Tagged: Education Loan

ATM :: You can cut tax via these 3 expenses and interest income also: Find out how

By Babar Zaidi | ET Bureau|Jan 08, 2018, 06.30 AM IST | Economic Times

Most of us are aware of deductions available to a taxpayer on gross total income. The most well known are the deductions under Section 80C. Here are a few more breaks available under 80C and various other sections of the Income Tax Act that you can make the most of to further reduce your taxable income.

1. Education loan

If you have taken an education loan for yourself, your spouse or children, or a student you are legal guardian to, you can claim this deduction under Section 80E for the interest paid on the loan amount. The entire interest paid in a financial year is eligible for deduction without any limit. School tuition fees also qualify for tax benefit under Section 80C. The amount of tax benefit is within the overall limit of the section of Rs 1.5 lakh a year. For tax purposes, the fee lowers the total gross income of the taxpayer, which in turn, reduces the tax liability.

2. Medical insurance premium

The amount paid as medical insurance premium is eligible for deduction under Section 80D. The maximum deduction that can be claimed under this section is Rs 60,000, but there are many sub-limits. An individual can avail a maximum deduction of Rs 25,000 for premium paid for themself, their spouse or dependent children. An additional deduction of Rs 25,000 is allowed on premium paid for parents. If the policyholder is a senior citizen, the deduction limit is Rs 30,000. One can also claim a tax break of Rs 5,000 on preventive health checks.

3. Home loans

- Repayment of the principal amount of a home loan is allowed as tax deduction under Section 80C. This deduction is available irrespective of the year for which the payment has been made. The amount paid as stamp duty and registration fee is also allowed as a deduction under Section 80C.

- A tax break for payment of interest on home loans is allowed under Section 24. The maximum tax deduction allowed of a self-occupied property is Rs 2 lakh.

- Section 80EE provides for an additional deduction of Rs 50,000 for interest on home loans for first-time buyers. In this case, the loan amount should be below Rs 35 lakh and the value of the house should be lower than Rs 50 lakh.

4. Interest on savings account

Interest earned on savings bank account is allowed as deduction under Section 80TTA. The maximum amount that can be claimed is Rs 10,000. This does not mean that interest of up to Rs 10,000 is exempted income. You should show this amount as income from other sources in your ITR and then claim deduction under Section 80TTA.

Source : https://goo.gl/gUB5Ss

ATM :: Planning your Taxes and your Loans

To avoid last-minute hassles, it is always good to plan taxes and loans in advance.

Sep 15, 2017 06:29 PM IST | MoneyControl.com

In order to avoid any last minute hassles while filing your tax returns, you need to ensure that you plan your taxes in advance. If you have the right foresight and plan your loans and taxes properly, then you can surely save a lot of money.

Here are some key details on planning your taxes and loans…

Salary restructuring

There are a few components which can help in bringing down your tax liability. For this, you need to reallocate your salary. Like medical expenses which are reimbursed by the employer, certain food coupons, house rent allowance, leave and travel allowance etc., should be used efficiently to bring down your tax liability.

Proper use of tax exemption

There are several tax saving options under 80C and 80D. Under 80C, you have options like NSC, PPF, a premium of life insurance, 5-year FD with banks and post office etc. 80D includes premium paid in Mediclaim policies.

Your tax plan and financial plan must go hand in hand

Your tax-saving plan has to be in tandem with your financial plan. Opt for tax-saving options which will contribute to achieving your financial goal.

The loan factor

There are loans which can actually help in reducing your tax burden. So, you should ensure that you make use of this benefit to the maximum.

Exploiting the loan factor:

If you are planning to take a home loan for buying a home, then restructure it in the best possible way as it can give you tax benefits. Under Section 80C, the principal repayment of housing loan can give you a deduction of up to Rs 1,50,000 and under Section 24B, the interest paid on a housing loan can get you a deduction of up to Rs 2,00,000.

Now, if the home loan amount is huge, then it may cross the tax exemption limit. In such cases, you can opt for a joint loan with spouse or parents or siblings. This will help both the individuals to get the tax benefit. It, thus, becomes a useful tax-saving option for the entire family. It should be noted that stamp duty and registration charges that are paid while transferring the property are also eligible for income tax deduction under the Section 80C.

If you take a loan to buy a second home, then to you can get the advantage of tax deductions under Sections 80C and 24B. Under Section 80C, the principal loan amount will be considered and under Section 24B, the interest paid towards the loan will be considered.

Education loan can also be taken for self or for your spouse or children. You can get tax benefits if you take the loan from a scheduled bank or a notified financial company. You can easily claim a deduction for payment of interest. The tax benefits can be enjoyed for a maximum period of eight years or on the term of the loan repayment.

Personal loans also come with the tax advantage. Personal loans which are taken for renovating or repairing home are helpful. Personal loans taken to make down payment of home loan will also give you the advantage of tax benefit.

To sum up…

Thus, there are different ways and means of reducing your tax liability. Loans give you the dual advantage. They take care of your financial needs i.e., buying a home or higher education of your children and at the same time, they also give you the much needed tax-benefit. So, explore all the pros and cons of the various loans and use them to plan your taxes effectively.

Source: https://goo.gl/FAj4J9

ATM :: 10 Ways to Invest Wisely and Save Income Tax

Are you still trying to figure out ways to save tax? Tax saving is not as difficult as we think. We just have to be aware of things that we need to do to reap the tax benefits.

News18 Specials | Updated:July 3, 2017, 2:41 PM IST | news18.com

Are you still trying to figure out ways to save tax? Tax saving is not as difficult as we think. We just have to be aware of things that we need to do to reap the tax benefits. Also, it is crucial to declare investments at the beginning of the year to your employer so that accordingly, he can adjust the TDS (Tax Deducted at Source) and you get the tax benefits in advance rather than waiting for refund from the I-T Department.

Given below are 10 Ways to invest wisely and save income tax.

Home Loan: Paying EMIs for home loan can be a burden for you but the good news is that it can help you claim the tax benefits. You can claim the interest paid upto Rs.2,00,000/- on your home loan EMIs as an exemption from your taxable income. If you make any pre-payments to your home loan, then pre-paid principal upto Rs. 1,50,000/- can be claimed as a deduction.

HUF Account: If you are earning additional income apart from your salary, then it is taxable. However, if you open a Hindu Undivided Family account and show it under your HUF then you can save tax.

Tuition Fee Payment: We usually spend hefty amount of our income to pay for the education of our children. We can get tax rebate for the amount that we pay as tuition fee for upto two children.

Leave Travel Allowance: LTA given by your employer for the expenses that you and your family have incurred on travel within India can be claimed as deduction. It’s better to plan your vacation in advance and get the LTA benefits.

Health Insurance + Medical Expenses: You can claim tax benefit up to Rs.15,000/- for self, spouse and children and Rs.20,000/- for parents above 65 years of age. Additionally, you can claim upto Rs.15,000/- annually for medical expenses by showing genuine consultation and medicines bills.

Pension Funds: Fortunately, I-T laws provide you the opportunity to reduce your taxes if you are investing in pension funds.

Education Loan Repayment: Just like tax benefits available on tuition fee payment, you can also claim deduction for EMIs that you pay towards your Education loan. So investing in your education has more benefits than just upscaling your skillset.

Employee Provident Fund: Under section 80C, not only the interest, income and maturity amount of your EPF account is exempted from tax, but also the contribution that you make to the PF account can be claimed as deduction.

National Pension Scheme: NPS is one of the most secure investment options given by the postal department. You can claim tax rebate on the amount that you contribute to this scheme.

Donations for Charity: While donating for a charitable cause you not only get the inner peace but it also makes you eligible for tax exemption.

Source: https://goo.gl/CmqgtS

ATM :: Financial Slavery: Do you really need a loan-free life?

Sukanya Kumar, Founder & Director, RetailLending.com | Aug 12, 2016, 10.28 AM | Source: Moneycontrol.com

The more we become ‘social’, the more we tend to show-off. It leads to more bad loans. It is time to shun bad loans and embrace good loans wherever required.

