Tagged: Provident Fund

ATM :: How to withdraw 90% of your provident fund to buy a house

May 12, 2017 | 11:39 IST | SOURCE : Economic Times | Retrieved from Timesnow.tv

In an effort to make its ‘Housing for all by 2022’ a success, the government has allowed for EPFO members to withdraw up to 90 percent of their provident fund (PF) accumulations to make down payments to purchase a house and to pay housing loan EMIs.

Pre-requisites for PF withdrawal

In order to dip into the provident fund saving, the new rule highlights that the PF holder will only be eligible if he/she has been a contributing PF member for at least 3 years, and is buying property in a registered housing society that has at least 10 members.

Further, the property has to be purchased in the member’s name and cannot be purchased jointly with anybody else, except your spouse.

How the money can be used

The money withdrawn can only be used for an outright purchase, as a down payment for a home loan, for buying plots or for the construction of a house. The transactions can be made through central government, state government and even from a private builder, including promoters or developers.

Can the money be used to buy resale flats as well?

Unfortunately no, EPFO will only make payments directly to a cooperative society, the state government, central government, or any housing agency under any housing scheme, or any promoter or builder, in one or more installments. The rule will not apply to real estate purchases in the secondary market or resale transactions.

Can you withdraw both employee and employer contribution?

An EPFO member can withdraw his own share of PF contribution plus interest as well as the employer’s share of contribution plus interest.

Can you EMI payment through PF?

A PF member can use his PF contribution to pay full or part EMIs for a home loan taken in the member’s name. The EMI will be directly paid by EPFO to the government, housing agency or the bank.

How to apply

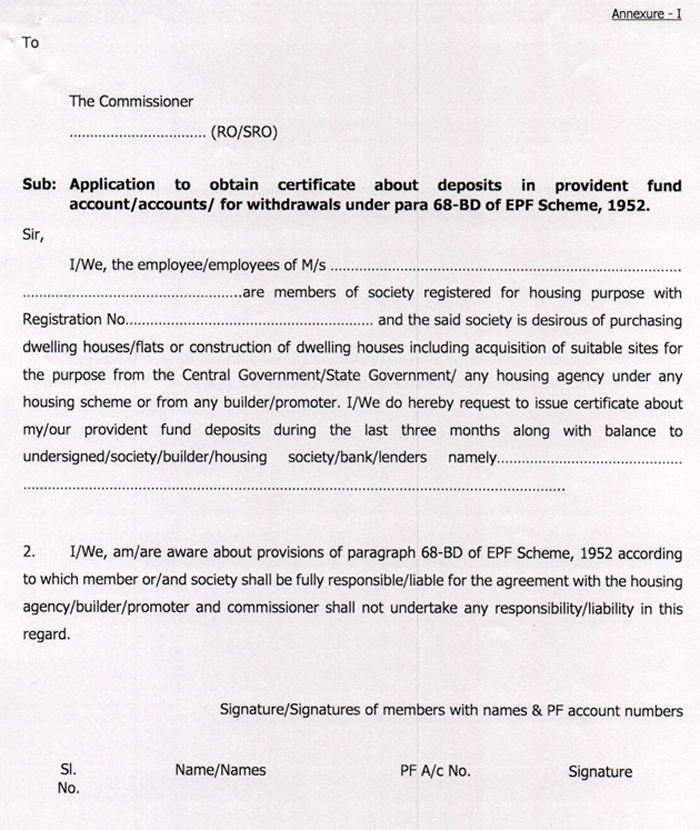

A PF member can apply individually or jointly through a housing society to get a certificate from the EPFO.

Through Annexure I form, an employee can ask for the balance and the deposits made in the last three months before applying. This will help the EPFO determine how much EMI can be arrived at.

Also, the employee has to mention the name and details of the bank or housing society to whom such certificate is to be issued.

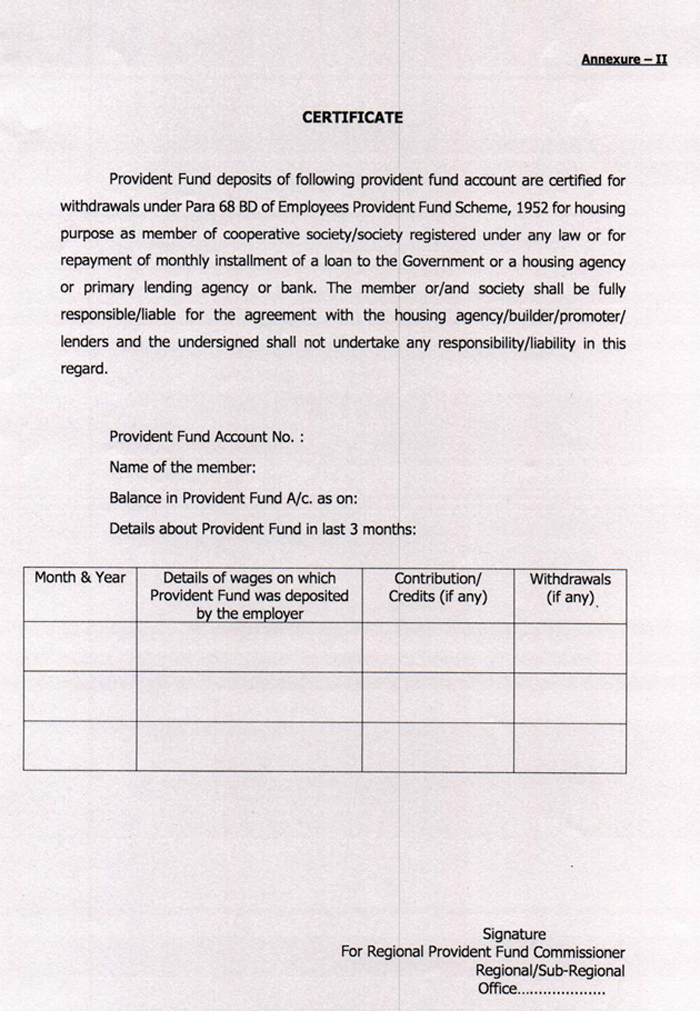

The EPFO then issues a certificate showing the outstanding balance and last three month’s deposit in the account. Alternatively, members can take printouts of their PF passbook downloaded from the EPFO website and submit it to housing agencies or banks.

