley may have been forced to back down on taxing Employees’ Provident Fund (EPF) withdrawals a week after introducing the measure in the Budget, but the government has not given up on the goal of creating a pensioned society.

It’s now considering a proposal to make it mandatory for employers to route most of their share toward the retirement savings of employees into the Employee Pension Scheme (EPS) rather than EPF for employees above the salary threshold of Rs 15,000 per month, an official said. Aprivate sector employer matches contributions made by an employee to EPF — 12% of basic salary by each. While all of the employee’s contribution goes to EPF, 8.33% of the employer’s payment goes to EPS subject to a maximum of Rs 1,250 a month.

That’s 8.33% of Rs 15,000, the statutory limit for contributions. These and other EPS conditions may change if the proposal is implemented wherein those earning more than Rs 15,000 a month will see a higher share of the employer’s contribution going to EPS.

Changing the rule on the employer’s contribution would mean that a substantial portion of this would go toward a pension for the employee, rather than getting withdrawn at one shot from the EPF at retirement. This will maintain parity between EPF and the General Provident Fund as the former will continue to enjoy exempt-exempt-exempt (EEE) status at the stages of investment, accumulation and payout. “This proposal was discussed at a highlevel meeting in the PMO last week,” said the senior government official cited above. He was one of those who attended the meeting.

There was near agreement that this would be a better way to move toward a pensioned society, according to the official, who did not wish to beidentified. “Government does not want to go wrong this time and we would ensure that there are extensive consultation with all stakeholders on the proposal,” the official added.

On Tuesday, Jaitley scrapped his Budget proposal to tax EPF withdrawals unless the subscriber bought an annuity, saying that the government wanted to undertake a comprehensive review. This followed a backlash against the move from those who would be affected despite the government explaining that it wanted to discourage people from taking out all their money in one shot and ensure that they had a steady income over the remainder of their lives.

The EPS proposal was welcomed by tax experts.

“Making employers contribute to EPS is a more sensible decision that will help the government (succeed in) its objective of creating a pensioned society,” said PwC personal tax leader Kuldeep Kumar. Kumar is of the view that the government should restore an EPS feature that was discontinued two years ago and change the provisions of the scheme so that defined benefits are given only to those in the low-income segment.

The government used to contribute 1.16% to the pension kitty of every EPF member as part of EPS run by the EPFO to offer a pension for life after the age of 58. In September 2014, EPFO withdrew this subsidy for those earning above the threshold of Rs 15,000 per month.

Source : http://goo.gl/Hbxzaj

NTH :: PF interest rate hiked to 8.8% for 2015-16 from existing 8.75%: Bandaru Dattatreya

The government on Tuesday increased interest rates on provident fund (PF) to 8.8 per cent for the ongoing financial year ended March 2016 from 8.75 per cent earlier.

By: FE Online | New Delhi | February 17, 2016 10:16 AM | FinancialExpress.com

EPFO provides the rate of interest from its earnings on investment on formal sector workers’ fund without any assistance from the government. (AP)

The government on Tuesday increased interest rates on provident fund (PF) to 8.8 per cent for the ongoing financial year ended March 2016 from 8.75 per cent earlier.

EPFO has been paying 8.75 per cent interest rate for the last two fiscals to its 5 crore organised sector subscribers.

“PF interest rate is hiked to 8.8 per cent for 2015-16 from existing 8.75 per cent,” said Labour Minister Bandaru Dattatreya on Tuesday. “We had last time given 8.75 per cent and this time, seeing the situation, we are declaring 8.8 per cent for the workers,” he told reporters after chairing the 211th meeting of the Central Board of Trustees (CBT) of the Employees’ Provident Fund Organisation (EPFO).

The trade unions had demanded that the interest rate be fixed at 8.90 per cent, the government had revised it to 8.80 per cent, he said, underlining the Centre’s commitment to the working class.