This is a very sensitive subject. Most of us in the financial broking business will shiver thinking what will happen, if this ever comes to of no one borrowing anymore. But let us overcome this superficial personal gain agenda and see what lies beneath.

A man in his late 20-s or early 30-s is bound to have a couple of small loans like credit cards, personal loans etc. here and there. They may be for shorter periods. As he progresses well in life and gains stability in his profession, he wants to settle himself. A big part of this ‘settlement’ is buying a home. And a home loan is generally taken for 20 years by most.

Given the current property prices across the world, buying a home with your own savings and liquidating your financial papers is not a possibility. You are bound to fall short way beyond the market price. Gone are those days when a man used to build a home with his retirement benefits and borrowing only from his provident fund account. He never used to enjoy the home fully as he has spent his hay-days staying at a rental home/company accommodation which never was his ‘own’.

The more we become ‘social’, the more we tend to show-off. If my colleague has got something which he boasts about, we have to get the better ones to overtake him. Our home-maker (to the true sense) spouse wants to buy a home with more number of bedrooms and amenities, her neighbouring friend could afford. Even our teenage children want to buy better gadgets to make sure they have their friends’ groups flocking around them and think they have the ‘latest’ ones.

There is no end to these needs, no end to loaning to purchase these, and hence the terms ‘financial slavery’. A man pays 70% of his net take home salary to pay off his monthly loan EMI-s and needs to survive with the balance 30% only, and with this lean sum pay for his home rent, children’s education and their extra-curricular activities, day-to-day expenses, food, clothing, entertainment, hobbies and also family trips and shopping.

We are afraid to start our own venture; afraid to opt for a better opportunity, if it requires us to take a study-break for a couple of months, we are even afraid to get married these days (I hear it from many 30-somethings frequently), since we are afraid to take more responsibility, given that we are already under so much debt.

Now, all of it is not that bad. There are two clear groups of loans. The good loans and the bad loans. One needs to let go of the bad loans to relieve himself / herself from being miserable, and continue happily with the good loans and feel good to have them.

Bad loans:

Any item, bought with loan-money, which depreciates in time, is a bad loan. You never recover the sum you paid, plus you pay the interest on that sum too.

For example, you buy clothes or any electronic gadgets via a consumer durable loan or you buy a car with a car loan, or you buy just some books by swiping your credit card…….. The moment you are walking out of the shop, it depreciates by 30-50% to the least. It becomes a ‘second hand’ item. You never regain the price, unless of course your car becomes a vintage one and pays off (pun intended).

So, a loan on credit card, a personal loan, a consumer durable loan, a car loan- all these are bad loans. It only boosts your ego and gifts you a ‘rich’ lifestyle and only brings momentary joy with no permanent effect on yourself.

Good loans:

A loan which enhances the worth of the purchased product over time and even crosses the mark of it, to give a handsome return over the period, also absorbing the interest cost attached to it.

A home and an education loan are in this category. A home always appreciates in price, if bought wisely with proper research in good location, and will supersede the interest cost too. The percentage of people making a true loss while selling their property is negligible.

The added advantage of taking a home loan is also the tax benefit you get under a couple of sections. There are subsidies available on affordable housing too.

An education loan while taken will be with a moratorium so that it is easy on the pocket of the student. This loan enriches you as a person and helps you get a well-paid job or find a business solution for yourself, after getting trained professionally. The return on this is lifelong. You keep reaping the benefit of you educating yourself, till your last day. The interest you pay while taking this loan is negligible, of course.

Strangely enough, the bad loans are the ones which are more expensive too!

So, to avoid enslaving yourself from paying high monthly debts, please relieve yourself of the high-interest rate loans which are eating away your month’s pay and giving no returns other than being depreciated day by day.

One last thing, many people feel themselves under a ‘burden’ of home loan and tends to close that first. Do not make that mistake ever. If you have spare money, invest in retirement plans, SIP and other low-risk debt-funds to reap the benefit when you are old and retired. By foreclosing your home loan early with the liquid cash and hence not having any money left for investment anywhere, will leave you only with a house post-retirement with no money in hand. And, you can’t eat, enjoy and spend the house for next 20-25 years of your retired life. You need money for that.

Be wise. Live a life without any bad loans. No loans at all may not be financially a good choice for the modern generation, since you want to enjoy yourself when you are young. Ultimately, we live longer now than earlier with all the medial attention we get these days.

Happy Good Loaning! Happy Freedom from Bad Loans!!

Source: http://goo.gl/wKmt0d

ATM :: Relocating abroad and consequences of defaulting on education loan EMIs

Mehul completed his B. Tech in computer science from a leading institute in Pune and was hired by a renowned IT company through a campus interview.

By: Harshala Chandorkar | Published: April 23, 2016 1:58 PM | The Financial Express

Profile: Mehul Kumar (name changed), aged 25 years, a software programmer with a leading IT MNC

Scenario:

Mehul completed his B. Tech in computer science from a leading institute in Pune and was hired by a renowned IT company through a campus interview. At 23 years Mehul had the world at his feet with a high paying job and promising career path charted out for him. After working for two years at the company’s Mumbai office, Mehul was deputed to work on a project in the Chicago office in US. Getting paid in dollars when the rupee was seeing its worst fall, Mehul decided to make most of his finances.

He decided to purchase a plush bungalow in an elite locality in his home town in Pune. While on a vacation back home, he chose the property and made an advance token payment to the builder. He then applied for a home loan at an MNC bank and was confident of express approval considering his high paying international job.

However within a few days he was informed by the bank representative that his home loan application had been rejected owing to his credit history in CIBIL. Mehul immediately accessed his credit report online from CIBIL and found that his report showed defaults on an education loan he had availed for his B. Tech course. Before leaving for Chicago, Mehul had not bothered to ensure repayment on his education loan EMIs as he did not think that not closing dues would impact him in any way. And now his careless attitude had resulted in a bad credit record which hampered his chances of availing the home loan for his dream house.

Solution: What can Mehul do now?

The first thing that Mehul must do is to repay his education loan dues and avail a ‘No Dues’ certificate from the bank. He should then gradually start building his credit history by regularly paying his credit card bills and EMIs on any other loans he may have availed. He should also keep checking his credit report regularly to assess the health of his credit history. As his credit history and credit score improves and shows no defaults and delinquencies, he can apply for the home loan again and be confident of its approval.

Conclusion:

It is critical to understand that while moving abroad is a beautiful opportunity to develop both personally and professionally, one must never forget to payback and close the financial obligations in the home country. Before you go abroad for a longer period of time, it is good to decide what it is you want to do with your existing bank relations and financial liabilities.

One of the most important financial matters to sort at this time is credit card outstandings, loans and any debts that you may still owe. Here are a few tips to ensure that you have an immaculate credit history before you move abroad.

Pay and close all your credit card outstandings. If you decide on cancelling credit cards, ensure you receive a closing statement from the credit card company.

If you are running a home loan or any other loan, ensure that you make arrangements for regular EMI payments on this loan. Keep a track of the monthly EMI repayments and do inform your bank of your relocation and the new address.

It is equally critical to repay and close education loans, if you have availed any. Never think that it’s okay not to repay education loans. You credit report includes details of education loan as well.

Keep a track of your credit history by accessing your credit report and score regularly.

Protecting your credit history and score is critical even if you plan to leave the country and settle abroad. Remember that your credit history and score will affect almost every area of your life when conducting financial transactions. In some countries a prospective employee’s credit report is checked before recruitment. Therefore if you are moving abroad for work please ensure that you have a good credit history. You never know when you may be asked for your credit report!

Source: http://goo.gl/4Yux8A

NTH :: Banks learn a hard lesson worth Rs 5,192 crore on education loans

The figures speak for themselves. As on July 21, 2015, the total exposure of all banks to education loans was Rs 64,900 crore, according to RBI data. On an average, banks face an 8% default on this portfolio – that is Rs 5,192 crore.

Manju AB | Wednesday, 16 September 2015 – 7:25am IST | Place: Mumbai | Agency: dna | From the print edition

Sluggish job creation in the country is seeing students turning out to be the largest loan defaulters. Students from the southern states of Kerala and Tamil Nadu are the ones who are giving bankers sleepless nights, with the latter leading the defaulters list.