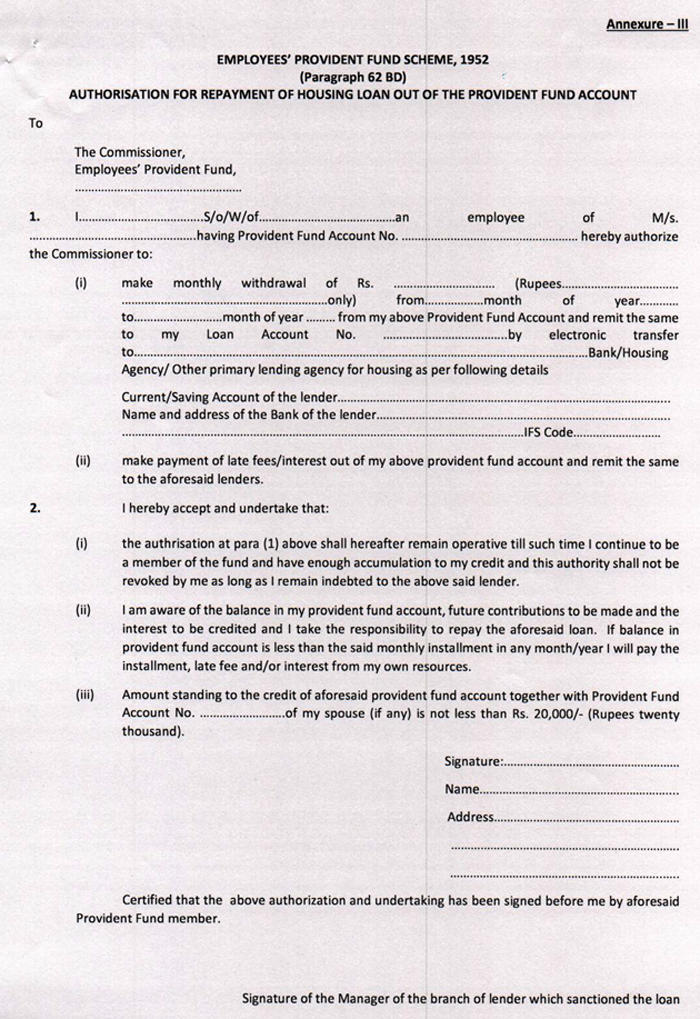

If a member wishes to use PF money to meet EMI’s, then in addition to Annexure I, an authorisation by the member is to be filled in a prescribed format. It will carry details such as PF amount, PF and loan account number, lender name, address etc. One has to get this form authorised from the lender i.e. branch manager of the lender who has sanctioned the loan. Once approved, EPFO will start transferring EMI’s online to the lender’s account.

What if an employee leaves his/her job?

The EPFO has made it clear that under no circumstances would it be liable for any default of payments to the lender. The EPFO will not be party to any agreement made between an EPFO member and a society or builder.

In case a member quits his job, the responsibility of repaying the loan would rest with the employee and not the EPFO.

Conclusion

While dipping into your PF account to make a down payment makes your life easier, it is important to remember, your PF is meant to take care of your post retirement needs, and depleting it may jeopardise your retirement.

So make sure you have a backup plan to meet postretirement needs through equity mutual funds or PPF.

Source: https://goo.gl/egUXjH

NTH :: PF interest rate hiked to 8.8% for 2015-16 from existing 8.75%: Bandaru Dattatreya

The government on Tuesday increased interest rates on provident fund (PF) to 8.8 per cent for the ongoing financial year ended March 2016 from 8.75 per cent earlier.

By: FE Online | New Delhi | February 17, 2016 10:16 AM | FinancialExpress.com

EPFO provides the rate of interest from its earnings on investment on formal sector workers’ fund without any assistance from the government. (AP)

The government on Tuesday increased interest rates on provident fund (PF) to 8.8 per cent for the ongoing financial year ended March 2016 from 8.75 per cent earlier.

EPFO has been paying 8.75 per cent interest rate for the last two fiscals to its 5 crore organised sector subscribers.

“PF interest rate is hiked to 8.8 per cent for 2015-16 from existing 8.75 per cent,” said Labour Minister Bandaru Dattatreya on Tuesday. “We had last time given 8.75 per cent and this time, seeing the situation, we are declaring 8.8 per cent for the workers,” he told reporters after chairing the 211th meeting of the Central Board of Trustees (CBT) of the Employees’ Provident Fund Organisation (EPFO).

The trade unions had demanded that the interest rate be fixed at 8.90 per cent, the government had revised it to 8.80 per cent, he said, underlining the Centre’s commitment to the working class.

EPFO provides the rate of interest from its earnings on investment on formal sector workers’ fund without any assistance from the government. The income projection of the retirement fund body is upwards of Rs 34,844 crore for the current fiscal. At this, EPFO would not have any problem to raise the rates to even 9% considering that it would still have Rs 100-odd crore surplus.

Source : http://goo.gl/M5GRI6

NTH :: PF may be withdrawn online from August

PTI|11 Feb, 2016, 04.19PM IST | Economic Times

NEW DELHI: Retirement fund body EPFO may launch by August an online facility to withdraw provident fund, a move that will reduce paperwork and provide hassle-free service to its subscribers.

With the new facility, settling PF withdrawal claims would just take few hours.

“We are hopeful of launching an online facility for PF withdrawal claims by August this year. We have already digitised our records and processes using Oracle operating system,” a senior EPFO official told PTI.

“EPFO will soon buy blade servers for setting up three Central Data Centres at Gurgaon, Dwarka (Delhi) and Secunderabad. All the three centres will be connected to 123 offices of the Employees’ Provident Fund Organisation (EPFO),” he said.

The process of procuring servers would be completed by May while the testing would start in June to gauge the response of the system in place.

“After intensive testing and trials in June and July, we are planning to launch the online PF withdrawal facility in August this year,” the official said.

Once this is operational, subscribers can apply online for PF withdrawal, which will be transferred directly to their bank accounts.

At present, subscribers who wish to settle their accounts with the EPFO are required to apply manually.

For settling online claims, the subscribers would have to activate their Universal (portable PF) Account Numbers which are seeded with KYC details including bank accounts, Aadhaar number and permanent account number.

The EPFO has over five crore subscribers.

As many as 6.15 crore UANs were issued by EPFO out of which 2.34 crore have been activated by the subscribers so far.

Source : http://goo.gl/Nf7HsB

NTH :: Interest rates on small savings schemes like PPF may be reset every quarter

By Deepshikha Sikarwar, ET Bureau | 23 Jan, 2016, 10.31AM IST | Economic Times

NEW DELHI: Interest rates on popular small savings schemes such as Public Provident Fund (PPF), National Savings Certificate (NSC) and the Kisan Vikas Patra could soon be reset every quarter as part of the government’s plan to peg them closer to market rates to reduce market distortions and help the cause of lower interest rates.