EPFO provides the rate of interest from its earnings on investment on formal sector workers’ fund without any assistance from the government. The income projection of the retirement fund body is upwards of Rs 34,844 crore for the current fiscal. At this, EPFO would not have any problem to raise the rates to even 9% considering that it would still have Rs 100-odd crore surplus.

Source : http://goo.gl/M5GRI6

NTH :: EPFO planning one time bonus of Rs 750 crore for its subscribers in FY16

By Yogima Sharma | ET Bureau | 11 Feb, 2016, 07.00AM IST | Economic Times

NEW DELHI: The Employees’ Provident Fund Organisation is considering doling out a Rs 750 crore bonus to its subscribers for 2015-16 instead of raising the interest rate, a first of its kind move that could translate into double-digit returns for crores of workers on their retirement funds.

EPFO had earlier proposed raising the interest rate to 8.95% in the current fiscal year, compared with 8.75% in 2013-15 and 2014-15, based on its earnings estimate for the year.

The proposal had met with some resistance from the finance ministry as it would put pressure on it to raise interest rates on small savings schemes and would not be sustainable going forward. Therefore, the retirement fund body that manages the savings of more than 5 crore organized sector workers is considering a onetime bonus payment.

“We are considering the option of bonus for the first time because this would substantially benefit people in the low income bracket who are otherwise not entitled for an income tax exemption for deductions under PF,” a senior government official, who is privy to the proposal, told ET. Only those subscribers who have contributed for 12 months in a row would be eligible for the bonus. As per EPFO’s internal estimate, around half its subscribers would get bonus this year if the proposal went through with this condition.

“In a way we are introducing differential interest rate for our subscribers under which low income people would get double-digit interest rate for their deposits in the current fiscal (year),” the official said, speaking on the condition of anonymity.

The February 16 meeting of EPFO’s Central Board of Trustees – it includes representatives of the government, employees and employers – would weigh both options (bonus payout and an increase in interest rate) and will make a final decision.

To become effective, it will then have to be notified by the finance ministry. The proposal of differential interest rate, however, is likely to face stiff opposition from trade unions including RSS-affiliate Bhartiya Mazdoor Sangh.

“We don’t appreciate the idea because it is only benefiting a few and not all EPFO subscribers. What they propose to distribute as bonus is the surplus income from the contribution of all employees and hence it should be equally distributed,” Vrijesh Upadhya of BMS said.

EPFO provides the interest from the returns on investments it makes, without any assistance from the government. So, workers’ representative are of the view that there is no difficulty in providing a higher rate of interest for the current fiscal year.

Source : http://goo.gl/1FWWIq

NTH :: PF may be withdrawn online from August

PTI|11 Feb, 2016, 04.19PM IST | Economic Times

NEW DELHI: Retirement fund body EPFO may launch by August an online facility to withdraw provident fund, a move that will reduce paperwork and provide hassle-free service to its subscribers.

With the new facility, settling PF withdrawal claims would just take few hours.

“We are hopeful of launching an online facility for PF withdrawal claims by August this year. We have already digitised our records and processes using Oracle operating system,” a senior EPFO official told PTI.

“EPFO will soon buy blade servers for setting up three Central Data Centres at Gurgaon, Dwarka (Delhi) and Secunderabad. All the three centres will be connected to 123 offices of the Employees’ Provident Fund Organisation (EPFO),” he said.

The process of procuring servers would be completed by May while the testing would start in June to gauge the response of the system in place.

“After intensive testing and trials in June and July, we are planning to launch the online PF withdrawal facility in August this year,” the official said.

Once this is operational, subscribers can apply online for PF withdrawal, which will be transferred directly to their bank accounts.

At present, subscribers who wish to settle their accounts with the EPFO are required to apply manually.

For settling online claims, the subscribers would have to activate their Universal (portable PF) Account Numbers which are seeded with KYC details including bank accounts, Aadhaar number and permanent account number.

The EPFO has over five crore subscribers.

