Tagged: Life Insurance

ATM :: 5 rules to keep in mind after your loan is sanctioned

Jan 08, 2018 04:27 PM IST | MoneyControl.com

The following article is an initiative of BankBazaar.com and is intended to create awareness among the readers

Applying for a loan can be nerve-racking, with a number of formalities expected to be completed. Most of us think that our job is done once the loan is sanctioned, but this is not the case. The real story, in most cases, begins once the loan is disbursed, for this is when we encounter problems with the repayment.

So if you are someone who has recently applied for a loan, (be it a home loan, a personal loan, car loan, medical loan, or any other loan), you should consider these 5 rules to ensure that you get the most out of the money.

1. Never miss your EMI – Taking a loan is a huge financial responsibility. Banks sanction loans for a specific time period (the tenure), charging interest rates on the amount loaned. The borrowed money is expected to be repaid within the given time, with the entire sum and the interest component split into EMIs. Paying the EMI on a monthly basis is not merely a requisite with regards to the legalities, it also helps in building a good credit score.

A missed payment is reflected on the credit report, which could make it difficult to get a loan sanctioned in the future. Missing successive payments could result in lenders blacklisting one, which could ultimately lead to the borrower being labelled a defaulter.

A borrower should ensure that he/she has sufficient funds to repay the loan on time. In certain cases, banks can charge a fine for late payment, which can be a considerable sum in case of high loan amounts (for example a home loan).

2. Never use your savings to repay the loan – Most of us invest in certain saving schemes like PPF, fixed deposits, mutual funds, etc. These funds are ideally designed to help us during emergencies. Utilising them to repay a loan is an absolute NO-NO. Similarly, digging into your retirement fund to meet your EMI obligations should be avoided at all costs, for this can have a huge impact on your future, where you might find it hard to have a regular source of income.

3. Take an insurance cover for the loan amount – Certain loans can be of extremely high values. This is especially true in the case of home loans, where the loan amount is typically in excess of Rs.10 lakh. This can be a significant sum for most people, with it taking years to repay it. Given the unpredictability surrounding life, one should always take an insurance policy which covers the loan liability in case of the borrower’s death. A number of life insurance policies come with this option, wherein the outstanding loan amount (in case the insured passes away) is paid by the insurer. This can limit the financial strain on the family members of the borrower. One could also consider taking an insurance policy in case of other loans, if the repayment amount is significant.

4. Avoid taking additional loans while a current loan is active – Banks and NBFCs often come up with attractive offers to promote borrowing. A number of us can often give in to the lure of extra money, applying for additional loans even when we don’t need them. This should be avoided at all costs, for any additional loan increases the financial burden when it comes to repayment. Also, applying for multiple unsecured loans like personal loan or travel loan while already paying EMIs can come across as sketchy, in addition to having an impact on the credit score. Banks would be wary of offering loans in the future in such instances. If one truly is in the need of additional financial resources, he/she should first close an existing loan before taking a new one.

5. Make prepayments when you have extra money – There are a number of times when we come across additional income. Returns from investments, a bonus from the office, an increase in your salary, etc. can be used to prepay a loan. This can help one save money on the interest payable, in addition to offering peace of mind, knowing that one’s liability is reduced.

A loan, when used effectively can help us out during financial emergencies, but being frivolous once it is sanctioned could lead us towards additional turmoil.

Source: https://goo.gl/enBVeJ

ATM :: How to become rich fast at a young age in India: 5 amazing investment strategies to follow before you turn 30

Everyone wants to be financially secure and well off by the age of 35-40. However, when we are in our 20’s, we tend to live life in the moment and forget saving for the future.

By: Sanjeev Sinha | Updated: November 27, 2017 2:25 PM | Financial Express

All of us have various financial goals in life. Everyone wants to be financially secure and well off by the age of 35-40. However, when we are in our 20’s, we tend to live life in the moment and forget saving for the future. This is not the right approach towards creating wealth. Therefore, to ensure that you are financially secure and on the right track with your money, here are 5 important investments that you must make before you hit your 30-year milestone:

1. Investment towards tax saving

Considering that you are working and earning, it is important for you to assess your tax liability and take advantage of tax deductions available under Section 80C of the Income Tax Act. “By proper tax planning, you can not only reduce your tax liability but also save some more to invest towards your other goals. One of the best tax-saving instruments is Equity-Linked Savings Schemes (ELSS). It is a type of open-ended equity mutual fund wherein an investor can avail a deduction u/s 80C up to Rs 1.50 lakh for a financial year,” says Amar Pandit, CFA and Founder & Chief Happiness Officer at HapynessFactory.in.

2. Investment towards emergency corpus

There are various events like accidents, illnesses and other unforeseen events that we may encounter in our lives. These events should never occur, but if they do, one needs to be adequately prepared for the same. In critical cases, such events may hamper one’s ability to work and may even lead to a loss in earnings for a few months or years. Hence, “it is advisable to build a contingency corpus, which is equivalent to at least 5-6 months of living expenses. Further, your emergency fund should be safe and easily accessible (liquid in nature) at short notice, in case of an emergency. Hence, savings bank accounts and liquid mutual funds are two options for setting aside the emergency corpus. However, considering that liquid and ultra-short term mutual funds are more tax efficient in nature, it is advisable to park a major portion of your corpus in the same,” says Pandit.

3. Investment towards long-term goals

It is very important to save and invest towards your long-term goals such as marriage, buying a house, starting your own venture, retirement, and so on. You must start with determining how much each goal will need and the savings required to achieve the goal. Once the corpus is fixed, you can invest towards the goal regularly. As an investment strategy, start fixed monthly investments – SIPs (Systematic Investment Plan) in mutual funds. Always remember, the earlier you start investing towards your goals, the longer time your investments will have to grow and the more you will benefit from the power of compounding. Equity mutual funds which are growth oriented are a preferable investment option for long-term goals.