The government will also reduce the mark-up over the benchmark government bond rate for such schemes of small maturities to nudge short term rates lower.

High interest rates on small savings schemes have long been cited as a structural barrier to interest rates coming down as they compete with bank deposits, but are not subject to the same kind of market pressures as them. Because they stay high, bank deposit rates are forced to remain high and therefore prevent lending rates from coming down.

A senior government official said the first reset under the new rules will happen from April 1 this year and rates are expected to fall. A notification will be issued soon, this official said, adding that interest rates on schemes for senior citizens and a scheme for girl children were not likely to be revised.

Small savings’ interest rates are linked to yields on government bonds of comparable tenure, but unlike gilts that are traded daily and see yields change, these change only sparingly.. The last revision in rates on these schemes was on April 1last year. Since then, market rates have moved south following a 0.75 percentage point policy rate cut by the Reserve Bank of India, creating a wide wedge between what the banks can offer and what is available on small savings.

State Bank of India, for example, offers 7 per cent on deposits of maturity of five years or more. Deposits of such tenure fetch 8.5 per cent in a post office small savings account. The PPF rate for a similar maturity is 8.7 per cent. This wide gap between small savings’ and market rates impacts deposit mobilisation by banks as their ability to reduce deposit rates is adversely impacted. This impacts banks’ ability to lower lending rates as well.

A quarterly reset of small savings rate will ensure that distortion in the rates caused by the small savings is kept to a minimum, officials said. The weighted average yield of dated government securities was 7.9 per cent in April-September 2015 compared with 8.81 per cent in the first half of the preceding year, potentially opening up the possibility of an up to one percentage point reduction in the small savings rate.

In their pre-budget meeting with Finance Minister Arun Jaitley earlier this month, banks and financial institutions had also suggested quarterly benchmarking of rates.

Source : http://goo.gl/LBLfSt

NTH :: Here’s how your provident fund may earn higher interest rate this fiscal

Interest rates of provident fund might increase to 8.95% from 8.75% earlier

DNA WEB TEAM | Fri, 22 Jan 2016-09:47am , Mumbai , dna web desk

The interest rates of provident fund might increase to 8.95% from 8.75% earlier. The Employees Provident Fund Organisation’s (EPFO) finance panel has recommended the increase in interest rates on statutory savings of over 5 crore subscribers to 8.95% in the current fiscal, according to a leading news agency.

The central board of trustees have endorsed the proposal and is yet to get the finance ministry nod. If the proposal is approved then it will be the highest return since 2011 when the interest rates were 9.5% and the highest ever real interest rate, said the report.

The 8.95% interest rate will translate into returns of nearly 12% for the highest slab as withdrawals and interest earnings do not attract tax at the time of withdrawal.

The government and the Reserve Bank of India (RBI) are looking at reducing deposit rates in order for banks to cut lending rates and push investment. The move to increase the interest rates on EPF deposits may result in a diversion of bank discounts or other small saving schemes.

The finance ministry is expected to lower the interest rates on many small savings schemes by up to 50 basis points.

The EPFO’s, which is a basic investment for many employees, increase in interest rates might face some resistance from the finance ministry. However, it might go through as the middle class depends on it for savings.

Source: http://goo.gl/IIbZf7

NTH :: EPFO Insurance Scheme – Hassle free: Nominee entitled for benefits, irrespective of cause of death

Here’s all that you should know about the employee deposit linked insurance scheme.

Written by Adhil Shetty | Published:Dec 11, 2015, 2:00 | Indian Express

Not many investors know that the retirement benefits administration body Employees’ Provident Fund Organisation (EPFO) offers an insurance scheme covering all employees working with organisations as part of the EPF.

Along with the Employee Provident Fund and the Employee Pension Scheme, the Employee Deposit Linked Insurance (EDLI) forms the troika of the social security schemes administered by the Employees Provident Fund Organisation.

Here’s all that you should know about the employee deposit linked insurance scheme.

What is Employee Deposit Linked Insurance?

Employee Deposit Linked Insurance is a term insurance plan offered by the EPFO. The scheme offers life coverage for all employees working with the organised sectors and enrolled in EPF. The scheme is administered by the Employees Provident Fund Organisation and is applicable to all companies who are part of the EPF.

The EDLI scheme works just like a group term insurance plan where if an employee dies during the service period, his family or nominee gets the sum assured up to a certain maximum limit as defined by the rules of the EDLI scheme.

Protection coverage under the EDLI scheme

Being a group term insurance plan, EDLI offers a 24-hour-protection to the employees as part of the scheme. This means the insured does not need to be at their workplace for the scheme to be valid or applicable. The scheme protects them 24×7 irrespective of whether they are at work or not.

The coverage and premium charges under the EDLI scheme are the same for every employee irrespective of any factor including age or gender.

Employees contribute 0.5 per cent of their monthly basic pay and dearness allowance (capped at a maximum of Rs 15,000) as premium for this, and the coverage is linked to the premium.

The family or nominee of the policyholder (employee) under the EDLI scheme will get benefits irrespective of the cause of death including illness, accident, or natural causes.

EDLI earlier had stipulated 12 months of service with the same employer as a mandatory condition for being protected under the insurance scheme. Now, there is no such minimum limit of service and employees are covered under the EDLI scheme as soon as they start working with a company.

Extent of claim available

As per the recently issued EPFO guidelines, the maximum claim amount is capped at 30 times of the last drawn salary of the policy holder. Along with the claim amount, EPFO also offers a bonus of Rs1.5 lakh for each claim.

So the maximum claim amount you can avail under the EDLI scheme is therefore calculated as 30 times Rs 15,000 plus the Rs 1.5 lakh bonus, which comes to Rs 6 lakh. The previous limit was Rs 3.6 lakh only.

How to file for a claim

Before you opt for a claim under the EDLI scheme, make sure that you have all the required documentation in place. You will need:

* Death certificate of the employee as issued by the local municipal corporation.

* Legal heir certification or succession certificate.

* If the employee was working with a company exempted under the EPF Scheme 1952, the employer will need to submit the PF details of last 12 months.

* Once you have all the documents in place, you will need to submit the EDLI claim form. The form is available at: http://www.epfindia.gov.in/site_docs/PDFs/Downloads_PDFs/Form5IF.pdf

You should also submit Form 20 and Form 10D / 10C to claim provident fund dues. Before submitting the claim form, you will need to get it attested by the employer.