The figures speak for themselves. As on July 21, 2015, the total exposure of all banks to education loans was Rs 64,900 crore, according to RBI data. On an average, banks face an 8% default on this portfolio – that is Rs 5,192 crore.

Public sector banks are the worst-hit, as they are mandated by the government to give collateral-free loans. Private banks do not extend education loans. Bankers say moves are afoot to take collateral from the two southern states.

For the largest bank, State Bank of India (SBI), the default rate is 5%. The SBI’s default rate for its home loans is less than 1%. Even in the other portfolios of the bank, the default rate is about 3-4%.

For Bank of Baroda, the default rate on student loan is as high as 8.2% on a portfolio of Rs 2,100 crore. Its overall retail loan default is much lower, at 2.4%, and the home loan defaults is 1.64%. The same rates are replicated at most banks, with the Union Bank of India reporting a default rate of 6.5% and Canara Bank 8%. State Bank of Travancore, which is headquartered in Thiruvananthapuram, is affected the most, with a default rate of 12%.

A senior SBI official said: “Repayment is better in cases where borrowers are settled abroad as they generally get good employment and are able to repay their dues. Also, such loans are backed by collateral security. Students are very mobile. They move away from their place of study and it becomes very difficult to trace them. So, now we are insisting on PAN/ Aadhar details of the borrower/ co-borrower. In addition, we are ensuing that the names of defaulters do appear in the CIBIL database.”

All public sector banks are mandated to run the Student Loan Scheme, based on the Model Education Loan Scheme of Indian Banks’ Association (IBA). Under this model, loans up to Rs 4.5 lakh are extended without any collateral security, with just a co-borrower around. For loans above Rs 4.5 lakh and up to Rs 7.5 lakh, banks seek third-party guarantee. For loans above Rs 7.5 lakh, students need to submit collateral security. Delinquency is highest in the bracket up to Rs 4.5 lakh

“Tamil Nadu leads the default list, followed by Kerala, Andhra Pradesh and Odisha. These states have management courses and students are unable to secure jobs that will take care of their EMIs,” a senior Bank of Baroda official said. The bank has not kept any limit on its education loans.

According to a Union Bank of India official, “About 35% of the bank’s Rs 3,200 crore portfolio is lent to the southern states, where the maximum defaults occur. Loan requests are the highest from these states and we do not refuse education loans.”

Source: http://goo.gl/a47Pbi

NTH :: Education loan default can impact CIBIL score

Harshala Chandorkar | June 4, 2015 18:42 IST | The Hindu

According to CIBIL data, the outstanding education credit, including for study within the country and abroad, stood at Rs. 63,800 crore as on March 31 this year.

Non-repayment of education loan can now affect one’s credit score, a top official of Credit Information Bureau (India) Ltd (CIBIL) has said.

“The education loans have to be paid once one completes his/her course and gains employment. Also, like any other loans and credit cards, education loans are also reported to CIBIL and get reflected in the borrower’s CIBIL Report and impact the CIBIL Trans Union Score,” said CIBIL Senior Vice President Consumer Services and Communications, Harshala Chandorkar.

CIBIL Trans Union Score is a key parameter relied on by banks while processing loan applications.

According to CIBIL data, the outstanding education credit, including for study within the country and abroad, stood at Rs. 63,800 crore as on March 31 this year.

The data released by CIBIL throws significant light on education loan trends in the country.

While the demand for educational loan is need based, the number of new loan accounts opened in calendar year are almost same over the last five years, it said.

Noting that the third and fourth quarters of each calendar year witness a spurt in education loans, the data says about 1,30,000 education loan accounts were opened in the fourth quarter of 2014.

However, the average sanctioned amount continues to grow over time, it added.

“Average sanctioned amount in fourth quarter of 2014 was Rs 6 lakh, while in fourth quarter of 2013 it was about 4.5 lakh. In recent period, loans with amount less than Rs 1 lakh has reduced below 10 per cent of total sanctions while loans with ticket size/amount of more than Rs 5 lakh have gone up to almost 30 per cent of the total sanctions.

“In fourth quarter of 2014, loans of ticket size of more than Rs 5 lakh were around 30 per cent of total sanctions while in fourth quarter of 2012, loans of more than Rs 5 lakh comprised about 22 per cent of total sanctions,” CIBIL said.

It says delinquency on education loans has decreased over the past year.

“Delinquency for 90+ days amount overdue was around 3.50 per cent in fourth quarter of 2013 which has lowered to 2.70 per cent in fourth quarter of 2014,” says the data.

Stating that bad loans from education segment are very high, the Reserve Bank’s Deputy Governor R. Gandhi had asked CIBIL and banks to “counsel” the youth on good credit behaviour during the CIBIL Trans Union Annual Conference in March, CIBIL said in a release.

ATM :: How does a falling rupee affect you?

Priya Nair | May 18, 2015 Last Updated at 00:10 IST | Business Standard

Be prepared to pay more if travelling abroad or if your child is studying there. Other impacts can be varied

Your family and you are flying to the US next week on holiday. Flight tickets and hotel bookings were done in advance. So, why should the rupee depreciation bother you? It should because all other expenses, such as sightseeing, local transfers and food will increase as a result of the fall in the rupee.

Similarly, if your child is studying in a foreign university, don’t be surprised if tuition fees increase substantially over last year.

There are also some advantages of a falling rupee. Those working abroad will gain, as the same amount they remit will translate into more rupees.

“It looks like the rupee will be in the 64-65 range (to the dollar). As the rupee tends to be overvalued and exports are not growing much, the Reserve Bank might be willing to let the rupee depreciate,” says Madan Sabnavis, chief economist, CARE Ratings.

The immediate impact will be on foreign travel and students studying abroad. The indirect impact will be on other expenses, too, as oil prices will go up and this could push up prices of other commodities. However, this time, as the price of crude oil in the international market is low, there might not be much of an impact on domestic oil prices, says Sabnavis.

Below is a look at some ways a weaker rupee will impact your life and what you can do about it.

Foreign travel

Europe tours are popular with Indians in the summer months of April to June. Most people book in October for departures starting in April. Those who have booked and paid earlier, including the forex component, will not feel much of an impact. However, travellers who don’t pay the forex component in advance might feel the pinch. Usually, travellers pay the deposit and for flight tickets in rupees, in advance. The forex component, which covers accommodation, meals, sight-seeing and excursions, can be paid later. “For trips in April, packages are booked as early as October. We pushed many of our customers to pay in advance. Those who did not pay then might feel the pinch now,” says Daniel D’Souza, head of sales, Tour Operating, Kuoni India.

One way to avoid last-minute heartburn is to pay for your entire package in advance and not only the rupee component. If booking last-minute, choosing a short-haul holiday to a destination closer to home rather than a long-haul holiday is also a way to save some costs.

Tips to save

- Reduce the number of days from 10 to, say, eight

- Reduce the number of excursions

- Switching to a lower category hotel or staying in a bed and breakfast or home stay

- Cut on shopping rather than sight-seeing, since it is the experience that matters

- Opting for public transport such as trains, subway or buses, rather than renting a car

- While sightseeing, choose days when tourists are allowed to go for free or given discounts. Most monuments abroad have such days

- While shopping, buying from flea markets can work out cheaper than from stores

- Take a decent amount of cash with you, as you might not get good rates while travelling

- Pre-paid travel cards that allow you to load multiple currencies are a good option. In these cards, the value of the rupee is of the date the money is loaded to the card

Foreign education

Students studying abroad also suffer when the rupee falls. The US, Britain, Canada, Singapore and Australia are popular countries for Indian students. The university will not offer any leeway in tuition fees. Students will have to pay the entire amount. In most cases, you will have to pay before a term starts.