4. Investment towards short-term goals

There are many short-term goals that are recurring in nature, such annual vacation, buying a car or any asset in the near term and so on. For such goals, you are advised to park your funds in liquid or arbitrage mutual funds rather than a savings account. “Mutual funds are more tax efficient than savings accounts and also there are different funds for different time horizons. For example, for goals to be achieved within a year, you can opt for liquid or ultra-short term funds whereas for goals to be achieved post one year, you can opt for arbitrage funds,” advises Pandit.

5. Investment towards health and life cover

Life and health insurance typically are not supposed to be considered as investments. However, both are very important and must be considered as one of the priority money move to be made before turning 30. If you are earning and have a family dependent on you, you must assess and buy the right life insurance term cover for yourself. Further, with costs of health care and medical on the rise, any untoward illness without sufficient cover will have you dip into capital which is unnecessary. Hence, there cannot be any compromise on health insurance. Thankfully, there are various health covers available in the market today. You should opt for the right cover for yourself, depending on your needs and post considering all the options.

Source: https://goo.gl/Abf7TR

ATM :: Why it makes more sense to switch your home loan after this interest rate cut

By Sunil Dhawan | ECONOMICTIMES.COM| Updated: Jan 04, 2017, 11.23 AM IST

The start of the new year may have something to cheer for the home loan borrowers. Several banks have significantly reduced the interest rates charged on these loans.

The State Bank of India (SBI) has lowered its home loan rate from 9.10 per cent to 8.60 per cent and ICICI Bank from 9.10 percent to 8.65 percent, HDFC at 8.7 per cent, with other banks set to follow suit. Effectively, home loan rate has come down by an average of about 0.4-0.5 per cent after these announcements.

Noticeably, SBI’s one-year MCLR is at 8 per cent which makes the spread on its home loan 0.6 per cent. So, even though the MCLR of banks have fallen, the actual home loans are not at MCLR. Still, the writing on the wall is clear – there is more room to cut home loan rates by the banks.

Borrowers on base rate should switch now

If not all then at least the old borrowers who have been servicing their EMI’s based on the erstwhile base rate system of lending, stand to benefit. Even though bank’s base rate hasn’t come down as much, they now have a stronger reason to switch to the current MCLR-based lending. With the recent interest rate cuts on loans by banks the differential between base rate at which old borrowers are servicing their loan and the current MCLR is widening.

For those who had taken loans after July 1, 2010, but before April 1, 2016, the loans are linked to the bank’s base rate. And for most of these borrowers, the home loan interest rate is around 10 per cent. After the recent rate cuts announced by banks, the average MCLR has fallen to about 8.75 percent or even lower. This differential of 1-1.25 percent in base rate and MCLR will help old borrowers to switch to MCLR and save on total interest outgo.

Why to switch now

The primary reason to switch from base rate to MCLR has to be the sluggishness seen in banks’ passing on the benefits of RBI rate cuts to borrowers. RBI’s repo rate cuts were not reflecting in the bank’s base rate but are a part of the factors that goes into calculating the bank’s MCLR so, the moment repo rate changed, MCLR was impacted.

Further, the MCLR takes into account the marginal cost of funds which includes the rate at which the bank raises deposits and other cost of borrowings. With banks flush with funds post demonetisation, the bank’s CASA deposits (current account-savings account) have swelled and have given the banks the leeway to go for such major rate cuts.

The base rate, on the other hand, has seen only marginal reduction since last 24 months. Post demonetisation, banks are expected to wait and see the impact once the restrictions on cash withdrawals are removed. If the funds don’t move out from the banking system in significant amounts, further rate cut is expected.

MCLR based borrowers

For the new home loan borrowers who have taken loan after April 1, 2016, there’s not much immediate benefit from the recent rate cuts. For most MCLR-linked home loan contracts, the banks reset the interest rate after 12 months for their home loan borrowers. So, if someone has taken home loan from a bank say in May, 2016, the next re-set date will be in May, 2017. Any revisions by RBI or banks will not impact their EMIs or the loan till the reset date

What’s MCLR mode of lending

A new method of bank lending called marginal cost of funds based lending rate (MCLR) was put in place for all loans, including home loans, given after April 1, 2016. Under the MCLR mode, the banks have to review and declare overnight, one month, three months, six months, one year, two years, three years rates each month.

Watchouts

In a falling interest rate scenario, quarterly or half-yearly could be a better option, provided the bank agrees. But when the interest rate cycle turns, the borrower will be at a disadvantage. After moving to the MCLR system, there is always the risk of any upward movement of interest rates before you reach the reset period. If the RBI raises repo rates, MCLR too, will move up.

Options for base rate borrowers

When the interest rate on your loan goes down banks, on their own, typically reduce the tenure automatically (instead of reducing EMI amount) and thereby, transfer the benefit of lower rate to the customers.

The base rate borrowers now have two options – switch to MCLR based lending with the same bank or else transfer i.e. get the loan refinanced from another bank on MCLR mode. One may also continue the loan on base rate, especially if the loan term is nearing the end.

The RBI has made it clear that banks should allow base rate borrowers to switch to MCLR. The existing loans can run till maturity or borrowers can switch to MCLR on mutually agreed terms.

Switching from base rate to MCLR within the same bank

It makes sense to switch if the difference between what you are paying and what the bank is offering now as MCLR is significant. And also in cases where the time for the home loan to finish is not near.

Switching loan from base rate to MCLR with another bank (refinancing)

If your bank is offering a high home loan interest rate (MCLR plus spread) then look for refinancing. Get the loan refinanced from a bank offering a lower interest rate. You may have to incur processing fees. However, banks are not allowed to charge foreclosure or full repayment charges. Other charges may include lawyer’s fees, mortgage charges, etc. Remember, the bank may ask you to buy a home loan insurance cover plan, which is not mandatory. Get the loan insured through a pure term insurance instead, in addition to any insurance that you already have.

Conclusion

Switching to MCLR in itself should help you save a substantial amount. In addition to switching the loan from base rate-linked to MCLR and thereby saving interest, prepare a systematic partial prepayment plan to further reduce the interest burden. It’s after all better to up your home-equity rather than making it a highly leveraged buy-out.