Source : http://goo.gl/H6OSfl

NTH :: After EPFO, smaller pension funds set to invest in stocks

TNN | Sep 3, 2015, 06.25AM IST | Times of India

The government, with an objective of creating a credible counterbalance to foreign funds in the stock market, is getting several smaller pension funds controlled by it to follow the Employees’ Provident Fund Organisation (EPFO) to invest part of their corpus in the stock market. Last month, for the first time in its 64-year history , EPFO, which manages over Rs 8.5 lakh crore worth of funds for salaried employees, started investing 5% of its incremental inflows (about Rs 400 crore per month) in stocks.

“Coal Miners Pension Fund, Seamen’s Provident Fund Organisation, Assam Tea Planters’ Fund, Jammu & Kashmir employees’ pension fund and several other such funds are now talking to Sebi for investing in stocks,” a senior Sebi official said.”The overall strategy for the government, to get domestic pension funds to invest in the equity market, is to have in place an institutional money pool which could be a counterbalance to FPIs,” the Sebi official said. FPIs, or foreign portfolio investors, mainly constitute foreign institutional investors (FIIs) and also include foreign individual investors and other investors of non-Indian origin.

Such a strategy to create a large pool of domestic institutional investors is necessitated by the fact that often, because of domestic or global factors that could be fundamental or technical in nature, foreign funds start buying or selling in the Indian market. This, in turn, leads to substantial volatility in the Indian market. To check such abrupt and sharp volatility , the government wants to have in place a large pool of long-term domestic institutional money , the Sebi official said.

As of now, mutual funds have around Rs 3 lakh crore in equities while another Rs 5 lakh crore is with insurance companies and other institutions. The combined equity investment figure of these domestic institutions nearly equals the total equity holdings of FPIs. Yet, selling by FPIs leaves a major impact on the stock market because they can take money out of India while domestic institutions cannot. The government wants a cushion that is able to balance out selling by FPIs even on a major scale.

Last month, EPFO started investing in the stock market through two of SBI Mutual Fund’s exchange-traded funds (ETFs), one each on nifty and sensex indices. To tap the long-term pension money from these PF funds, mutual fund houses are also launching ETFs, with UTIMF being the latest to open a sensex and a nifty ETF. LICMF and IDBI Bank have also filed their documents with Sebi.

Although EPFO has the leeway to invest up to 15% of its incremental corpus in stocks, it has started with 5%.Fund industry players said that other smaller PFs, which are also talking to Sebi to start investing in the stock market, will not take any extra risks in such investments and follow the EPFO model and stick to 5% now.

Source : http://goo.gl/ZZjpjs

NTH :: Take-home salary to take a hit after changes in PF Act

Ministry for deduction of provident fund on house rent, gratuity, other allowances along with basic wage.

Written by Surabhi | New Delhi | Published on:May 21, 2015 2:49 am | Indian Express

Your take-home salary is set to see a sharp cut with a labour ministry proposal to include house rent, gratuity, traveling and other allowances as part of the “contributing wages” on which provident fund would be deducted.

The proposal is part of the final amendments of the Employees’ Provident Fund and Miscellaneous Provisions Act, 1952, that has also sought to increase PF deductions to 12 per cent of the contributing wages from the current rate of 10 per cent.

These amendments have already been cleared by the EPFO’s Central Board of Trustees and are expected to be taken to the Union Cabinet by next month and tabled in Parliament in the Monsoon Session.

The proposal is a significant change from the current practice, wherein PF is deducted only on the basic wages. Under the new proposal, even contributions to the related Employees’ State Insurance Corporation will be part of the “contributing wages” on which PF will be deducted.

The proposal comes due to the different wage structures followed by establishments and High Court rulings. “To bring uniformity and transparency in the calculation of contribution payable by the employers, the definition of the contributing wages is proposed to be included. Specific details of allowances included or excluded for the purpose of PF contribution have been mentioned to avoid any ambiguity,” said the labour ministry.

It has also called for a significant expansion of the coverage of the scheme to include establishments with up to 10 workers, all types of establishments as well as all kinds of employees including those on contract and apprentices.

“The definition of employee has been broadened to include all types of workers including contractor workers and apprentices,” said the ministry, adding it would include those who “receive their wages directly or indirectly from the employer”.

Similarly, the term “establishment” would be expanded to include “any organisation, institution, corporation, local body, company, co-operative society, trusts, self help groups or any other legal entity employing one or more person.”

However, a special provision has been included for reducing the rate of contribution for establishments employing less than twenty person.

Following up on the Budget announcement, the draft amendments have also proposed to give a one time chance to members of the EPFO to switch to the National Pension System.

Doing away with the prescribed retirement age of 58 years for the EPFO scheme, the amendments, which were finalised by the labour ministry after meetings with trade unions and employer representatives, have said that it will now be decided by the Central government.

But providing relief to firms facing hard times, the draft amendments have sought to empower the government reduce or waive contribution in case of establishment or class of establishments.

It has also defined unorganised sector workers for the purpose of the proposed unorganised sector workers’ fund.

Source : http://goo.gl/71oj3L

NTH :: Affordable housing scheme for EPFO subscribers in offing

PTI | Jan 4, 2015, 02.20PM IST | Economic Times

NEW DELHI: The Labour Ministry is preparing a mega housing scheme to offer affordable houses to over 5 crore subscribers of retirement fund body EPFO in the backdrop of the government’s mission ‘Housing for all by 2022′.

The Ministry intends to collaborate with PSU banks, housing finance companies, state-owned construction firms like NBCC and authorities like DDA, PUDA, HUDA to build houses at a price to be fixed by the government.

“Labour Ministry is preparing a scheme under which affordable houses will be provided to the Employees’ Provident Fund Organisation (EPFO) subscribers, particularly those who are in the low income bracket,” a source in the ministry said.

At present, there are over 70 per cent EPFO subscribers whose basic wages are less than Rs 15,000 per month.

In a recent note, the Prime Minister’s Office had asked EPFO to promote affordable housing for its subscribers and use its funds for the purpose.

According to the note, deployment of 15 per cent of EPFO funds as loan for low cost housing would generate a credit flow of Rs 70,000 crore and can create 3.5 lakh additional low-cost homes.

EPFO currently manages a huge corpus of Rs 6.5 lakh crore and its annual incremental deposit is in excess of Rs 70,000 crore.

The Labour Ministry is keen on a scheme under which EPFO subscribers could withdraw their PF deposits to make part-payment of the total cost of the house.

At present, EPFO subscribers can withdraw money from their PF accounts for buying houses only after contributing for a period of five years in the schemes run by the body.