As many as 6.15 crore UANs were issued by EPFO out of which 2.34 crore have been activated by the subscribers so far.

Source : http://goo.gl/Nf7HsB

NTH :: Labour ministry asks EPFO, ESIC not to inspect startups for 3 years

PTI | Jan 25, 2016 16:55 IST | FirstPost

New Delhi: The Labour Ministry has directed retirement fund body EPFO and health insurance provider ESIC to exempt startups from inspection and filing returns for 3 years.

In line with Prime Minister Narendra Modi’s vision to nurture startups, the ministry said in a set of directions last week that the new age ventures should be allowed to self-certify their compliance with 9 labour laws.

Labour Secretary Shankar Aggarwal in a letter said startups should not be inspected or asked to file returns for 3 years under 9 laws including Employees’ Provident Fund and Miscellaneous Provisions Act and the Employees State Insurance Act.

“Promoting startups would need special hand holding and nurturing. Thus, such ventures may be allowed to self-certify compliance with the Labour Laws,” he added.

They will be exempted from inspection under the Building and other Construction Workers (Regulation of Employment and Conditions of Service) Act, Inter-State Migrant Workmen (Regulation of Employment and Conditions of Service) Act, Payment of Gratuity Act and Contract Labour Act.

Startups will also be exempted from filing returns under the Industrial Disputes Act, Building and other Construction Workers Act, Inter-State Migrant Workmen Act, Contract Labour Act, EPF Act and ESI Act.

There will be a blanket exemption from inspection and filing returns for the first year and would be asked to file an online self declaration form.

They will also not be asked to file return or inspected for the next two years, but will be inspected in case a “very credible and verifiable” complaint of violation is filed in writing and the approval has been obtained from the Central Analysis and Intelligence Unit (CAIU), Aggarwal said.

Except the EPF and Miscellaneous Provisions Act and the ESI Act, the implementation of other seven laws lies in both central and state government’s sphere.

Labour Ministry had directed its officials as well as the EPFO and ESIC to regulate inspection of startups, under laws which lie in the centre’s sphere.

Source : http://goo.gl/9H9uch

NTH :: Interest rates on small savings schemes like PPF may be reset every quarter

By Deepshikha Sikarwar, ET Bureau | 23 Jan, 2016, 10.31AM IST | Economic Times

NEW DELHI: Interest rates on popular small savings schemes such as Public Provident Fund (PPF), National Savings Certificate (NSC) and the Kisan Vikas Patra could soon be reset every quarter as part of the government’s plan to peg them closer to market rates to reduce market distortions and help the cause of lower interest rates.

The government will also reduce the mark-up over the benchmark government bond rate for such schemes of small maturities to nudge short term rates lower.

High interest rates on small savings schemes have long been cited as a structural barrier to interest rates coming down as they compete with bank deposits, but are not subject to the same kind of market pressures as them. Because they stay high, bank deposit rates are forced to remain high and therefore prevent lending rates from coming down.

A senior government official said the first reset under the new rules will happen from April 1 this year and rates are expected to fall. A notification will be issued soon, this official said, adding that interest rates on schemes for senior citizens and a scheme for girl children were not likely to be revised.

Small savings’ interest rates are linked to yields on government bonds of comparable tenure, but unlike gilts that are traded daily and see yields change, these change only sparingly.. The last revision in rates on these schemes was on April 1last year. Since then, market rates have moved south following a 0.75 percentage point policy rate cut by the Reserve Bank of India, creating a wide wedge between what the banks can offer and what is available on small savings.

State Bank of India, for example, offers 7 per cent on deposits of maturity of five years or more. Deposits of such tenure fetch 8.5 per cent in a post office small savings account. The PPF rate for a similar maturity is 8.7 per cent. This wide gap between small savings’ and market rates impacts deposit mobilisation by banks as their ability to reduce deposit rates is adversely impacted. This impacts banks’ ability to lower lending rates as well.