Source: https://goo.gl/6R5mh0

ATM :: Three must have add-ons with your term life insurance plan

Santosh Agarwal – PolicyBazaar | Dec 08, 2016,12.35 IST | Source: Moneycontrol.com

Did your insurance agent discourage you from buying a term life insurance plan just because you will get no benefit unless you die? If you trust him blindly, you will only help him earn a better commission, by going over budget for a plan that may not cover you sufficiently. The agent was right when he said that a term plan offers the sum assured only if the policyholder dies during the policy tenure. But, what he may not have pointed out to you is:

1. Insurance plans that offer benefits on maturity are more expensive than term plans.

2. By opting for a TROP (Term with Return Of Premium) plan, you can get back all the premiums you paid, on the maturity of the policy.

3. By purchasing add-ons or riders, you can enhance the protection offered by your term plan.

Riders are purchased additionally with a basic life insurance plan for getting additional benefits. Term plans are the simplest and the most cost-effective life insurance plans. But a term plan alone may not be sufficient in certain cases. For instance, if you get severely injured in an accident, or get diagnosed with a life-threatening disease, a term plan will not help you bear the major expenses of your prolonged treatment. In such cases, the add-ons come in handy. When you buy a life insurance plan, the available riders may vary with the insurance provider and the policy.

Here, we will discuss the three most important add-ons that you must have with your basic term insurance plan.

1) Accidental disability rider

Accidents are unfortunate and unpredictable. An accident may leave you disabled for life. If you have dependents in your family, they will be in a crisis to manage their living and paying for your treatment simultaneously while you are not earning. Such unfortunate instances are covered by accidental disability rider. If you suffer from disability due to an accident, the rider will offer the sum assured by which your family will be able to maintain a livelihood and bear the cost of your treatments as well.

Cost estimates: If you are a 30-year-old, opting for a base cover of Rs. 1 crore over a 35-year time period, an accidental disability rider will cost you around Rs. 300 to Rs. 500 annually for a cover of Rs 10-30 lakh.

2) Critical illness rider

Today’s fast-pacing life is taking a toll on our health. Consequently, several life-threatening diseases are on the rise. The diseases like cancer, stroke, organ failure call for prolonged treatments that can be quite expensive. Critical illness riders ease off the burden of expensive medical treatments by offering a lump sum assured to the policyholder in case he is diagnosed with any of the medical conditions pre-specified under the plan. However, pre-existing medical conditions will not be covered by this rider.

Cost estimates: If you are a 30-year-old, opting for a base cover of Rs. 1 crore over a 35-year time period, a critical illness rider will cost you around Rs. 5,000 to Rs 10,000 annually for a cover of Rs 25-50 lakh.

3) Waiver of premium rider

When you buy a term plan, you get into a contract of paying on a regular basis for a certain period of time (unless it is a single pay plan). But what will happen if you are unable to work due to some unfortunate accident in your life? How are you going to pay for the rest of the policy term if you are left disabled by the accident and there is no other earning member in your family? The waiver of premium rider comes with the solution. In case you are unable to pay your premiums due to some disability or diseases leading to the loss of your job, all your future premiums will be waived off. You will no longer have to pay the premiums but your basic term plan will still continue till the date of maturity. Typically, this rider comes included as part of a term cover, however if that’s not the case, it’s recommended to opt for this must have rider.

Cost estimates: If you are a 30-year-old, opting for a base cover of Rs. 1 crore over a 35-year time period, the waiver of premium rider will cost you around Rs. 400 to Rs 600 annually.

The cost of a rider may vary from one insurance provider to another. Both expensive and low-cost riders are available and they also depend on the base sum assured. However, riders are, undoubtedly, the most important tools to strengthen your basic term insurance cover. Riders come in handy in certain eventualities in life. So, if you want comprehensive life coverage for you and your family, a term plan with the three riders mentioned above are worth considering.

Source: https://goo.gl/ew4OWS

ATM :: Young earner? Five financial mistakes you may regret later

By Sanjiv Singhal | Jun 20, 2016, 07.00 AM IST | Economic Times

Interact with a lot of young earners on a daily basis. These are men and women in the first 5-6 years of their working lives, with dreams and hopes that require money to achieve. Some of them are already saving, while others are not, but all are full of questions and want to know how to do it better. It doesn’t matter what job they have and how much they earn; there are mistakes that run through all their stories. Here are some of the most common ones:

“I bought a life insurance policy to save tax.”

The good thing about this confession is that the person understands he made a mistake. For most, it starts at the end of the year when they needed to submit their investment proof to the HR. They scramble around to figure out how and blindly buy an insurance policy (after all, insurance is a good thing to have, no?). Almost every other tax-saving option is better than life insurance. Tax-saving (ELSS) funds are the best option for young earners.

“I wasn’t sure where to invest, so I didn’t.”

When you don’t set aside money regularly, it sits in your bank account and often gets spent. This hurts in two ways. One, it doesn’t create wealth for you, which investing early does. Second, it forms unsustainable spending habits. Start by setting aside 5-10% of your salary every month in a debt fund or in a recurring deposit if you don’t know enough about mutual funds.

“I bought stocks to double my money because my friend did.”

This is a mistake often made due to lack of understanding about how stock investment works and a false sense of knowledge. Greed and stories of exceptional returns also spur one on. The best way to resist this is to check with friends and colleagues about how many actually earned such fantastic returns and how many lost money. Stock investing requires deep knowledge and time. As a young professional, you are better off committing this time to your job.

“I change jobs every year to increase my salary.”

This is not an investing mistake, but one of not investing in yourself. Sticking with a job gives you the opportunity to develop your skills in a specific area. It also gives you the time to learn softer skills – of working with people and managing them. This leads to better career prospects and more wealth.

“I forgot about my education loan.”