The Ministry also intends to provide subsidy to the EPFO subscribers in low-income bracket to help them avail benefits of various low-cost housing schemes of the government.

Financial institutions, sources said, would be roped in to provide housing loan at low interest rates under the priority sector lending for construction of affordable houses under the scheme.

The scheme, however, will be optional for EPFO subscribers as there is no need to provide affordable houses to those who already own one.

Under the housing scheme, there would three different income categories–Low Income, Middle Income and High Income. Houses and financial incentives under the scheme will be offered on the basis of the income of a subscriber.

The subscribers would be facilitated to pay equated monthly instalments of the their home loan through their provident fund account.

The source said that under the scheme EPFO may use its funds to create a corpus for provide housing loan at affordable interest rate to its subscribers.

Source : http://goo.gl/UgHGHP

ATM :: Will your provident fund be enough?

The PF can be an important pillar in a retirement plan, but one needs to make additional investments to build a corpus big enough to sustain one’s expenses for 20-odd years after retiring.

Preeti Kulkarni, TNN | Nov 24, 2014, 07.10AM IST | Times of India

If you dream about a comfortable retirement but are planning to depend solely on your Provident Fund (PF) to meet your needs, be ready for a shock. The PF can be an important pillar in a retirement plan, but the corpus of the average subscriber is likely to fall woefully short of his requirement.One needs to make additional investments to build a corpus big enough to sustain one’s expenses for 20-odd years after retiring.

To be fair, the Provident Fund’s design makes it the most effective way to save for retirement. You start contributing from the very month you start earning, and since it is a compulsory saving, you can’t avoid it. Besides, your contribution is linked to your income and rises with every increment in your salary. If a person takes up a job at the age of 25, even a modest contribution of Rs 5,000 a month and a matching contribution by his employer can build up a massive corpus of Rs 6.89 crore over 35 years. This calculation assumes that his income (and, therefore, the contribution) will rise by 8% every year and the PF will give 8.5% returns.

While the figure of Rs 6.89 crore may appear huge, it may not be enough. If you need Rs 50,000 a month for living expenses today, a 7% inflation would push up the requirement to roughly Rs 5.34 lakh a month in 35 years. When you are 60, you would need a corpus of Rs.10.52 crore to sustain inflation-adjusted withdrawals for the next 20 years. Assuming a post-tax return of 8.5% and 7% inflation, the Rs 6.89 crore from the PF would be completely wiped out in a little over 12 years. This could mean having no money in your retirement account at the age of 72.

There’s another problem. To make your PF work for you, you must remain invested for the long term. However, a lot of people withdraw their PF when they change jobs, thus losing out on the power of compounding. “In India, the PF is often used for other purposes, particularly when people change jobs. They end up withdrawing this accumulated corpus to buy expensive gadgets or go on a holiday, forgetting that the purpose was retirement planning,” says Arvind Usretay, India Retirement Business Leader, Mercer. A recent global survey by Mercer has ranked India’s retirement system the lowest among the 25 countries surveyed.”What continues to hold India back is the lack of retirement coverage for the informal sector and less than adequate retirement income expected to be generated from contributions made to the Employees’ Provident Fund (EPF) and gratuity benefits,” notes the Mercer study.

Another global study by Towers Watson points out that a significant majority of employees sees their employer retirement plans as the most important source of income in retirement. “Employers must educate their employees on the need for retirement planning and provide them the tools to help them save adequately,” says Anuradha Sriram, director, benefits, Towers Watson, India.

To ensure a comfortable life in retirement, one needs to make additional investments to build a corpus big enough to sustain one’s expenses for nearly 20 years in retirement. Here are a few options you can consider.

Mutual funds

Mutual funds are, perhaps, the best way to supplement your retirement savings.Among these, equity mutual funds have the potential to give very high returns, but also carry high risk. They are best suited to younger investors who can withstand short-term volatility to earn long-term gains. “Equity funds should be the instrument of choice for young investors who have 25-30 years to build a retirement kitty,” says Suresh Sadagopan, founder of Ladder7 Financial Advisories. An additional advantage of investing in equity funds is that the gains are tax-free.

If you are averse to taking risks, consider a balanced fund, where the eq uity exposure is lower. Ultra cautious investors can go for MIPs of mutual funds that invest only 15-20% of their corpus in stocks and put the rest in bonds. However, the returns of MIPs will not be able to match those of equity and balanced funds.

Ulips

Ulips have earned a bad name because of the rampant mis-selling in the past.However, this much reviled product can be a good option for retirement planning.In recent months, insurance companies have come out with online plans that levy very low charges. The Click2Protect plan from HDFC Life charges an annual fund management fee of 1.35%, which is less than the direct mutual fund charges. The Bajaj Allianz Future Gain plan does not levy premium allocation charges if the annual investment is Rs 2 lakh and above. The Edelweiss Tokio Wealth Accumulation Plan doesn’t have policy administration charges. Some Ulips, such as Aviva i-Growth and ICICI Prudential Elite Life II, don’t have lower charges but compensate long-term investors with ‘loyalty additions’. The best part in a Ulip is that one can shift money from debt to equity, and vice versa, without incurring any tax liability. The corpus is also taxfree on maturity.

Unit-linked pension plans

Unlike Ulips, unit-linked pension plans are not a very good option. Although they work like Ulips during the investment years, the rules at the time of maturity are different. You can withdraw only 33% of the corpus on maturity and the balance must compulsorily be used to buy an annuity . The pension from the annuity is fully taxable as income, so these plans are not tax-efficient. Besides, they have very high charges in the initial years, which eat into the returns of the investor.There is no online unit-linked pension plan on offer.

NPS

The New Pension Scheme offers greater flexibility to investors than the unit-linked pension plans from insurance companies. The charges are also very low. The investor can choose from six pension fund managers. He can also switch to another fund manager once in a year. The best part about the NPS is the lifestage fund. Under this, the asset allocation is linked to the age of the investor. The exposure to a volatile class like equity is progressively brought down as the person gets older. “It is a well-planned pension product and facilitates automatic lifecycle-based investment option, making it attractive even for those who may not be financially savvy ,” says Usretay. The drawback of this scheme is that the equity exposure is capped at 50%, and 40% of the corpus must mandatorily be put into an annuity to earn a pension. As mentioned earlier, the pension income is fully taxable.

Traditional insurance policies

They offer tax-free income and insurance cover, but traditional insurance policies are not the best way to save for retirement.The returns are quite low at 6-7%, and the investor has very little flexibility . The PPF, which offers the same tax benefits, may seem like a better alternative. If the annual ceiling of Rs 1.5 lakh in the PPF is a problem, you can contribute more to your PF through the Voluntary Provident Fund.