A quarterly reset of small savings rate will ensure that distortion in the rates caused by the small savings is kept to a minimum, officials said. The weighted average yield of dated government securities was 7.9 per cent in April-September 2015 compared with 8.81 per cent in the first half of the preceding year, potentially opening up the possibility of an up to one percentage point reduction in the small savings rate.

In their pre-budget meeting with Finance Minister Arun Jaitley earlier this month, banks and financial institutions had also suggested quarterly benchmarking of rates.

Source : http://goo.gl/LBLfSt

NTH :: EPFO Insurance Scheme – Hassle free: Nominee entitled for benefits, irrespective of cause of death

Here’s all that you should know about the employee deposit linked insurance scheme.

Written by Adhil Shetty | Published:Dec 11, 2015, 2:00 | Indian Express

Not many investors know that the retirement benefits administration body Employees’ Provident Fund Organisation (EPFO) offers an insurance scheme covering all employees working with organisations as part of the EPF.

Along with the Employee Provident Fund and the Employee Pension Scheme, the Employee Deposit Linked Insurance (EDLI) forms the troika of the social security schemes administered by the Employees Provident Fund Organisation.

Here’s all that you should know about the employee deposit linked insurance scheme.

What is Employee Deposit Linked Insurance?

Employee Deposit Linked Insurance is a term insurance plan offered by the EPFO. The scheme offers life coverage for all employees working with the organised sectors and enrolled in EPF. The scheme is administered by the Employees Provident Fund Organisation and is applicable to all companies who are part of the EPF.

The EDLI scheme works just like a group term insurance plan where if an employee dies during the service period, his family or nominee gets the sum assured up to a certain maximum limit as defined by the rules of the EDLI scheme.

Protection coverage under the EDLI scheme

Being a group term insurance plan, EDLI offers a 24-hour-protection to the employees as part of the scheme. This means the insured does not need to be at their workplace for the scheme to be valid or applicable. The scheme protects them 24×7 irrespective of whether they are at work or not.

The coverage and premium charges under the EDLI scheme are the same for every employee irrespective of any factor including age or gender.

Employees contribute 0.5 per cent of their monthly basic pay and dearness allowance (capped at a maximum of Rs 15,000) as premium for this, and the coverage is linked to the premium.

The family or nominee of the policyholder (employee) under the EDLI scheme will get benefits irrespective of the cause of death including illness, accident, or natural causes.

EDLI earlier had stipulated 12 months of service with the same employer as a mandatory condition for being protected under the insurance scheme. Now, there is no such minimum limit of service and employees are covered under the EDLI scheme as soon as they start working with a company.

Extent of claim available

As per the recently issued EPFO guidelines, the maximum claim amount is capped at 30 times of the last drawn salary of the policy holder. Along with the claim amount, EPFO also offers a bonus of Rs1.5 lakh for each claim.

So the maximum claim amount you can avail under the EDLI scheme is therefore calculated as 30 times Rs 15,000 plus the Rs 1.5 lakh bonus, which comes to Rs 6 lakh. The previous limit was Rs 3.6 lakh only.

How to file for a claim

Before you opt for a claim under the EDLI scheme, make sure that you have all the required documentation in place. You will need:

* Death certificate of the employee as issued by the local municipal corporation.

* Legal heir certification or succession certificate.

* If the employee was working with a company exempted under the EPF Scheme 1952, the employer will need to submit the PF details of last 12 months.

* Once you have all the documents in place, you will need to submit the EDLI claim form. The form is available at: http://www.epfindia.gov.in/site_docs/PDFs/Downloads_PDFs/Form5IF.pdf

You should also submit Form 20 and Form 10D / 10C to claim provident fund dues. Before submitting the claim form, you will need to get it attested by the employer.

Source : http://goo.gl/H6OSfl

NTH :: EPFO may raise interest rate on PF from 8.75% for FY16

PTI | Dec 8, 2015 19:24 IST | FirstPost

New Delhi: Retirement fund body EPFO is likely to increase the interest rate on PF deposits for 2015-16, from 8.75 percent fixed for the last two financial years, during its trustees’ meet on Wednesday.