Given the high tuition fees in foreign universities and the cost of living, most students take some loan and pay for the rest by scholarships or taking a part-time job. “When the rupee falls, it becomes difficult for the entire family, not only the student. And, not many individuals know how to hedge themselves against currency fluctuations by using derivative products. What you can do is try and pay the entire fee upfront when the exchange rate is low. Most universities give a discount of one or two per cent if you do so,” says Naveen Chopra, of The Chopras, a foreign educational consultancy.

Neeraj Saxena, chief executive, Avanse, a non-banking financial company that gives education loans, says there is an option to enhance the loan amount during the course. “We don’t usually disburse the full loan amount at one go. We do as per the semester. So, if the fees increase in the third semester, we can increase the loan amount,” he advises.

Saxena suggest students going abroad should look for scholarships or part-time jobs like teaching assistantships. “We find of the Rs 30-35 lakh required for a foreign university course, students often are able to earn Rs 8-10 lakh through part-time jobs, which pay by the hour,” he says.

Tips to save:

- Using discount coupons given by universities and accepted at all major stores

- Using cards like the ISIC (a specialised card for students) for travelling, eating out, even shopping at some departmental stores

- Going for free concerts, to movie halls which offer student discounts

- Going to budget pubs, during happy hours, for leisure

- Use special cards that offer discounts to students for eating out and shopping

Medical costs

The rupee’s weakness will push up medical costs, too. About 30-40 per cent of a hospital’s cost is on account of medical equipment and of these, 80 per cent is imported, says Vivek Desai, managing director, HOSMAC, a health care management consultancy. “Many common procedures in cardiology and cancer care use imported equipment. Even orthopaedic implants and consumables used in laboratories are imported. Any increase in their costs will be passed on to patients and there is nothing the latter can do about it. That is why medical insurance is a must. That, too, comes with a ceiling,” he says.

Other costs like air-conditioning and flooring in hospitals, also imported, will also see an increase and hospitals are likely to pass these on to patients by way of higher charges.

Patients going abroad for treatment will also see an increase in cost due to the rupee’s fall.

Tips to save:

- Health insurance is one way you can deal with rising medical costs. Buy one early in life

- Even if covered under your employer’s group medical insurance, take a separate family floater

- Buy a top-up medical insurance to increase your sum assured without too much increase in premium

A weak rupee will benefit

Remittances

Non-resident Indians (NRIs) sending money home will benefit from the rupee’s weakness, as they will get more returns for what they send. Typically, NRIs with higher disposable incomes send more money to India when the rupee falls, says Sudesh Giriyan, chief operating officer, Xpress Money. “We will see an increase in remittances when the rupee crosses 64 to a dollar. In the case of cash remittances, we don’t see much increase because these are smaller ticket-size. But in direct remittances, which are bigger ticket-size, currency value has a bigger impact,”

Many NRIs also take loans from banks abroad, since the interest rates are lower, and remit money to India in order to invest, he adds.

There is usually an increase of seven to 10 per cent in remittances on account of rupee weakness, says K A Babu, head-retail and NRI banking, Federal Bank. Remittances from the Gulf countries tend to increase in such times than those from elsewhere.

With regard to investments, those from the lower income group prefer bank fixed deposits – NRE rupee deposits or FCNR deposits which are in foreign currency. The NRE deposits offer the same rates as domestic FDs and can be liquidated easily. The FCNR deposits will provide protection from exchange rate volatility, though the rates are lower.

“Ideally, investors should have a mix of both kinds of deposits. That way, they can earn high interest rates and also get a hedge from currency fluctuation,” Babu says.

For NRIs in the high income segment, banks and wealth management firms offer portfolio management services, through which they can invest in stocks, PMS schemes, mutual funds, fixed income products, real estate, etc. The preference is usually for land or residential property. Some NRIs might also look to expand their business in India and buy commercial property.

International funds

International equity funds that invest abroad will benefit from the fall in the rupee. Investors of such funds would have seen their portfolios rise in the past few months. According to data from Value Research, over the past three-month period, returns from international funds have been the highest at 6.19 per cent, while equity multi-cap funds have seen their returns fall 3.19 per cent.

But these gains are marginal and should not be the only reason for investing in international equity funds. For instance, over a one-year period, multi-cap funds have given returns of 34.84 per cent, while in the case of international funds, it is 7.78 per cent.

The US market is currently doing well and will definitely give better returns in the near term, as it will not be as volatile as the Indian equity market. But over a longer term, that is a five-year period, Indian equities will definitely give better returns. So, one can look at international funds provided they have sufficient exposure to Indian equities, say experts.

Anand Radhakrishnan, chief investment officer at Franklin Equity, Franklin Templeton Investments – India, also says investors should not look to time the markets, but invest on a regular basis and in a systematic manner. “Typically, the exposure would depend on the individual’s risk profile and investment objective, but as a thumb rule, one should have at least 20 per cent of their investment portfolio allocated to international assets. Equity investments warrant a longer investment horizon and we recommend investors come in with a three-to-five year horizon or more,” he says.

Source : http://goo.gl/SUyRgr

ATM :: Education loan or top-up loan: A toss-up

ADHIL SHETTY CEO, BankBazaar.com | May 15, 2015, 12.43 PM IST | Source: Moneycontrol.com

Education loans do offer tax benefits and easy repayment norms, however they come with some limitations where a top-up loan scores.

Your all-grown-up son or daughter is finishing school and is raring to fly abroad. After all, the foreign university where he or she had always dreamt of studying at has finally accepted his application. So, you have done your homework as parents and explored all the education loan products in the market. Or, have you?

Education loans certainly one time-tested option to fund your child’s dream education, but there are other equally viable options today. Like top-up loans.

What is a top-up loan?

A top-up loan is an add-on to a home loan, considering the appreciation of the property price over the time. If you already have a home loan with any bank, have paid a minimum of 6-12 EMIs, and have a healthy repayment track record, you can apply for a top-up loan. There are no additional documents required when applying for a top-up loan. All you need to do is to walk in to the bank where you have home loan, and hand over your latest payslip and bank statement to request for a top-up. The bank initiates a technical evaluation of the property already mortgaged with them, and the loan is disbursed to your account within 48 hours in most cases.

Education loan versus top-up loan

Education loans are specifically crafted loans for students, but borrowers are free to make their choices weighing the pros and cons of various loan types, to get the best for their individual needs. Here is how education loans stack up against top-up loans when they go toe-to-toe.

Interest rate: Education loans often come with interest rates ranging from 12% to 17% (on an average), while a top-up loan is just 0.5% to 1% above your home loan rate, that is, at around 11% to 14%. In case a top-up loan turns out to be cheaper, it can actually reduce the interest outgo on your child’s higher education.

Repayment: The tenure of a top-up loan can be the same as that of your home loan, which means you can combine its repayment along with the home loan equated monthly installment (EMI). So considering its stretchable tenure, the monthly outflow will tend to be less. For instance, if you need a loan of Rs 6 lakh and have been offered both top-up loan and education loan at 12% interest rate, the two options shape up differently when you consider your monthly outgo in each. Top-up loans of 6 lakhs for a period of 15 years come with anapproximate EMI of Rs.7,201. The maximum possible tenure for an education loan is 8 years. So, the same loan for 8 years tenure would require you to shell out Rs.9,752 per month – almost a third more than the top-up loan option.

Total cash outflow: Continuing with the above example, for an education loan, the total cash outflow including the interest will be Rs.9,36,163 (without considering Pre-EMI, as it depends on whether you opt for moratorium period or not). A top-up loan, on the other hand, would require an outflow of Rs. 12,96,182. But, assuming you can build a corpus over 8 years, if the top-up loan is pre-closed in the 8th year, you can save around 2.7 lakhs in interest outgo for the balance tenure. This way, the total outflow does not differ much between the two loan options, but a top-up loan can be easier on your wallet as it provides the flexibility of lower EMIs while allowing any accrued savings over time to be redirected towards a pre-closure.

Ease of applying: It is easy to apply for a top-up loan as compared to an education loan, as exhaustive paperwork is not involved unlike an education loan where, along with heavy paperwork, you may need to produce security and guarantors in some cases.

When should you consider an alternative to education loans?

You are not eligible for an education loan: Not all educational courses are approved by banks. For instance, you may not get a loan for an online course. A top-up loan comes to your rescue here.