A lot of young earners are starting their financial lives with an education loan taken for an MBA or MTech. As they mostly work away from home, they may not get the communication from the bank, or choose to ignore it. The interest mounts up and they are left with a bigger repayment amount. Focus on education loan repayment in a disciplined manner. When you are done with the with the repayment, direct this amount to long-term investments. Avoiding these common mistakes is easy once you know about them. Spending time learning about the principles of money and investing is a good investment to begin with.

(The author is Founder & Head, Product Strategy at Scripbox)

Source: http://goo.gl/O7HPqf

ATM :: Risk cover for your home loan

BALAJI RAO | The Hindu

A term assurance provides financial stability in case of unforeseen events and ensures that EMIs are paid.

Rangan is 35 years old, married, has twins aged three years. His wife, Ragini, is a home-maker. She teaches music to a few young aspirants and earns a small amount of money every month that takes care of her personal expenses. But Rangan is the main earning member of the family. He works for an IT company, earns well, has a home loan which still has another 17 years of repayment (Rs.50 lakh more to be paid including principal and interest), has a car loan to be paid for another three years, and has to take care of his children’s education over the next 20 years.

Rangan is bit worried about unforeseen events such as accidents, illness, loss of job and premature death. He has a beautiful house on which he had spent quite a bit of his savings and also taken a hefty loan. He also wants to secure his family financially.

What could Rangan do that ensures his family is not into any financial mess if some unforeseen event occurs? The one solution for all these is insuring the risks adequately. There is a general confusion due to lack of financial education and awareness that insurance plans are purchased to meet life’s events, whereas the purpose of insurance is to protect against unforeseen events leading to financial risk. Financial goals and risks should not be mixed; it would be a bad marriage.

Segregate goals, risks

Rangan should segregate his financial goals and financial risks. His goals are to meet his children’s education expenses, their marriage, expenses upon retirement some 25 years from today, vacations, upgrading of house, upgrading of car, pre-closing his home loan, etc. His financial risks are losing his job, health scare leading to hospitalisation, and premature death that could risk his house (not being able to pay the EMIs).

While Rangan is investing in financial instruments such as debt and equity to meet his financial goals he has inadequate cover to meet his financial risks. He should split his risks in such a way that he manages them diligently with low investments. Let’s see how Rangan can do it.

Three elements

He should buy three separate pure risk covers by way of term assurances. For the home loan outstanding, he should buy a term assurance which could cost him Rs.5,000 per annum (approx.) for a period of 17 years. In case of premature death the insurance company would pay his legal successor the sum assured which could be utilised to repay the home loan and retain the house.

For the children’s education he should buy another term assurance plan for Rs.1 crore for a period of 20 years which could cost him Rs.6,500 per annum (approx.). In case of his untimely death, the sum assured would be paid by the insurance company to cover the children’s education-related expenses.

For his life risk until retirement, he can choose another Rs.50 lakh to Rs.1 crore as sum assured under term assurance for 25 years which could cost him Rs.5,500 to Rs.6,500 per annum (approx.) that would take care of all other financial risks.

In case no untoward incident (such as his untimely death) happens, at the end of 17 years during the repayment of his home loan the premium payment will stop. Similarly, 20 years from today the premium payment for education too stops; only the overall risk-related premium payment would continue till he is 60 years old.

This is by far the best method of addressing financial risks. People make the mistake of buying traditional plans such as endowment, money back and whole-life policies which are highly expensive and impractical to cover the entire financial risks across different stages and requirements of life.

Health insurance

Rangan should also buy health insurance. Though he argues that his company has medically covered him and he will not need another insurance cover, this has no rationale because if he quits his job, his company-covered insurance would become invalid. Even if he works till his retirement, post-retirement his insurance cover would cease to exist. Hence, he should buy a health cover worth at least Rs.15 lakh which could cost him approx. Rs.15,000 per annum.

Source : http://goo.gl/xXVEqh

ATM :: Financial planning in new year: Start it now

Don’t tinker with your long-term investment plan. But it is always better to make some critical changes, based on new tax laws and instruments

Sanjay Kumar Singh | April 3, 2016 Last Updated at 22:10 IST | Business Standard

The start of a new financial year is a good time to review your financial plan and take stock of where you stand in relation to your goals. If new goals have emerged, this is the time to make fresh investments for these. While having a steady approach is a virtue here, make some adjustments in the light of developments that have occurred over the past year.

Equity funds

Large-cap funds have fared worse than mid-cap and small-cap ones over the past one year (see table). Over this period at least, the conventional wisdom that large-cap funds tend to be more resilient than mid-cap and small-cap ones in a declining market was overturned. Nilesh Shah, managing director, Kotak Mahindra AMC, offers three reasons. “For the bulk of the previous year, FIIs were sellers of large-cap stocks, whereas domestic institutional investors (DIIs) were buyers of mid- and small-caps. Large-cap stocks are also more linked to global sectors like metal and oil, whereas mid- and small-caps are linked to domestic sectors. The latter has done better than the former, leading to stronger performance by mid- and small-cap stocks. Large-cap stocks’ earning growth decelerated or remained subdued throughout last year while mid- and small-caps delivered better growth,” he says.

Despite last year’s anomalous performance, investors should continue to have the bulk of their core portfolio, 70-75 per cent, in large-cap funds for stability, and only 20-25 per cent in mid-cap and small-cap funds. Large-caps could also fare better in the near future. Says Ashish Shankar, head of investment advisory, Motilal Oswal Private Wealth Management: “IT, pharma and private banks, whose earnings have been growing, will continue to do so. Public sector banks and commodity companies, whose earnings have been bleeding, will not bleed as much. Many might even turn profitable. FII flows turned positive this month and FIIs prefer large-caps. With the US Fed saying it won’t hike interest rates aggressively, global liquidity should improve. If FII flows continue to be stable, large-caps should do better.” Valuations of large-caps are also more attractive.

Debt funds

Among debt funds, the category average return of income funds and dynamic bond funds was lower than that of short-term, ultra short-term and liquid funds (see table). Explains Shah: “Last year, while Reserve Bank of India (RBI) cut policy rates, market yields didn’t soften as much. The yield curve became steeper. The short end of the curve came down more than the long end, which is why shorter-term bonds did better than longer-term gilts.”