Apart from making additional investments for retirement, you need to plan for emergencies as well. An unexpected event can derail your financial planning.”Build a contingency fund for financial emergencies and buy adequate life and health insurance,” says Sudipto Roy, managing director, Principal Retirement Advisors. The contingency fund should be big enough to take care of six months’ expenses.

Source : http://goo.gl/pClWsT

ATM :: Retire rich: Supplement your Provident Fund with other high-yielding options

Preeti Kulkarni, ET Bureau Nov 10, 2014, 01.34PM IST | Economic Times

If you dream about a comfortable retirement but are planning to depend solely on your Provident Fund (PF) to meet your needs, be ready for a shock. The PF can be an important pillar in a retirement plan, but the corpus of the average subscriber is likely to fall woefully short of his requirement. One needs to make additional investments to build a corpus big enough to sustain one’s expenses for 20-odd years after retiring.

To be fair, the Provident Fund’s design makes it the most effective way to save for retirement. You start contributing from the very month you start earning, and since it is a compulsory saving, you can’t avoid it. Besides, your contribution is linked to your income and rises with every increment in your salary. If a person takes up a job at the age of 25, even a modest contribution of Rs 5,000 a month and a matching contribution by his employer can build up a massive corpus of Rs 6.89 crore over 35 years. This calculation assumes that his income (and, therefore, the contribution) will rise by 8% every year and the PF will give 8.5% returns.

While the figure of Rs 6.89 crore may appear huge, it may not be enough. If you need Rs 50,000 a month for living expenses today, a 7% inflation would push up the requirement to roughly Rs 5.34 lakh a month in 35 years. When you are 60, you would need a corpus of Rs 10.52 crore to sustain inflation-adjusted withdrawals for the next 20 years (see table). Assuming a post-tax return of 8.5% and 7% inflation, the Rs 6.89 crore from the PF would be completely wiped out in a little over 12 years. This could mean having no money in your retirement account at the age of 72.

There’s another problem. To make your PF work for you, you must remain invested for the long term. However, a lot of people withdraw their PF when they change jobs, thus losing out on the power of compounding. “In India, the PF is often used for other purposes, particularly when people change jobs. They end up withdrawing this accumulated corpus to buy expensive gadgets or go on a holiday, forgetting that the purpose was retirement planning,” says Arvind Usretay, India Retirement Business Leader, Mercer. A recent global survey by Mercer has ranked India’s retirement system the lowest among the 25 countries surveyed. “What continues to hold India back is the lack of retirement coverage for the informal sector and less than adequate retirement income expected to be generated from contributions made to the Employees’ Provident Fund (EPF) and gratuity benefits,” notes the Mercer study.

Another global study by Towers Watson points out that a significant majority of employees sees their employer retirement plans as the most important source of income in retirement. “Employers must educate their employees on the need for retirement planning and provide them the tools to help them save adequately,” says Anuradha Sriram, director, benefits, Towers Watson, India.

To ensure a comfortable life in retirement, one needs to make additional investments to build a corpus big enough to sustain one’s expenses for nearly 20 years in retirement. Here are a few options you can consider.

Mutual funds

Mutual funds are, perhaps, the best way to supplement your retirement savings. Among these, equity mutual funds have the potential to give very high returns, but also carry high risk. They are best suited to younger investors who can withstand short-term volatility to earn long-term gains. “Equity funds should be the instrument of choice for young investors who have 25-30 years to build a retirement kitty,” says Suresh Sadagopan, founder of Ladder7 Financial Advisories. An additional advantage of investing in equity funds is that the gains are tax-free.

If you are averse to taking risks, consider a balanced fund, where the equity exposure is lower. Ultra cautious investors can go for MIPs of mutual funds that invest only 15-20% of their corpus in stocks and put the rest in bonds. However, the returns of MIPs will not be able to match those of equity and balanced funds.

Ulips

Ulips have earned a bad name because of the rampant misselling in the past. However, this much reviled product can be a good option for retirement planning. In recent months, insurance companies have come out with online plans that levy very low charges. The Click2Protect plan from HDFC Life charges an annual fund management fee of 1.35%, which is less than the direct mutual fund charges. The Bajaj Allianz Future Gain plan does not levy premium allocation charges if the annual investment is Rs 2 lakh and above. The Edelweiss Tokio Wealth Accumulation Plan doesn’t have policy administration charges. Some Ulips, such as Aviva i-Growth and ICICI Prudential Elite Life II, don’t have lower charges but compensate long-term investors with ‘loyalty additions’. The best part in a Ulip is that one can shift money from debt to equity, and vice versa, without incurring any tax liability. The corpus is also taxfree on maturity.

Source : http://goo.gl/y5gCLT

NTH :: Online transfer of PF accounts likely to start from August 15

Online transfer of PF accounts is likely to benefit over 13 lakh applicants every year.

PTI | Jul 28, 2013, 10.45AM IST | Times of India

NEW DELHI: Retirement fund body EPFO is likely to start online transfer of PF accounts on changing jobs by this Independence Day on August 15, a move that would benefit over 13 lakh such applicants every year.

The Employees’ Provident Fund Organisation (EPFO) has started registering digital signatures of employers from Thursday which is a prerequisite for providing the facility and is expecting an overwhelming response from employers.

According to sources, EPFO is hopeful that a sizable number of firms would get their digital signatures registered in the next two weeks and the body can then launch the service.

The source said that the body is planning the launch of service to coincide with Independence Day, which would be followed by an awareness campaign to make it popular.

He said that EPFO is expecting establishments which constitute 80 per cent of the transfer claims from sectors like IT, to register their digital signature in next 2 weeks.

According an an official, it would be very easy for these firms as they are already maintaining digital signatures for compliance like for ministry of corporate affairs. The body had managed about 6.9 lakh establishments in 2011-12.

Once the service is launched, subscribers would be able to apply online for transfer claims through their employers. It has set up a central clearance house for the purpose.

During 2012-13, 107.62 lakh claims were settled, of which 88 per cent were processed within 30 days, as prescribed by the body’s citizen charter.

EPFO expects 1.2 crore claims in 2013-14, including around 13 lakh PF transfer claims. It plans online settlements of about 10 lakh transfer claims of tech-savy applicants from industries such as IT, this fiscal.

The body has planned to reduce the time for transfer of PF account to three days through this online service.