You need better interest rates: The higher total outflow in case of a top-up loan can be preempted if you pre-close it sooner by building a corpus. Whereas, an education loan can be a costlyaffair considering its higher interest rates.

You need more money for the miscellaneous education-related expenses: Education loans cover only the course fee if you are pursuing education in India. But, other related expenses like capitation fees have to be borne out of your savings. Sometimes education loans come with a ceiling on the amount that can be sanctioned. However, with a top-up loan, you can apply for a higher amount considering your existing home loan, income and the property’s prevalent market value.

On the down side, top-up loans do not have tax benefits unlike home loans. Education loans, on the other hand, offer deduction under Section 80E for interest paid. In a top-up loan, the repayment begins immediately. With an education loan, you can wait for a certain period to start re-payment if you can sit easy with the accumulating interest.

Finally, education loan or top-up loan – the choice is yours. Ultimately, it is a toss-up between friendlier EMIs and higher loan amounts on the one hand, and repayment flexibility and tax rebates on the other, but what should matter is that you have given your child the future he or she deserves.

Source : http://goo.gl/aNQAyO

ATM :: Don’t miss retirement goals for children’s higher education

It could mean having to prolong work life and putting money in risky investment options

Arvind Rao | April 25, 2015 Last Updated at 21:25 IST | Business Standard

It’s a dilemma several middle-aged parents grapple with. Two goals – retirement and saving for children’s higher education – but not enough funds to meet them. Parents would be tempted to compromise on the former to meet the latter. But with medical costs rising exponentially, this can’t be looked at as a viable solution. This could also mean extending their work life or taking greater investment risks closer to retirement.

The dilemma

Here’s a case study that shows how one can strike the right balance. Ajay and Varsha Sharma, aged 50 and 48 respectively, earn Rs 40 lakh annually, which is not enough to fund all of their major goals. They have to repay their existing home loan of about Rs 40 lakh in the next five years. The couple needs Rs 4.5 crore for retirement and Rs 70 lakh in the next 10 years to fund the higher education of their two children.

The family savings work out to about Rs 15 lakh a year. Their employment-linked retirement benefits and 1 BHK property investment is expected to fetch Rs 2.12 crore, or 45 per cent, of their retirement corpus. This leaves them with a gap of Rs 2.48 crore, or about 55 per cent of the total corpus.

To fund the gap, the Sharma’s can invest Rs 10 lakh per annum in a mix of diversified and mid-cap equity funds. Assuming annualised returns of 12 per cent, they should be able to garner Rs 2.48 crore over the next 12 years.

At the current EMI of Rs 54,000, their home loan outstanding at about Rs 40 lakh is projected to close at the end of 10 years. They aspire to accelerate the repayment and close the loan in four years. For this, they will have to accumulate at least Rs 6.50 lakh annually via monthly contributions in recurring deposits. At the end of every year, the accumulated amount should be used to prepay the loan.

The amount of Rs 70 lakh for higher education can be mopped up by investing about Rs 4.5 lakh per annum over the next 10 years in equity-oriented balanced funds, assuming annualised returns of 10 per cent.

With the current family savings, they are looking at a deficit of about Rs 6 lakh per annum, at least for the first five years.

Part-funding children’s education

The couple has decided to make a provision for up to 50 per cent of their children’s higher education budget by extending the period for their accelerated home loan. They can cut the savings rate for the repayment by 50 per cent to Rs 3.25 lakh a year, thereby extending the period for their home loan repayment to about six years. This way, their contribution for the education also comes down to about Rs 2 lakh and savings for all three goals fit within the family savings. The additional family savings at the end of the home loan period could be used to boost retirement savings or for their children’ marriages.

To accumulate the remaining 50 per cent of their education corpus, Sharma’s children can fall back on scholarships. They can also meet the expenses through education loan or loan against fixed deposits:

Education loan: Interest rates on these are 11-12.5 per cent, with tax benefits available under section 80E. A good retirement corpus, in the form of investments, will enable one of the parents to stand as guarantor/co-applicant for the loan. For loans above Rs 4 lakh, margin money, ranging between 15-20 per cent of the loan, may be required, which can be funded by the parents.

Loan against fixed deposits: Let’s assume the Sharma’s garner a corpus of about Rs 2.5 crore at the time of retirement, which they don’t fully need immediately. They could invest, say, Rs 25 lakh in a bank FD giving 8 per cent per annum and take an overdraft against the same for their children’s education. The rate of interest charged in case of overdraft will be 1-2 per cent higher than the FD interest rate. Even assuming a 10 per cent rate of interest, this option works out to be cheaper than an education loan, but the interest paid will be sans tax benefits under section 80E.

The parents can make the children responsible for repaying the overdraft with their earnings. This will enable them to get their fixed deposit back along with the accumulated interest, which can then be utilised for their retirement. The Sharma’s should avoid loans against property as the EMI would be calculated only for their balance working years, which could mean a bigger outgo per month, plus no tax benefits on the interest paid thereon.

Funding education completely

In case the Sharma’s decide to fund 100 per cent of their children’s education and continue with the six-year home-loan closure plan, they would need to set aside Rs 7.5 lakh per annum and work for two more years to fund their retirement corpus. The Sharma’s may have to invest more aggressively, allocating as much as 75 per cent of their savings in a mix of equity mid- and small-cap and sectoral funds, and the remaining 25 per cent in balanced funds to achieve an 18 per cent growth rate and retire within the next 12 years. This strategy, however, may expose the Sharma’s to a bigger risk of not achieving their target corpus within the available time frame if the equity market do not deliver good results. Considering these risks, it is definitely better for them to part-fund their children’s education needs and not compromise on their retirement goals.

The writer is a chartered accountant

Source : http://goo.gl/lNXl7d

ATM :: How to avoid debt traps: All you wanted to know

By: CreditVidya | April 8, 2015 9:12 am | Financial Express

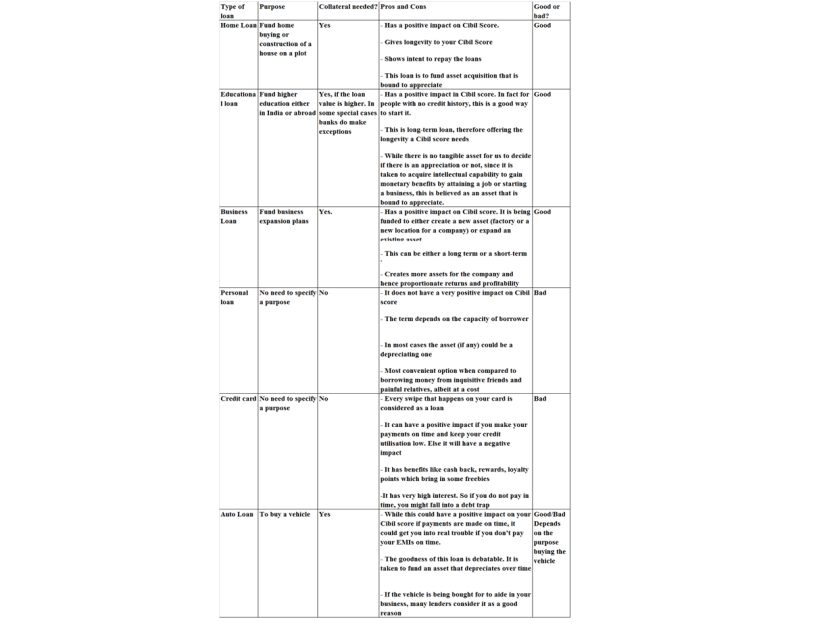

Not all loans are bad. If the loan is used to create an asset and is productive in nature, it can be termed as a good loan. Home, business and educational loans fall in this category.

On the other hand, if the loan creates no asset or is of very little productive use, it can be termed as a bad loan. A personal loan to go on a vacation or a heavy credit card swipe to buy an asset that would depreciate and an auto loan will fall in the bad loan category. They can create debt traps.