Stick to funds that invest in high-quality debt paper, in view of the worsening credit environment. Shankar suggests investing in triple ‘A’ corporate bond funds. “Today, you can build a triple ‘A’ corporate bond portfolio with an expected return of 8.5 per cent. Many of these have expense ratios of 40-50 basis points, so you can expect annual return of around eight per cent. If bond yields come down, you could end up with returns of 8.5-9 per cent. If you redeem in April 2019, you will get three indexation benefits, lowering the tax incidence considerably.” Investors who have invested in dynamic bond funds should hold on to these. “A rate cut is expected in April. Yields will drop and there may be a rally in the bond market,” says Arvind Rao, Certified Financial Planner (CFP), Arvind Rao Associates.

CHANGES YOU NEED TO MAKE

Investment

- Fixed deposit rates from banks will be better than returns from the post office deposits in the new financial year

- Choose your tenure first and then, do a comparison of bank fixed deposit rates before making the final choice

- Invest in the yellow metal via gold bonds

Insurance

- If your liabilities have increased, revise term cover upward

- Revise health cover every three-five years to deal with medical and lifestyle inflation

- Revise sum assured on home insurance if you have added to household assets

Tax planning

- Conservative investors should invest in PPF at the earliest

- Those who can take some risk should bet on ELSS funds via SIP

- Invest Rs 50,000 in NPS

Traditional fixed income

The recent cut in small savings has jolted conservative investors. The rates on these have been linked to the average 10-year bond yield for the past three months. These will be revised every quarter now, make them more volatile. “People who want to invest in debt and want sovereign security should continue to invest in Public Provident Fund (PPF). No other instrument gives a tax-free return of 8.1 per cent with government security,” says Rao.

As for time deposits, financial planner Arnav Pandya suggests, “From April, fixed deposits of banks will give better returns than those of the post office. Decide on your investment tenure, see which bank is offering the best rate for that tenure, and invest in its deposit.” Lock into current rates fast, as even banks are expected to cut their deposit rates.

Tax-free bonds are another good option. Nabard’s recent issue carried a coupon of 7.29 per cent for 10 years and 7.64 per cent for 15 years. Beside getting tax-free income, investors stand to get the benefit of capital appreciation if interest rates are cut.

“People who have some risk appetite may also look at debt mutual funds and fixed deposits of stable companies,” adds Rao.

Gold

The sharp run-up in gold prices over three months, owing to the rise in risk aversion globally, took most people by surprise. The sudden spurt emphasises the need to stay diversified and have a 10 per cent allocation to the yellow metal in your portfolio. However, instead of using gold Exchange-traded funds (ETFs), which carry an expense ratio of 0.75-1 per cent, invest via gold bonds, which offer an annual interest rate of 2.75 per cent. The Budget made gold bonds more attractive by exempting these from capital gains tax at redemption.

Tax planning

Start investing in tax-saving instruments from the beginning of the year. “Don’t leave tax planning for the end of the year, otherwise you may have to scramble for funds,” says financial planner Ankur Kapur of ankurkapur.in. For those with the money, Pandya suggests: “Invest the entire amount you need to in PPF before the April 5. That will take care of tax planning for the year and you will also earn interest on your investment.”

Investors with a higher risk appetite could start a Systematic Investment Plan (SIP) in an Equity Linked Savings Schemes (ELSS) fund, which can give higher returns. “If you invest early in the year via an SIP, you will reap the benefit of rupee cost averaging,” says Dinesh Rohira, founder and Chief Executive Officer, 5nance.com. Pankaj Mathpal, MD, Optima Money Managers suggests linking all tax-related investments to financial goals.

If you live in your parents’ house and pay rent to them to claim House Rent Allowance benefits, which is perfectly legal, get a rent agreement prepared.

With 40 per cent of the National Pension System (NPS) corpus having been made tax-free at withdrawal in this Budget (the entire corpus was taxed earlier), this has become more attractive. “Open an NPS account if you have not done so already and enjoy the additional tax deduction of Rs 50,000,” says Anil Rego, CEO & founder, Right Horizons. In view of the low returns from annuities, into which 60 per cent of the final corpus must be compulsorily invested, don’t invest more than Rs 50,000.

Tax deduction under Section 24 is available on the interest repaid on a home loan. “Buying a property to avail of the benefit is not advisable if the family has a primary residence,” says Rego.

Insurance

While reviewing your financial plan, check if the term cover is adequate. A family’s insurance cover should be able to replace the breadwinner’s income stream. Financial planners take into account household expenses, goals like children’s education and marriage, and liabilities like home loans when deciding on a person’s insurance requirement. “If goals have changed or liabilities have increased, raise the amount of cover,” suggests Mathpal. Kapur says the premium rate is likely to be lower if you buy the term plan before your birthday.

Your health insurance cover might also need to be raised to take care of medical inflation. The same holds true for household insurance if you have reconstructed your house and the structure has become more expensive, or if you have added expensive assets. Rohira suggests buying add-on covers like accidental insurance and critical health insurance for comprehensive protection.

Source: http://goo.gl/iZ3KSx

ATM :: All you need to know about single premium life insurance

By Gargi Banerjee | May 21, 2015, 11.14 AM IST | Economic Times

Want to get over with buying an insurance policy at one go because you have some money lying idle? A single premium insurance policy is just the thing for you then. As compared to a traditional or a regular premium insurance policy where you pay insurance premiums at periodic intervals, this is a onetime payment solution for those who do not want to get into the hassle of periodic payments.

Once the premium payment has been made, you become the owner of a policy with a specific death benefit. It is literally a “fill it, shut it and forget it” kind of a policy, as you do not have to worry about paying any further payments or the lapse of your policy in case in forget to make any payments. All major insurers provide single premium life insurance policies for the benefit of their customers and you can use the help of a policy aggregator website to find out which one works best for you.

When should you buy a single premium policy?