“Though the proposal for fixing rate of interest on PF deposits is not listed on agenda, the EPFO’s apex decision making body the Central Board of Trustee (CBT) can announce rate in its meeting scheduled tomorrow,” according to a source.

Maintaining same EPFO interest rate. Reuters Maintaining same EPFO interest rate. Reuters

The source further said the meeting is called mainly to discuss the restructuring of Employees’ Provident Fund Organisation (EPFO), but since the EPFO has worked out income projections for the current fiscal, the rate of interest can be fixed in tomorrow’s meeting.

The income projections for the current fiscal suggest that the body can pay rate of interest which is slightly higher than 8.75 provided in 2013-14 and 2014-15.

The finance ministry, however, wants EPFO to retain the existing interest rate of 8.75 per cent for FY 2015-16.

During a recent meeting of top officials from the finance and labour ministries, the former urged the latter to retain the interest rate at 8.75 per cent for the current fiscal as well in view of the government’s intention to reduce rate of returns on small saving schemes and PPF, said the source.

However, fixing the interest rate solely depends on the EPFO’s apex decision making body CBT, headed by the labour minister, as the body provides rate of return from its own income.

Source : http://goo.gl/gDMJwH

NTH :: Now, employees can withdraw EPF money without employers’ permit

Prashant K. Nanda | Last Modified: Wed, Dec 02 2015. 01 47 AM IST | Live Mint

Employees can avail the benefit if details such as Aadhaar number and bank account number have been linked to the EPF UAN and their KYC verification has been done by the employer

New Delhi: Employees will no longer need the approval of their employers to withdraw money from their Employees Provident Fund (EPF) corpus.

If details such as Aadhaar unique identity number and bank account number have been linked to the EPF universal account number (UAN) and their know-your-customer (KYC) verification has been done by the employer, then the employees can avail themselves of the benefit of this hassle-free initiative immediately, the Employees Provident Fund Organisation (EPFO) said on Tuesday.

The state-run retirement fund manager also issued an order on Tuesday to all its field offices across India, instructing them to give effect to the order immediately.

In its quest to make EPFO a more subscriber-friendly organization, the retirement fund manager had delinked the employer from the process, central provident fund commissioner K.K. Jalan said.

Currently, employees need the approval of their employers to withdraw their EPF corpus, leading to unwanted delays on occasion.

Many employees have complained to the EPFO that organizations at times use their approval powers as a tool to harass them.

“Employees whose details like Aadhaar number and bank account number have been seeded into their UAN and whose UAN has been activated, may submit claims in Form 19, Form l0C and Form 31 directly to the commissioner without attestation of their employers, in such form and manner as may be specified by the central provident fund commissioner, for fast settlement of claims,” the EPFO order dated 1 December said.

Since October 2014, the government has allowed EPF number portability through UAN.

All active EPF subscribers have been allotted a UAN which needs to be linked to his Aadhaar and bank account numbers.

The employer verifies the details and approves the KYC details through a digital signature.

But in the past one year, not all EPF subscribers have activated their UAN on the EPFO portal, largely due to three key reasons—lack of awareness, pending KYC and lack of digital signature.

Of the over 40 million active subscribers, only 21 million have activated their UAN, as per data available with the labour ministry.

EPFO authorities said the simplified withdrawal process will work as a catalyst to persuade more employers to get their KYC done and activate their UAN.

“As a retirement fund body, we are now focusing on our subscribers. We are turning subscriber-friendly and hope more people can take benefit from it,” said Jalan, adding that as the corpus and the subscriber base grows, EPFO will continue to adopt new practices.

EPFO has a corpus of more than Rs.8 trillion—Rs.6 trillion directly under it and another Rs.2 trillion with exempted trusts and company trusts who manage their own EPF under the direct supervision of the EPFO. The corpus has been growing by 15% every year for the last couple of years.