Source : http://goo.gl/do2sK1

NTH :: Online PF transfer claim settlement to be a reality by August end

PTI | Jul 7, 2013, 12.23PM IST | Times of India

NEW DELHI: Retirement fund body, EPFO, will be able to operationalize the facility of online settlement of provident fund (PF) transfer claims by August end, a move which would benefit over 13 lakh such applicants every year.

“Employees’ Provident Fund Organisation (EPFO) will make functional, the online settlement of transfer claims on changing jobs, by August end,” a source said.

EPFO is expecting 1.2 crore claims in 2013-14, including around 13 lakh PF transfer claims. The body has planned to settle online, around 10 lakh transfer claims of tech-savvy applicants from industries like IT and other sectors this fiscal.

The reason for their optimism is that the employers in sectors like IT; generally have a registered digital signature, which is prerequisite for online claim settlement, the source said.

Taking the first step towards launch of online PF transfer claim facilities, EPFO had unveiled the revised transfer claim form for the purpose on Thursday.

The revised ‘Transfer Claim Form’ can be presented after verification, either through the present employer or the previous employer. Earlier, the form could be submitted after verification, only through the present employer.

EPFO has set up a central clearance house to enable subscribers to apply online for PF withdrawal and transfer claim settlements.

The body also has plans to launch a facility for online settlement of withdrawal of PF subsequently. It has already digitalized the records of 122 offices and processed all its present claims on computer.

At present, the body has geared up for speedy settlement of all types of claims. As such 40 of its offices are doing it in less than 5 days and 30-40 offices in 10 days.

EPFO has already computerized the processing of claims. It envisages settlement of all types of claims within a three-day period. At present, EPFO is expected to settle all claims within 30 days as per its citizens’ charter.

Source: http://goo.gl/ICtav

NTH :: EPFO to keep interest rate on PF unchanged at 8.5% in 2013-14

PTI | Jun 23, 2013, 10.38AM IST| Time of India|

NEW DELHI: Retirement fund body EPFO is likely to pay an interest rate of 8.5 per cent on provident fund deposits for 2013-14 to its over five crore subscribers, the same as provided in 2012-13.

“The rate of interest on PF deposits is unlikely to be changed for the current fiscal at 8.5 per cent,” a source privy to the development said.

Employees’ Provident Fund Organisation (EPFO) paid 8.5 per cent interest rate to its subscribers in 2012-13 which was higher than 8.25 provided in the 2011-12 fiscal.

The source further revealed that the EPFO office has already worked out the income projections and the feasible rate of return to be provided on PF deposit in the current fiscal.

As per the practice, the EPFO would have to place the proposal before its advisory body Finance and Investment Committee (FIC) after which it is considered by the apex decision making body Central Board of Trustees (CBT)headed by the Labour Minister for taking final call on the matter.

Once approved, the proposal is put before the finance ministry for its concurrence.

EPFO has recently reconstituted the CBT and thus the FIC would be constituted again in the next meet of trustees.

According to the source, the CBT meeting is likely to be convened next month as the new Central Provident Fund Commissioner, K K Jalan, who is executive head of EPFO has taken charge.

The source said that one of reason for proposing to keep the rate of interest unchanged for this fiscal is slight drop in government securities yield.

As per the 2008-Investment Pattern adopted by the EPFO, the body can invest up to 55 per cent of its huge corpus of over Rs 5 lakh crore in the state and central securities.

Source : http://goo.gl/ZLpqV

ATM :: EPF/PPF scores over NPS

Neha Pandey Deoras & Shivani Shinde | Bangalore/ Mumbai April 7, 2013 Last Updated at 22:30 IST| Business Standard|

For retirement solutions, financial advisors prefer sticking to a combination of EPF/PPF and equity mutual funds

Bangalore-based Dirk Lewis, 30, who works for a leading information technology services company, plans to subscribe to the National Pension System (NPS) from the next financial year (2014-15). His company offers the NPS option to its employees, over and above the mandatory Employees’ Provident Fund (EPF) provision.

“NPS would help me save more on the tax front. Also, knowing myself, I would save only when I am forced to. This way (through NPS), I would be able to build a neat corpus for my retired life. I have some expenses this year, which wouldn’t allow me to contribute towards NPS,” says Lewis.

A host of companies, including Infosys, Wipro, Reliance Industries, Muthoot Finance, Colgate-Palmolive, Capgemini and Pantaloons, offer the NPS option.

Samir Gadgil, general manager and global head (compensation and benefits), Wipro, says the company has been seeing good traction from employees interested in NPS, over and above EPF. “On an average, annual contribution stood at Rs 4-6 crore. And, the number of employees subscribing to the scheme is growing on an annual basis,” he says.

Wipro recommends NPS for product diversification, as well as a substitute for voluntary contribution towards EPF, Gadgil says.

Some companies say primarily, those in the 30-35 age bracket are subscribing to NPS, as they are aware the product’s equity component could deliver good returns through 30 years.

George Alexander Muthoot, managing director of Muthoot Finance, feels NPS would help his employees build a decent retirement fund.

A company can either offer investment options at the subscriber level, allowing employees to choose the pension fund manager and the asset allocation (active choice), or at the company level, in which case the company decides the fund manager and the asset allocation (auto choice). Under the latter, the company may opt for the portfolio mandated for central government employees and choose from the three government fund managers – LIC Pension Fund, SBI Pension Fund and UTI Retirement Solution – or from schemes and fund managers for the voluntary sector.

All one has to do is subscribe to NPS and ask his/her employer to deduct a fixed amount every month or year. Many companies also contribute towards their employees’ NPS and get tax benefits under Section 80CCE by terming this business expenditure in their profit-and-loss accounts. Even the employer’s contribution of up to 10 per cent of basic and dearness allowance is eligible for deduction, though such employers later deduct their contribution from the employee’s salary. Most companies ask for an annual contribution of at least Rs 6,000 (once a year), or at least Rs 500 a month. Many companies have spread awareness on NPS among employees through web seminars, group discussions and helpdesks at their campuses.

Financial planners, however, aren’t too enthused by NPS (compared to EPF), though comparing the two isn’t fair—while EPF is purely a debt product, NPS also invests in equity. Certified financial planner Arnav Pandya feels EPF is meant for those who do not understand investment very well—they simply put away money in EPF and earn handsome returns. NPS, however, is meant for those who have a fair knowledge on investment and can choose funds. “NPS is a product that should figure in the list you consider for investing for your retirement, whether you put money into it or not,” he says.

For Mumbai-based certified financial planner Gaurav Mashruwala, in their current forms, EPF scores over NPS, a view shared by Sumeet Vaid of Freedom Financial Planners.