Most people prefer to buy a single premium life insurance policy when they have a lump sum available with themselves. It may be a hefty tax fund, a cash gift from a relative an inheritance or some windfall gains in case of business owners. If you do not wish to spend this money right away and are wary of investing it in the markets, or you think there is some more insurance cover you could do with, you can certainly opt for a single premium life insurance policy.

Protect your wealth against taxation

A single premium life insurance policy provides you protection against the axe of taxes. You are given exemption of upto R 1.5 lakhs when you invest in a single premium life insurance policy. Further the sum assured is also tax free in the hands of the receiver. God forbid if something were to happen to you, your beneficiary would receive the money completely tax free. However do bear in mind, that on a single premium life insrance policy you will get the benfit of tax exemption only once, as you are investing in it for a single time only.

Forget about lapses

Since the policy is paid up in full upfront you never have to worry again about the policy getting lapsed in case you forget to pay the premium. It is valid till the entire term of the policy and renders the sum assured after the policy term comes to an end. Creates cash value.

When you make the payment of single premium on a policy you are creating an asset for yourself. In case you need to avail of a loan facility, this can come in handy and can be used as a collateral against your loan. Besides, the cash value of the investment you have made accumulates every year, without you having to invest year after year.

Thus as you can see, single premium life insurance policies, though usually not the preffered vehicle for securing one’s life, can certainly offer some benefits. But the largest factor you should keep in mind is the affordability part of it. So if you can think of sparing the lump sum and locking it away to take care of your insurance needs, go ahead and get yourself that single premium insurance policy.

Source: http://goo.gl/1nL5We

ATM :: Beware of these hidden charges on your home loan

HARSH ROONGTA | Tue, 29 Mar 2016-09:22am | dna

Shrinking interest rate margins have made several lenders to insert hidden charges to increase their margins by stealth.

The home loan industry has come a long way from the time when the only charges that you had to watch out for were the processing charges taken under various heads and pre-payment charges. Regulation has ensured that there are no pre-payment charges and competition has ensured that there is a greater degree of transparency around the processing fee, legal fee, valuation fee or technical charges. Competition has also ensured that there is hardly any difference in the interest rates charged by various home loan lenders. Unfortunately, the shrinking interest rate margins have made several lenders to insert hidden charges to increase this margin by stealth.

Here is a list of these charges:

Charge interest on the loan which is disbursed late – This is a common practice. The lender prepares a cheque, but it is not to be handed over till certain documents are received from the borrower and/or the seller. These documents normally may take a few days to a few weeks, and meanwhile, the interest meter is ticking for the borrower. This is not as small as it looks. On a loan of Rs 1 crore, the interest @9.50% works out to Rs 2,600 daily.

The cost of a 10-day delay in handing over the cheque (which is pretty common) means an additional cost of Rs 26,000 or 0.26% of the loan amount. You should negotiate with the lender that you will only pay interest from the day the cheque is actually handed over to the seller and not from the date mentioned on the cheque.

Advancing the EMI payment date – The EMI amount is calculated assuming that the payment will be made at the end of 30 days from the date of disbursement. If this EMI is paid earlier than 30 days, the cost becomes much higher than the stated cost. An example will illustrate this. If the disbursement is made on February 15, 2016, and the EMI is payable on the first of every month then typically you should pay interest equivalent to 15 days’ interest (from February 15, 2016, to March 1, 2016) and the EMI should start from April 1, 2016, only. However, most lenders will start off the EMI from March 1, 201, and still charge you for a full month’s interest. Again, the difference is not as small as it sounds. 15 days’ extra interest for a Rs 1 crore loan @9.50% works out to Rs 39,000 or 0.39% of the loan amount. Again, you can negotiate with the lender to make sure that this additional hidden interest is not charged to you. Unlike the first point which is easily understood, this point is technical and the lender can run loops through the borrower while explaining how the EMI is calculated.

Forcing borrowers to buy expensive insurance products – Lenders have tied up with life and general insurance companies to provide life, disability and property insurance to borrowers and they force you to take these policies. The lenders earn fat commissions on the sale of these insurance policies and even though officially not permitted, they force the borrowers to sign up for these policies. It is a good practise to have such type of insurance policies when you take a loan, but the problem is that the policies being hawked by the lenders are hugely overpriced, reflecting the captive base of borrowers and the fat commissions for the lender inbuilt in such policies. To avoid having to pay for these overpriced policies, you can negotiate with the lender that you will buy these policies on your own. In all probability, you will get the exact same policy from the same insurance provider as what the lender is pushing at a fraction of the cost that the lender will charge.

Forcing borrowers to take a credit card or some other add-on products – In most cases this is offered for free while not stating that it is free only for the first year and would have an annual fee every year after that. You can easily negotiate your way out of this one.

Whilst these are the “extra” charges that lenders take from borrowers, there is a charge that they are unfairly accused of taking. For example, in Maharashtra, you have to pay a stamp duty of 0.20% of the loan amount on the document creating the security in favour of the lender. It is obvious that this charge will be recovered from the borrower (it is also mentioned in the loan agreement as recoverable from the borrower), but I have heard many borrowers complain that this is a hidden charge sprung upon them. This document is in favour of the borrower as it is conclusive proof that documents have been handed over to the lender. This is extremely useful when the loan period ends because there have been increasing the number of cases where the lenders have misplaced the title deeds and claim that these were never deposited with them in the first place. A stamped and registered document will prevent the lender from making any such claims.

In this new age, the lenders depend on the borrowers lack of attention to slip in the extra charges. It makes eminent sense for the borrowers to take the help of professionals to help them navigate through this process. The fee payable to such professionals will be more than made up by the savings in these “extra” charges.

Source : http://goo.gl/ImwYEb

ATM:: 9 smart ways to save tax

Babar Zaidi | TNN | Jan 11, 2016, 08.57 AM IST | Times of India

Do-it-yourself tax planning can be rewarding and challenging. Rewarding, because you can choose the tax-saving instrument that best suits your needs. Challenging, because if you make the wrong choice, you are stuck with an unsuitable investment for at least 3-5 years. This is where our annual ranking of best tax-saving options can prove helpful. It assesses all the investment options on seven key parameters—returns, safety, flexibility, liquidity, costs, transparency and taxability of income. Each parameter is given equal weightage and a composite score is worked out for the various tax-saving options.