Sharad Patil, secretary general of Employers Federation of India, said that the move looks “logical”. “If the withdrawal happens through Aadhaar and bank account, it will reduce the settlement period and also cut down the chance of corruption in the EPFO,” Patil said.

Source : http://goo.gl/wLq25w

NTH :: After EPFO, smaller pension funds set to invest in stocks

TNN | Sep 3, 2015, 06.25AM IST | Times of India

The government, with an objective of creating a credible counterbalance to foreign funds in the stock market, is getting several smaller pension funds controlled by it to follow the Employees’ Provident Fund Organisation (EPFO) to invest part of their corpus in the stock market. Last month, for the first time in its 64-year history , EPFO, which manages over Rs 8.5 lakh crore worth of funds for salaried employees, started investing 5% of its incremental inflows (about Rs 400 crore per month) in stocks.

“Coal Miners Pension Fund, Seamen’s Provident Fund Organisation, Assam Tea Planters’ Fund, Jammu & Kashmir employees’ pension fund and several other such funds are now talking to Sebi for investing in stocks,” a senior Sebi official said.”The overall strategy for the government, to get domestic pension funds to invest in the equity market, is to have in place an institutional money pool which could be a counterbalance to FPIs,” the Sebi official said. FPIs, or foreign portfolio investors, mainly constitute foreign institutional investors (FIIs) and also include foreign individual investors and other investors of non-Indian origin.

Such a strategy to create a large pool of domestic institutional investors is necessitated by the fact that often, because of domestic or global factors that could be fundamental or technical in nature, foreign funds start buying or selling in the Indian market. This, in turn, leads to substantial volatility in the Indian market. To check such abrupt and sharp volatility , the government wants to have in place a large pool of long-term domestic institutional money , the Sebi official said.

As of now, mutual funds have around Rs 3 lakh crore in equities while another Rs 5 lakh crore is with insurance companies and other institutions. The combined equity investment figure of these domestic institutions nearly equals the total equity holdings of FPIs. Yet, selling by FPIs leaves a major impact on the stock market because they can take money out of India while domestic institutions cannot. The government wants a cushion that is able to balance out selling by FPIs even on a major scale.

Last month, EPFO started investing in the stock market through two of SBI Mutual Fund’s exchange-traded funds (ETFs), one each on nifty and sensex indices. To tap the long-term pension money from these PF funds, mutual fund houses are also launching ETFs, with UTIMF being the latest to open a sensex and a nifty ETF. LICMF and IDBI Bank have also filed their documents with Sebi.

Although EPFO has the leeway to invest up to 15% of its incremental corpus in stocks, it has started with 5%.Fund industry players said that other smaller PFs, which are also talking to Sebi to start investing in the stock market, will not take any extra risks in such investments and follow the EPFO model and stick to 5% now.

Source : http://goo.gl/ZZjpjs

NTH :: Pledge future PF to pay home loan: plan for weaker sections

The scheme would, however, be available only for low-cost housing and subscribers whose monthly salary is less than Rs 15,000. These workers constitute about 70 per cent of the EPFO’s five crore subscribers.

Written by Surabhi | New Delhi | Published:July 31, 2015 3:56 am | Indian Express

The scheme would, however, be available only for low-cost housing and subscribers whose monthly salary is less than Rs 15,000. These workers constitute about 70 per cent of the EPFO’s five crore subscribers.

The Government is considering a proposal to allow subscribers of the Employees’ Provident Fund Organisation (EPFO) to pledge their “future stream of provident fund (PF) contributions” to pay off a housing loan.

The option has been recommended by an expert committee set up by the retirement fund body to facilitate housing for its subscribers as part of the government’s mission to ensure housing for all by 2022.