Lack of financial knowledge and discipline goes a long way in preventing people from getting into debt traps. It is important to educate people on loans, bad Cibil credit score and other issues in the personal finance space. While personal loan or any other form of non-collateral loan seem to be the most convenient option, not everyone knows the gravity of the problems one might get into.

The following table explains the different types of loans and also weighs your pros and cons:

Here are top good practices to manage your finances better:

Save and then splurge: ‘Pay yourself first’, in other words, make the habit of saving a part of your income before spending. This goes a long way in keeping debts at bay.

Budget:If you go into debt, it’s an indication that you are living beyond your means. Without planning, it can be hard to know just when you are overspending. Drafting a budget for short, medium and long term expenses and tracking it allows you to see in black-and-white where your money goes. Trim your expenses so that the total outflow is less than the income.

Use debit cards: Debit cards are tied directly to your bank account. If you don’t have money you can’t spend on your debit card. Since no credit is extended, you can’t go into debt using your debit card.

Pay off balances monthly: One way to avoid overcharging on your credit card is to allocate money from your bank account before you make any charges. As soon as the charges hit, use the reserved money to pay them off.

Invest smartly: A well researched investment can yield great returns. Keeping abreast with the latest happenings in the financial world also helps one to make smart investments.

By following the above steps, people with bad financial habits can get out of debt traps. By constantly educating oneself and by inculcating financial discipline one can successfully prevent falling into debt.

Source : http://goo.gl/WkpvF9

ATM :: Before you sign as a guarantor for a loan, read this!

Adhil Shetty – CEO BankBazaar.com | Retrieved on 8th Apr 2014 | Moneycontrol.com

From bank’s perspective the guarantor is treated as good as the borrower. In case the borrower does not pay, guarantor has to pay off the loan, failing which his credit score goes for a toss

Indranil is a project manager in an MNC earning about Rs 30 lakhs per annum. He is quite successful in his professional life and married with 2 kids. With a decent bank balance, own house (on loan), a mid-size car and kids studying at good schools, he has “arrived in life”.

His cousin’s son, Srikant, needs Rs 15 lakhs to finance his MBA education. He goes to Indranil to get one of the documents signed as guarantor. Indranil, the ever-loving uncle, signs the papers and hands it over. Things go well, until one day four years later, he receives a call from Srikant’s bank with a demand to pay up the loan since he is the one who guaranteed the loan. Indranil is in a fix. He has no idea what this means and why he should pay. The bank is persistent and Indranilis now contemplating taking the help of a lawyer.

This is a scary situation to be in. Having to pay for being a good Samaritan is not a position that is enviable.

Types of loan where guarantors are needed

Although almost every stream of banking activity has been regulated and standardized in India, nomination of guarantors is one area where banks do not have uniform guidelines. Individual banks have the right to decide upon the requirement of guarantor. Usually banks require one or two guarantors for higher amounts of loan. The amount for which guarantor is required can be from Rs 5 lakhs and upward. It also depends on the credit history and paying capacity of borrowers.Loans requiring guarantors include education loans, house loans, or any other loan where the amount borrowed is high.

The case of default by the borrower

Most of us forget that a guarantor is not only a witness or “someone” who attests the authenticity of the borrower but also guarantees that the person will pay up the loan. A guarantor in effect says that he is backing the borrower financially and guarantees that the loan will be paid back in case the borrower defaults on his payment. Naturally, the guarantor is liable in such a case.

Banks usually wait for a few months before they issue notice to the guarantor about the default by the borrower. From bank’s perspective, the guarantor is treated as good as the borrower. Hence, it is the responsibility of the guarantor to clear the loan. In case he or she doesn’t, the bank treats the guarantor as wilful defaulter. In the above case, if Indranil doesn’t pay up, he will be named wilful defaulter unless his lawyer and bank come up with a solution.

Impact on CIBIL score

Since banks assume no difference between guarantor and borrower in case of default, this impacts the guarantor’s CIBIL score as well as his credit score as reported by other agencies. Remember that when you guarantee a loan, this information is sent to CIBIL and other credit reporting agencies. While this doesn’t harm you at the outset, the issue arises when the borrower defaults.

This means it has negative impact on your CIBIL score if you and the original borrower defaults. Most guarantors do not realise this, though. Naturally, a low CIBIL score will hamper your ability to raise loan in future.

What to know before becoming a guarantor

Today, there is no credit information that is hidden from banks. Almost all banks can access your credit data from CIBIL irrespective of whether you have a relationship with the bank or not. With such increased transparency and availability of information, it is advisable not to become a guarantor unless you know the person well enough. You should assess the capability of the borrower to pay up. For example,if you are ready to become guarantor for education loan, check which college the borrower has selected for admission. It is easier for an IIM or IIT graduate to pay up the loan than someone from a lower ranked school.

Additionally, you should look at the liability of a guarantor in case of default by original borrower. You can get details on this from the bank concerned. However, if there is no information available in the documents or through the lending bank, rest assured that a guarantor is liable to pay up in case of default.

Finally, check the documents needed from you to become a guarantor. Provide only what is required and do not give too much information. For example, if you are becoming a guarantor for a loan of Rs 20 lakhs, don’t show an FD of 1 crore as proof. This may not harm you in anyway, but it is unnecessary to reveal this financial information.

Conclusion

Turning a guarantor may impact your capability to raise loan for yourself. For example, if you have loan of about Rs 30 lakhs for yourself and have become guarantor for another Rs 20 lakhs for someone else, this may have bearing on the amount of loan you can borrow further in future.

However, this is again an area where banks have discretionary power. They can frame their own rules on whether they should consider this fact while approving the loan. It would be advisable to speak with the bank concerned before becoming a guarantor for someone if you have plans for taking a loan yourself.

Source : http://goo.gl/08Vo2V

NTH :: SBI, HDFC Bank, ICICI Bank cut lending rate; home, auto loans to get cheaper

Press Trust of India | Apr 07, 2015 at 08:24pm IST | @ibnlive

Mumbai: Nudged by the Reserve Bank of India, leading banks, State Bank of India, ICICI Bank and HDFC Bank, on Tuesday cut their lending rates. While SBI and HDFC Bank cut rates by a token 0.15 per cent, ICICI Bank slashed its lending rate by 0.25 per cent after the central bank maintained status quo on policy rate but termed as “nonsense” lenders’ claim that cost of funds was still high.

The action of the two banks could have a snowballing effect forcing others to follow suit, a move that can bring relief to corporate and retail borrowers including of home and auto loans.

The lowering of the base lending rate the banks was announced hours after a war of words erupted between RBI Governor Raghuram Rajan and the top bankers, who had appeared reluctant to effect a cut.

After two cuts in three months, the RBI kept the repo rate, at which the central bank lends to banks, unchanged at 7.5 per cent on fears of unseasonal rains impacting food prices.

The cash reserve ratio, which is the amount of deposits parked with the central bank, will remain at 4 per cent. Bank rate has also been retained at 8.5 per cent.

“I do not see an environment where credit growth is tepid, banks are sitting on money and their marginal cost of funding (has) fallen, the notion that it hasn’t fallen is nonsense, it has fallen,” Rajan said.

After his announcement and plain-speaking, leading bankers including SBI Chairman Arundhati Bhattacharya initially maintained that it takes time to lower the lending rates, which could happen in two or three months.

Hours later, SBI took the lead in effecting the rate cut, followed soon by HDFC Bank, whose CEO Aditya Puri had also hinted earlier in the day that it would take some time for rates to be cut by the lenders.

Bhattacharya later said she expected other lenders to follow suit by cutting their rates, as it was a competitive market. She also hinted at lowering of deposit rates.

On possibility of more cuts, she said, “I think there is an elbow room, but it all depends on credit growth pick up. We really want to see that happening.”

Promising an “accommodative monetary policy”, Rajan on his part said rate cuts going forward would depend on favourable macro economic data and whether banks pass on the benefits of two rate cuts so far on 2015.

While industry expressed unhappiness over the status quo on rates, Rajan said the market dynamics will force banks to lower their interest rates, while adding that sooner they cut the rates, better it would be for the economy.