While the ranking is based on a robust methodology, your choice should also take into account your requirements and financial goals. We consider the pros and cons of each option and tell you which instrument is best suited for taxpayers in different situations and lifestages. We hope it will help you make an informed choice. Happy investing!

ELSS FUNDS

ELSS funds top our ranking because of their tremendous potential, high liquidity and transparency. The ELSS category has given average returns of 17.8% in the past 3 years. The 3-year lock-in period is the shortest for any Section 80C option.

If you have already fulfilled KYC requirements, you can invest online. Even if you are a new investor, fund houses facilitate the investment by picking up documents from your house and guiding you through the KYC screening. ELSS funds are equity schemes and carry the same market risk as any other diversified fund. Last year was not good for equities, and even top-rated ELSS funds lost money. However, the funds are miles ahead of PPF in 3- and 5-year returns.

The SIP route is the best way to contain the risk of investing in equity funds. However, with just three months left for the financial year to end, at best, a taxpayer will manage 2-3 SIPs before 31 March. Since valuations are not stretched right now, one can put in a bigger amount.

SMART TIP

Opt for the direct plan. Returns are higher because charges are lower.

ULIP

The new online Ulips are ultra cheap, with some of them costing even less than direct mutual funds. They also offer greater flexibility. Unlike ELSS funds, where the investment cannot be touched for three years, Ulip investors can switch their corpus from equity to debt, and vice versa. What’s more, there is no tax implication of gains made from switching because insurance plans enjoy exemption under Section 10 (10d). Even so, only savvy investors who know how to use the switching facility should get in.

SMART TIP

Opt for liquid or debt funds of the Ulip and gradually shift the money to the equity fund.

NPS

The last Budget made the NPS attractive as a tax-saving tool by offering an additional tax deduction of Rs 50,000. Also, pension fund managers have been allowed to invest in a larger basket of stocks.

Concerns remain about the cap on equity exposure. Besides, the taxability of the NPS on maturity is a sore point. At least 40% of the corpus must be put in an annuity. Right now, the income from annuities is taxed at the normal rate.

SMART TIP

Opt for the auto choice where the equity exposure is linked to age and comes down as you grow older.

PPF AND VPF

It’s been almost four years since the PPF rate was linked to the benchmark bond yield. But bond yields have stayed buoyant and the PPF rate has not fallen. However, the government has indicated that it will review the interest rates on small savings schemes, including PPF and NSCs. If this is a worry, opt for the Voluntary Provident Fund. It offers that same interest rate and tax benefits as the EPF. There is no limit to how much you can invest in the VPF. The contribution gets deducted from the salary itself so the investor does not even feel it go.

SMART TIP

Allocate 25% of your pay hike to VPF. You won’t notice the deduction.

SUKANYA SAMRIDDHI SCHEME

This scheme for the girl child is a great way to save tax. It is open only to girls below 10. If you have a daughter that old, the Sukanya Samriddhi Scheme is a better option than bank deposits, child plans and even the PPF account. Accounts can be opened in any post office or designated branches of PSU banks with a minimum Rs 1,000. The maximum investment in a financial year is Rs 1.5 lakh and deposits can be made for 14 years. The account matures when the girl turns 21, though up to 50% of the corpus can be withdrawn after she turns 18.

SMART TIP

Instead of PPF, put money in the Sukanya scheme and earn 50 bps more.

SENIOR CITIZENS’ SCHEME This is the best tax-saving instrument for retirees. At 9.3%, it offers the highest interest rate among all Post Office schemes. The tenure is 5 years, extendable by 3 years. Interest is paid quarterly on fixed dates. However, there is a Rs 15 lakh overall investment limit.

SMART TIP

If you want ot invest more than Rs 15 lakh, gift the amount to your spouse and invest in her name.

BANK FDS AND NSCs

Though bank FDs and NSCs offer assured returns, the interest earned on the deposits is fully taxable. They are best suited to taxpayers in the 10% bracket or senior citizens who have exhausted the Rs 15 lakh limit in the Senior Citizens’ Saving Scheme.

SMART TIP

Invest in FDs and NSCs if you don’t have time to assess the other options and the deadline is near.

PENSION PLANS

Pension plans from insurance companies still have high charges which makes them poor investments. They also force the investor to put a larger portion (66%) of the corpus in an annuity. The prevailing annuity rates are not very attractive. Pension plans launched by mutual funds have lower charges, but are MFs disguised as pension plans. Moreover, they are debtoriented plans so they are not eligible for tax benefits that equity plans enjoy.

SMART TIP

Invest in plans from mutual funds. They offer greater flexibility than those from life insurers.

INSURANCE POLICIES

Traditional life insurance policies remain the worst way to save tax. Still, millions of taxpayers buy these policies every year, lured by the “triple benefits” of life insurance cover, longterm savings and tax benefits. Actually, these policies give very little cover. A premium of Rs 20,000 a year will get you a cover of roughly Rs 2 lakh. The returns are very poor, barely 6% if you opt for a 20-year plan. And the tax-free income is a sham. Going by the indexation rule, if the returns are below the inflation rate, the income should anyway be tax free. The problem is that once you sign up for these policies, they become millstones around your neck.

SMART TIP

If you can’t afford to pay the premium, turn your insurance plan into a paid-up policy.

Source: http://goo.gl/DWqo4K

NTH :: EPFO Insurance Scheme – Hassle free: Nominee entitled for benefits, irrespective of cause of death

Here’s all that you should know about the employee deposit linked insurance scheme.

Written by Adhil Shetty | Published:Dec 11, 2015, 2:00 | Indian Express

Not many investors know that the retirement benefits administration body Employees’ Provident Fund Organisation (EPFO) offers an insurance scheme covering all employees working with organisations as part of the EPF.