Under the proposal, when a subscriber purchases a house with a loan from a bank or a housing finance company, he can take an advance from his PF accumulation and also sign a tripartite agreement with the bank and the EPFO for pledging his future PF contributions as equated monthly installment (EMI) payment.

The scheme would, however, be available only for low-cost housing and subscribers whose monthly salary is less than Rs 15,000. These workers constitute about 70 per cent of the EPFO’s five crore subscribers.

“The committee was of the view that the majority of the members of the EPFO belong to vulnerable sections, and given their monthly earnings, the amount of loan required and availed by them would be less… the monthly PF contribution stream would cover a major portion of the loan EMI,” said the report which was submitted to the government recently.

The eligible subscribers could also be permitted to avail a benefit or subsidy by the Ministry of Housing and Urban Poverty Alleviation through its schemes for purchase of housing for economically weaker section (EWS) to supplement the EMI.

The report is expected to be taken up for discussion within the Ministry of Labour and Employment and then presented to the EPFO’s Central Board of Trustees (CBT) over the coming months.

The expert committee, which was set up in February this year following a recommendation by the CBT, unanimously backed the proposal but recommended that the retirement fund body would not provide standing guarantee for payment in case of default by the subscriber.

“Under the proposed tripartite agreement, the only obligation on part of the EPFO is to make available or pledge to the bank the future stream of PF contributions that are received by a member till such time that the loan is completed,” said the report.

So in case a subscriber gets laid off, the EPFO will not be responsible for re-paying the loan. In such cases, banks can take action against the person. The committee has pointed out that the option would also improve the credit worthiness of the subscribers and not impact their monthly take home salary.

At present, 12 per cent of a worker’s basic salary — up to Rs 15,000 per month — and a matching contribution of 12 per cent by the employer is deducted as PF contribution every month; 8.33 per cent of the employer’s contribution is then diverted into the Employees Pension Scheme (EPS). Subscribers are also allowed to make premature withdrawal from their retirement fund for building a house.

The committee had considered other options such as purchase of low-cost dwellings by the EPFO from agencies like HUDCO and NBCC; creating subsidiary to purchase plots for construction or houses; releasing the full PF accumulation to subscribers purchasing a house as well as providing a subsidised loan through the EPFO for the purpose.

Source : http://goo.gl/CLwCyn

NTH :: EPFO plans housing scheme for members, says labour minister Bandaru Dattatreya

PTI | Jul 10, 2015, 06.49PM IST | Times of India

NEW DELHI: Retirement fund body EPFO is considering a scheme for its subscribers so that they are able to own a house by retirement, labour minister Bandaru Dattatreya said on Friday.

“We have to see that by retirement every EPFO subscriber has his own house … We are considering this,” he said while unveiling ‘Nidhi Aapke Nikat’ or ‘PF Near You’, a public outreach initiative for its 6 crore members.

While he did not provide details of the scheme, sources said the ministry intends to collaborate with PSU banks, housing finance companies, state-owned construction firms like NBCC and authorities like DDA, PUDA, HUDA to build houses at prices to be fixed by the government.

EPFO’s central provident fund commissioner K K Jalan later told PTI that a committee comprising of EPFO trustees and senior labour ministry officials is working the proposal. The panel is expected to submit its report soon.

He also said EPFO has proposed to increase the maximum sum assured under the employees’ deposit linked insurance scheme 1976 to Rs 4.5 lakh, from Rs 3.6 lakh.

At present, there are over 70 per cent EPFO subscribers whose basic wages are less than Rs 15,000 per month who could benefit from the scheme.

EPFO’s plan comes against the backdrop of the Centre’s recently launched mission – ‘Housing for All by 2022’.

Dattatreya also said the EPFO would soon launch a service to provide details of subscribers account on their mobile phones.

Jalan said the EPFO is in the process of launching a mobile application for availing services like passbook details. The app will be launched by year-end, he added.

The ‘Nidhi Aapke Nikat’ initiative is aimed at increasing the interaction between the various stakeholders of EPFO.