“Comfortable liquidity conditions should enable banks to transmit the recent reductions in the policy rate into their lending rates, thereby improving financing conditions for the productive sectors of the economy,” he said.

Bhattacharya replied to this, saying that “it takes a little time for things to pass through. And, it is not only the cost of deposits that determines this.

“The passing through is also determined by the amount of liquidity, the amount of credit demand and competition which also drives rates up or down. There are very many factors and repo is only one of the factors.”

She also said that Indian banks work differently, as compared to the international banks.

Supporting SBI chief, ICICI Bank’s Chanda Kochchar said it is not just the repo rate change that determines the base rate change, it depends on cost of funds, deposit mix, liquidity situation and also on credit off take.

However, Bank of India chairperson Vijaylaxmi Iyer said, “The impact of reduction in cost of deposit experienced during the last quarter will encourage banks to pass on the benefit to customers. Retail borrowers may see lower EMIs.” RBI has surprised the markets with two rate cuts of 0.25 per cent each outside the scheduled review meetings in 2015, but banks have yet to respond to these policy rate cut by lowering their lending rates.

After the policy announcement, bankers said that most of them will have their asset liability committee meeting week to take a call on interest rates which besides repo rate depends on factors like demand for credit, cost of fund and deposit rates.

“We would see rates coming down as we see easing of interest rate cycle,” Bhattacharya said.

On the reluctance of banks to pass on the benefit of 0.50 per cent rate cut announced by the central bank since January, Rajan said, “We are not looking for a specific number (on the bank rate cuts) and saying unless this happens, nothing more will happen. But we want to facilitate the process of transmission.”

“Given that there has been very little transmission from rate cut so far… we are waiting to see transmission take place… I have no doubt that this will happen. If it happens sooner it is better for the economy,” he told reporters after the announcement of first bi-monthly monetary policy.

“The Reserve Bank will await the transmission by banks of its front-loaded rate reductions… into their lending rates,” the central bank said.

HDFC Bank’s Puri said the base rate cut is a function of the deposit cost.

“If the deposit cost goes down, then there will be a base rate cut. If it doesn’t there won’t be any base rate cut. However we feel between now and June, there should be repricing of cost and that will lead to a lower cost of funds for borrowers,” he said.

On the issue of bad loans, bankers lobby IBA chairman and Indian Bank head T M Bhasin said the lenders are optimistic that coming quarters will be better than the past few years, while other bankers refused to specify saying this is the silent period.

Source : http://goo.gl/V1pNkf

ATM :: How you can ease your parents’ financial burden

Young people lean too much on their parents for financial support. Here’s how you can ease their burden in times of rising expenses and uncertain returns.

By Sakina Babwani, ET Bureau | 25 Nov, 2013, 09.44AM IST | Economic Times

Ask a B-school aspirant, ‘Who will pay for your education?’ In most cases, the answer will be ‘My parents, who else?’ It’s also likely that parents will foot the wedding bills of their 30-something children. Even 40-year-olds take financial help from parents to buy their homes.

Unlike in the West, where people become independent as soon as they cross their teens, Indians never stop depending on their parents. In the West, it’s almost a stigma if a young adult is living with his parents. In India, it is assumed that parents will fund all the needs of their children.

A survey by HSBC shows that one out of every two retirees is funding his children’s needs (see graphic). In fact, 44% of the retirees who had not saved enough gave this as a reason for the shortfall. “Funding dependants in retirement is more common in India than the global average, with 52% funding their children even though they have retired,” notes the study.

This trend seems set to continue: a large majority of working-age people expect to be funding dependants in retirement, with only 29% not expecting to do so.

How you can ease your parents’ financial burden. So deeply ingrained is this attitude that parents consider themselves failures if they are not able to pay for their kids’ higher education, marriage and homes. “Children seldom think of financing their own needs. Only in rare circumstances, if parents are low-income earners, do children look for alternate sources to achieve their goals,” say

But this overburdening can wear out parents financially, especially those who belong to the sandwich generation. Such parents not only have to take care of their children’s needs, but also of their own parents, who typically have no source of income and depend entirely on them.

Our cover story this week tells you how to lessen the financial burden for your parents by saving and investing for your goals on your own. It will act as a breather for your parents, who can focus on their retirement planning by not having to save for you. Here are some tips that will not only ease your parents’ load but also make you financially independent.

Take an Education Loan

Till about a decade ago, school fees and related costs were within manageable limits. Now, however, studying in a public school can skew the household budget. An Assocham study says that the average annual cost of a school going child has risen almost three-fold from Rs 34,000 in 2005 to Rs 94,000 in 2011. According to an ET Wealth estimate, urban middle class parents spend close to Rs 55 lakh on raising a child from cradle to college, and education expenses account for nearly 45% of the total cost.

If they have already spent so much on your education, is it fair to expect your parents to arrange funds for your higher education? Instead, you can opt for a loan with your parent as a co-borrower. You can typically take a loan of up to Rs 10 lakh for studying in India and up to Rs 20 lakh for studying abroad. The interest rates on education loans range from 10% to 18%, depending on the bank and the type of course applied for. The good part is that the interest you pay on the loan is fully tax deductible, so your effective rate of borrowing comes down. The tax breaks are available for up to eight financial years. “An education loan is not only tax-efficient but also inculcates financial responsibility in an individual. The EMI prevents him from blowing up his income,” says Sudhir Kaushik, cofounder and CFO of Taxspanner.com.

Student loans are quite comprehensive as they typically cover costs of admission, tuition, boarding and books. You can start repaying the loan after you get a job or after six months of completing the course, whichever is earlier. However, do remember that if you don’t get a job or default on the payment, your parent, who is the co-borrower, will have to repay the loan.

Start Saving and Investing

The biggest thrill of earning money is the financial independence that comes with it. You don’t need permission from anybody before buying that slick new smartphone or that expensive dress you have been eyeing for weeks. Instead, you just swipe that small piece of plastic in your purse and purchase it. Would it not be great if you could extend this independence to larger items, such as funding your wedding or buying a house? Yes, it is difficult to build a corpus that runs into lakhs of rupees when you barely make Rs 30,000 a month.

However, large corpuses are not built in a day. It requires discipline and patience. If you diligently invest a portion of your income every month, you can build a sizeable portfolio in a few years. For example, even a modest investment of Rs 3,000 a month in a plan that grows at 12% annually would grow to Rs 2.18 lakh in three years. In five years, it would grow to Rs 4.12 lakh. Mumbai-based Akash Bhatia (see picture) has learnt the art of investing even before he has started earning.

“I started by investing a portion of my pocket money in stocks. Though I made a few mistakes, today I am sitting pretty on a corpus of Rs 2.5 lakh,” says the 22-year-old MBA student, who has been investing steadily for the past four years. In fact he was able to pay his course fee of Rs 1 lakh from his own investments.

However, experts believe that stocks are not the best investment option for newbie investors. “You can start with a recurring deposit and then move to mutual funds through the SIP route. Ideally, direct equity investment is for someone who has the time to devote to indepth research and analysis,” says certified financial planner Jayant Pai. If you haven’t started earning and your pocket money is too low, consider taking up a part-time job. It will not only help you earn some money but you will gain practical experience, which could prove invaluable in your career.

Share Household Expenses

If you are living with your parents, it’s only fair that you contribute to the household expenses. Your parents may not ask you to contribute and even dissuade you from doing so, but given that they are close to retirement, you should shoulder a significant burden of the monthly household expense.

Remember, if you allow your parents to save more for their retirement, it will lessen your own burden when they stop working. Paying rent to your parents is perhaps the most tax-efficient way of contributing to the expenses. If your employer offers you a house rent allowance as part of your compensation, you can claim exemption for the rent paid.

However, this is possible only if the property is registered in the name of your parent. The owner will be taxed for the rental income after a 30% deduction. So, if you pay your father a rent of Rs 3 lakh a year (Rs 25,000 a month), he will be taxed for only Rs 2.1 lakh.

It gets better if the property is jointly owned by both parents. Then you can divide the rent between them so that the tax liability is split between them. If their income exceeds the basic exemption limit, you can help them save tax by investing in their name under Section 80C options, such as the Senior Citizens’ Saving Scheme, five-year bank fixed deposits or tax-saving equity mutual funds.