“Simply put, EPF is slightly market-driven to the extent of investing in government securities, while NPS is about 50 per cent market-driven, due to the equity component. As a result, returns are safe in EPF, not in NPS. There is a small cost attached to investing in NPS, but there is no cost in investing in EPF,” says Mashruwala.

Also, NPS has withdrawal limits; EPF does not—it offers premature withdrawal for specific purposes (house construction, marriage and illness), without foreclosure. Any premature withdrawal leads to account closure in the case of NPS. Up to 20 per cent of the funds can be withdrawn from NPS before one turns 60; the rest has to be used to buy annuity. Also, you can easily stop contributing towards EPF in desperate times; you can’t do so with NPS.

“One NPS fund manager I met recently told me they don’t make money on NPS asset management; they hardly rejig the portfolio on the back of market conditions,” says an industry expert. If fund managers aren’t paid adequately, returns may soon start declining. The expert, therefore, feels the government should look at developing the product to make it more investor-friendly.

Also, NPS returns aren’t very attractive. The Employees’ Provident Fund Organisation (EPFO) gives 8.5 per cent returns to subscribers. Till August 2012, returns offered by NPS stood at 6-11 per cent (an average of 8.5 per cent). Though NPS should give better returns (compared to EPF) due to the equity component, this hasn’t been the case. Therefore, it hasn’t appealed to investors or financial advisors. Vaid says many company trusts that manage EPF money on their own have delivered higher returns – 9-9.5 per cent. Therefore, it might not be sensible to consider NPS.

Like Lewis, most look at NPS from a tax-saving perspective. Even then, the product doesn’t seem lucrative. An employee’s contribution of only up to 10 per cent of the basic and dearness allowance is eligible for deduction under Section 80CCD (this amount is within the Rs 1-lakh limit, under Section 80C). Most taxpayers exhaust a substantial part of the Section 80C limit through EPF contribution, which can be invested up to Rs 1 lakh, completely tax-free. Hence, contributing to NPS is hardly of any use, as long as you are an indisciplined investor and need to be forced into investing. A withdrawal from NPS is taxable at the slab rate and so is the annuity to be earned after retirement.

Therefore, Mashruwala advises sticking to EPF or Public Provident Fund (PPF), which offer annual returns of 8.7 per cent, and taking the equity-oriented balanced fund route to add equity to the retirement portfolio. According to mutual fund rating agency Value Research, equity-oriented balanced funds returned about seven per cent in the past year.

Financial experts feel for self-employed individuals, too, PPF scores over NPS, as investments of up to Rs 1 lakh in PPF are completely tax-exempt.

While Gadgil says an employee can continue using his NPS account even after quitting an organisation, Vaid is doubtful about whether an employee would be disciplined enough to continue investing on his own, as the organisation he joins next may not offer NPS. He says, “Servicing is better when a product is offered by an organisation. This might not be true for independent NPS accountholders. NPS’ product structure might not be easy to understand for most.” He recommends a combination of EPF/PPF, debt funds and index funds. In the past year, the BSE Sensex returned about nine per cent, while the National Stock Exchange’s Nifty gave eight per cent returns. From a tax point of view, too, equity is very efficient—if held for more than a year, returns from equity investment are tax-free in the hands of investors. Across categories, debt funds have returned 9-11 per cent higher than NPS. Also, if held for more than a year, debt funds get indexation benefits.

Source: http://goo.gl/C0nAM

NTH :: Your provident fund savings all set to fetch higher returns from 2013-14

30 MAR, 2013, 06.43AM IST, VIKAS DHOOT, ET BUREAU

NEW DELHI: You can expect your provident fund savings to earn better returns from 2013-14, though small savings instruments like national savings certificates will deliver lower returns from April 1.

The Employees’ Provident Fund Organisation (EPFO) will adopt a new investment pattern from the coming financial year, junking its archaic investment norms that have remained unchanged since 2003 and have been blamed for the falling returns on EPF savings in the last two years.

In 2011-12, over 6 crore EPF members were paid 8.25% on their retirement savings. For 2012-13, a return of 8.5% has been declared though the finance ministry is yet to ratify the payout.

By contrast, PPF savings earned 8.8% this year and will earn 8.7% in 2013-14. The labour ministry has decided to modify EPFO’s investment norms to boost returns on its Rs 5,00,000 crore corpus and stave off persistent criticism from stakeholders and the finance ministry over EPF returns being lower than high inflation rates and the comparable returns of 10%-14% offered by the New Pension Scheme run by the Pension Fund Regulatory and Development Authority.

The EPFO was hurtling into an investment crisis and its income was expected to fall to 8% by 2017-18, if it had maintained status quo. Though its corpus has been increasing, EPFO’s investment avenues haven’t grown, even as it faces increased competition from foreign institutional investors and domestic financial institutions in the bond market.

Under the new norms, EPFO can invest its corpus in bonds issued by eight new blue chip private sector firms such as Reliance Industries and Larsen and Toubro. Eight more firms, which include Tata Consultancy Services, Infosys Technologies, Wipro and Ambuja Cements, could also qualify for fresh bond investments.

This will significantly expand the universe of private firms that EPFO can invest in, which currently only includes seven firms — HDFC Bank, LIC Housing Finance, ICICI Bank, Infrastructure Leasing and Finance Services Ltd, Axis Bank, HDFC and IDFC.

To improve its returns from PSUs bonds, the EPFO has changed the tenure limits for such securities so that it can lock into better returns for a longer period. The maximum tenure for AAA-rated PSUs has been raised from 15 years to 25 Years, and from 8 years to 15 Years for AA-rated PSUs. AAA ratings denote the highest level of safety for bond investments.

Rating agency Crisil reckons that changes in norms for private sector firms’ bonds would boost EPF earnings by over Rs 3,000 crore in next 10 years. Similarly, allowing longer-term investments in public sector bonds would boost its income by over Rs 7,700 crore over the next decade.

Income from plain vanilla government bonds would also go up, as the PF office will now be able to deploy upto 55% of its fresh inflows into state government bonds that deliver higher returns than central government securities, where 70% of its annual corpus is currently parked. Nearly 90% of EPFO’s private bond investments were concentrated in banks, as on December 2012.

Even among public sector bonds, banks accounted for 53% of EPFO investments while other firms accounted for just 35%. With new bond issuances from public sector firms being limited, it has been forced to park money in banks’ term deposits.

The RBI’s implementation of Basel III capital regulations also creates the problem that new bond issues from banks will have an equity convertibility clause. The EPFO has steadfastly opposed equity investments, though finance ministry has opened the stock market window for PFs since 2005.

Source : http://goo.gl/6oZfa