The ‘PF Near You’ would replace Bhavishyanidhi Adalat and would be held on 10th of every month starting from July, 2015.

The programme was observed at all the 122 offices of the EPFO in the country.

Source : http://goo.gl/DOxFCG

NTH :: It’s not a savings account: Govt may cap premature PF withdrawals at 75%

PTI | Jul 7, 2015 08:45 IST | FirtPost.com

New Delhi – The government is looking to cap premature provident fund withdrawals at 75 percent for EPFO subscribers at any given time until the age of 58.

Under the existing provisions, Employees Provident Fund Organisation (EPFO) subscribers can withdraw the entire amount by showing not employed anywhere for two months. The proposal regarding changes in ‘The Employees’ Provident Fund Scheme’ has been sent to the Labour Ministry for approval.

“We will take a decision in this regard in the next 10-15 days,” Labour Secretary Shankar Aggarwal said.

Central Provident Fund Commissioner K K Jalan also said the proposed changes are likely to be notified in the next 10-15 days, as it has got the backing of employee unions.

Asked whether the 75 percent withdrawal ceiling has been proposed for even circumstances like constructing a house, marriage, children’s education, etc, Jalan replied in the affirmative.

The idea behind the proposal, he said, is to ensure that provident fund is used as an old-age security and not misused for purposes other than it was meant to be.

The provident fund money, he said, should be used as an old-age security scheme and not like a savings bank account.

Jalan added the EPFO plans to gradually further cap the withdrawal limit to up to 50 per cent and also put a ceiling on the number of withdrawals by a subscriber.

“Presently, out of the 1.3 crore annual claims, not less than 65 lakh claims are for full withdrawal. If the proposal is implemented by the Centre, the total number of claims would come down to 50 lakh,” Jalan said.

Elaborating on the rationale behind the 75 percent cap proposed, he pointed out that the contribution of an employer including interest, in any case, does not exceed more than 75 percent of the total contribution.

Besides, the EPFO yesterday unveiled its new revamped website. Inaugurating the website, Aggarwal expressed happiness on the various initiatives taken by EPFO in the recent past to bring about a transformative effect on the benefit delivery mechanisms by adopting IT enabled tools and techniques.

He further said that in the coming days EPFO shall be a centre for excellence in governance and would adopt more such citizen friendly initiatives.

Source : http://goo.gl/w2DWD0

ATM :: Six best investment avenues in the current scenario

By Sanjeev Sinha | 7 Jul, 2015, 12.38PM IST | ECONOMICTIMES.COM

Markets in 2014-2015 have been rife with fluctuations. The run up to the elections and its aftermath were great for the stock market. There was new optimism about the economy, industry, and business. Oil prices went down and inflation subsided.

A year later, there are prospects of less than normal monsoon, a world economy belabouring its way to marginal growth, and industrial production showing sluggish to incrementally better performance month by month. Markets too have reacted similarly and have gone down by around 6% from their record high hit in March. In such a situation, investors tend to get confused about how and where to invest. In this article, we will look at 6 avenues of investment that can still give you good returns. Here they go:

1. Equity mutual funds (especially comprising blue chip companies)

Though the market has gone down, there is not much downside in blue chip companies and mutual funds comprising of these companies. The government is clear about manufacturing and is providing faster clearances for factories to be set up, production to start, and energy to be given to the industry.

“This may take a few months to operationalize, but the trend is clear. The projects that were in limbo for the last couple of years have started getting approved. This will create significant momentum and wealth for large firms and their investors. Blue chip equity funds are offered by HDFC Mutual Fund, Birla Sun Life, Reliance and many more,” says Adhil Shetty, founder & CEO of BankBazaar.com.

2. Balanced fund (funds made up of equity and debt)

Many investors are not comfortable with pure equity funds because of high risk associated with the fund. Hence, they look for an avenue that is less risky and also takes advantage of market movements partially. Balanced fund is a good choice for such investors.