Pune-based IT professional Satyam Chawla (see picture) lives in his father’s house and pays him rent while his own residence has been rented out. “In this manner, not only is my father financially independent, but I can take care of him as well,” he says.

Some parents may not agree to take money from their children. So, the helping hand will have to be subtle. Buy health insurance for them, which is a real need for people heading for retirement. It also helps you save tax. Up to Rs 15,000 paid as premium for the health insurance of parents can be claimed as a deduction under Section 80D. If any of the parent is a senior citizen, the deduction is higher at Rs 20,000. This is over and above the Rs 15,000 deduction for your own family. Also, this deduction is available irrespective of whether parents are financially dependent on the taxpayer or not.

Be Open to Reverse Mortgage

Too many parents are not able to save for retirement because they allocate too much of their resources to their children’s needs and in building a house. If your parents are also asset-rich but cash-poor, reverse mortgage can unlock the value of their property.

In such an option, the bank pays a monthly amount to the owner of the house. With each payment, the bank’s ownership of the property increases. After the death of the owner, his legal heirs can either repay the loan, along with the interest, or let the bank sell the property. The bank will deduct the borrowed amount from the sale proceeds and give the balance to the heirs. The option of reverse mortgage is only available to senior citizens and they should be living in the house.

Reverse mortgage is a good way of earning an income by unlocking the value of real estate without selling it. But many youngsters oppose any such move by their parents because it imposes a liability on them. They don’t realise that the property is not being sold but is only partially mortgaged. Even if the parents take a monthly income of Rs 20,000 from the bank, it will take them 4-5 years to rack up a loan of about Rs 12 lakh.

However, it will allow the parents to live a life of dignity and financial freedom. Besides, they won’t have to lend financial support to their parents if they have a monthly income. Be open to the idea of reverse mortgage and explain the concept to your parents. A small tip: it’s good to involve all the stakeholders in such discussions lest a sibling feels that you are trying to sell the property.

Can children be sued for not caring for parents?

The law ensures that seniors are not left in the lurch.

THE SIMPLE answer is ‘yes’. Under Section 125 of the Criminal Procedure Code, 1973, and Section 5 of the Maintenance and Welfare of Parents and Senior Citizens Act, 2007 (MWPSC Act), parents can sue their children if they do not maintain them in their old age. However, this is applicable only if parents do not have any source of income to support themselves. A senior citizen can even sue a grandchild or any legal heir, provided he is not a minor.

The MWPSC Act goes a step further in protecting their rights. If a senior citizen has gifted his property on the condition that his child or relative will take care of his needs and the child goes back on his word, the transfer shall be considered as made through fraud or coercion and, hence, will be considered void. In 2012, 74-year-old M Jagadeesan of Madaraalli district in Tamil Nadu filed a complaint that his son, Anbarasan, had driven him out of the house.

After an inquiry, the district police was asked to assist Jagadeesan in getting his property back. While the law protects the rights of senior citizens, it also does not ignore the rights of creditors. If a borrower dies without repaying a loan, his children cannot be forced to pay. However, any asset belonging to the deceased person will be liquidated to repay his debts.

Source : http://goo.gl/IUFDwE

ATM :: 11 easy steps to get out and stay out of debt

K. Ramalingam | Updated On: August 05, 2013 11:52 (IST) | NDTV Profit

In spite of steady, regular income there are so many individuals who live paycheck to paycheck, carry their credit card outstanding, and fail to save anything for life after retirement. If you are one of them, now is the right time to take action to come out and stay out of debt.

It is not only possible but also very much achievable.

Discussed below are a few easy steps you can use to get out of debt:

1. Make a list of all your debts

You need to take a good look at all your loans. It could be credit card dues, personal loan, car loan, housing loan, education loan, loan from FD, loan from insurance policies, loan from your employer, hand loan, and so on. For each and every loan you need to note down basic details like how much you owe, the current interest rate, EMI amount, number of months (tenure) etc.

2. Negotiate for lower interest rates

If you could negotiate the interest rate and bring it down, you can come out of debt faster. Most of the credit card companies come forward for negotiation if you show interest in repaying. They need not run after you to collect the debt. They will be happy to negotiate as this will, in fact, reduce their expenses. Balance transfer offers from credit cards are also a good way to reduce your interest rate.

3. Refinancing and consolidation

Replacing a loan with another is known as refinancing. Getting a refinance should reduce your interest rate and bring down the time you are in debt. But people more often go for a refinancing option that provides them with lower EMIs, increasing, however, the time they stay in debt.

4. Categorise your debt

A house loan can increase your net worth over a period of time. This kind of loan gives you tax benefit also. For a businessman, car loan provides some tax benefit. Each one of your debts needs to be categorised based on such factors. This will help us in comparing different loans.

5. Prioritise your debts

After sorting out various loans, you can comfortably prioritise them. This will be based on the interest rates and tax benefits. At times paying off a small loan first can give you a lot of motivation to get out of your overall debt.

6. Creating and executing a debt payoff plan

You need to create a debt payoff plan with different scenarios, so that you can find out how some more savings or a different repayment order will help you to get out of debt faster. When creating a plan, you need to choose one which is comfortable to your attitude. Otherwise, you may not be able to execute it properly.

7. Keep yourself from taking fresh loans

You need to make a vow that you will not be adding any fresh loans until you come out of all your debts completely. Think, for a moment, how you will feel when you become debt free as this will give you a lot of positive energy to come out and stay out of debt.

8. Postpone buying major assets

Buying property or any other major asset needs to be postponed until you get rid of your debt. With your new ownership comes the new – probably large – and unpredictable expense. This can make you deviate from your debt payoff plan and, at times, make you bear unpleasant and uncontrollable consequences.

9. Stop using your credit card

When it comes to using credit cards, there are broadly two kinds of people: 1) who use credit cards responsibly; and 2) who don’t. Poeple of the responsible kind repay their credit card dues in full on receiving the bill. The other kind, however, would pay the minimum due amount and carry forward the remaining sum.

If you belong to the second group, you need to stop using credit cards – at least – temporarily. Take out and put your credit cards in a locker. You can start using them again once your financial situation and buying habits improve.

10. Change your spending habits

Being in debt obviously means that you have been living beyond your means. The solution is very simple: spend less and you will get out of all your debt soon. You need to change your spending habits. If you buy things you don’t need, you soon end up selling things that you do need. Don’t save what is left after spending; instead, spend what is left after saving.

11. Involve your family members

You need to inform all your family members and dependents about your debt status. This way, you will be able to take decisions with much more clarity. Moreover, if your family members know about your debt, they will also change their spending habits and support you in getting out of debt faster.

Consider the example of a postage stamp. The usefulness of a postage stamp lies in the fact that it sticks to one thing till it reaches its destination. Similarly, you need to stick to your debt pay off plan till you get out of it.

K. Ramalingam is a certified financial planner and the founder and director of Holistic Investment Planners. The opinions expressed here are the personal opinions of the author. NDTV is not responsible for the accuracy, completeness, suitability or validity of any information given here. All information is provided on an as-is basis. The information, facts or opinions appearing on the blog do not reflect the views of NDTV and NDTV does not assume any responsibility or liability for the same.

Source : http://goo.gl/hsmKSL

ATM :: 10 tips for students heading abroad

Deepa Venkatraghvan | Jul 26, 2013, 06.09PM IST | Times of India

Congratulations! You’ve secured admission in an educational institute abroad and are all set to make the big move. Before you go, here are a few tips you must keep in mind:

How much fees the RBI allows you to remit

The RBI regulation states that ‘for studies abroad the estimate received from the institution abroad or $100,000 per academic year, whichever is higher, may be availed of.’ So you can freely remit an amount of up to $100,000 per annum from India towards the tuition fees. If your fees exceed $ 100,000 per annum, then you need to take a letter from the foreign college giving the estimate of fees. You can remit the amount mentioned in the letter without taking permission from the Reserve Bank or any other authority.