Along with the Employee Provident Fund and the Employee Pension Scheme, the Employee Deposit Linked Insurance (EDLI) forms the troika of the social security schemes administered by the Employees Provident Fund Organisation.

Here’s all that you should know about the employee deposit linked insurance scheme.

What is Employee Deposit Linked Insurance?

Employee Deposit Linked Insurance is a term insurance plan offered by the EPFO. The scheme offers life coverage for all employees working with the organised sectors and enrolled in EPF. The scheme is administered by the Employees Provident Fund Organisation and is applicable to all companies who are part of the EPF.

The EDLI scheme works just like a group term insurance plan where if an employee dies during the service period, his family or nominee gets the sum assured up to a certain maximum limit as defined by the rules of the EDLI scheme.

Protection coverage under the EDLI scheme

Being a group term insurance plan, EDLI offers a 24-hour-protection to the employees as part of the scheme. This means the insured does not need to be at their workplace for the scheme to be valid or applicable. The scheme protects them 24×7 irrespective of whether they are at work or not.

The coverage and premium charges under the EDLI scheme are the same for every employee irrespective of any factor including age or gender.

Employees contribute 0.5 per cent of their monthly basic pay and dearness allowance (capped at a maximum of Rs 15,000) as premium for this, and the coverage is linked to the premium.

The family or nominee of the policyholder (employee) under the EDLI scheme will get benefits irrespective of the cause of death including illness, accident, or natural causes.

EDLI earlier had stipulated 12 months of service with the same employer as a mandatory condition for being protected under the insurance scheme. Now, there is no such minimum limit of service and employees are covered under the EDLI scheme as soon as they start working with a company.

Extent of claim available

As per the recently issued EPFO guidelines, the maximum claim amount is capped at 30 times of the last drawn salary of the policy holder. Along with the claim amount, EPFO also offers a bonus of Rs1.5 lakh for each claim.

So the maximum claim amount you can avail under the EDLI scheme is therefore calculated as 30 times Rs 15,000 plus the Rs 1.5 lakh bonus, which comes to Rs 6 lakh. The previous limit was Rs 3.6 lakh only.

How to file for a claim

Before you opt for a claim under the EDLI scheme, make sure that you have all the required documentation in place. You will need:

* Death certificate of the employee as issued by the local municipal corporation.

* Legal heir certification or succession certificate.

* If the employee was working with a company exempted under the EPF Scheme 1952, the employer will need to submit the PF details of last 12 months.

* Once you have all the documents in place, you will need to submit the EDLI claim form. The form is available at: http://www.epfindia.gov.in/site_docs/PDFs/Downloads_PDFs/Form5IF.pdf

You should also submit Form 20 and Form 10D / 10C to claim provident fund dues. Before submitting the claim form, you will need to get it attested by the employer.

Source : http://goo.gl/H6OSfl

ATM :: Stealing from your wallet? 7 entrapments from banks that you should be aware of

By Sangita Mehta, ET Bureau | 13 May, 2015, 10.48AM IST | Economic Times

A bank’s facilities typically come loaded. For the unsuspecting customer, it could just be a question of filling out a fixed deposit form or being granted a home loan. But there are some entrapments the bank will slip in that you need to be aware of, says Sangita Mehta.

HOME LOAN: Double Trouble

Watch out: When you apply for a home loan, the bank will sell you property insurance — which covers damage to property — and mortgage protection term insurance, which covers the loan in the event of the borrower’s death

What you should know: The housing society may already have property insurance. You don’t have to opt for an insurer the bank has a tie-up with. Ensure the premium is not clubbed with the loan, in which case, you will have to pay interest

CREDIT CARD: Take it or Leave it

Watch out: Banks often sell credit cards with the promise that for the first year, they will not charge any fee and the customer can discontinue it from the second year. However, at the end of the second year, the card company sends an innocuous mail stating they will renew the card for a fee unless the customer explicitly rejects it.

What you should know: The Reserve Bank of India has banned banks from giving such negative options. Customers should ideally use the credit card of a bank they do not have a savings bank with. In case of a dispute, banks often debit money from the borrower’s account

DEPOSITS: Auto Route

Watch out: When you’re opening a fixed deposit, watch out for ‘auto renewal’ in the fine print

What you should know: If you do not opt for auto renewal, the money is transferred to the savings account after maturity, where the bank offers about 4% interest as against 7-9% on FDs. You may forget to renew the deposit and the bank won’t remind you. When you tick that ‘auto renewal’ box, the bank cannot charge you a penalty on premature withdrawal of the deposit

ATM, CYBER FRAUD: Cry ‘Thief’

Watch out: If you find a fraudulent transaction in your account, immediately notify the bank

What you should know: If you are the unfortunate victim of an ATM or e-transaction fraud, watch out: the bank is liable to prove its innocence. If the bank is not notified, the maximum loss to you is `10,000 Postnotifi cation, the customer is not liable to bear any cost

LOCKER FACILITY: Keep your Freedom

Watch out: Banks put a price tag on a ‘scarce’ commodity like the bank locker

What you should know: Your bank may ask you to invest in fi xed deposits or mutual funds or even third party insurance, with the bank locker, even though they are not allowed to to do so by the RBI. You anyway need to pay an annual rental

PERSONAL LOANS: Don’t Rush to Pre-pay

Watch out: Banks have stiff conditions on prepayment of personal loans

What you should know: The RBI has mandated banks to not charge a penalty for pre-payment of a home loan if the interest is on a floating rate. But the rule does not apply for other personal loans. Some banks charge as much as 5-10% on pre-payment of loans. Some banks don’t even permit you to repay the loan for the fi rst six months or one year

PROCESSING FEES: No Free Lunches

Watch out for: For every home loan, auto loan and personal loan, banks charge a processing fee, which can be steep

What you should know: This fee is mostly at the discretion of the bank and can be as high as 1 percentage point, which itself will infl ate your outgo. If any bank says they have a lower rate, ensure the processing fee is also low.

Source : http://goo.gl/r0S6eK

ATM :: SBI MaxGain Home Loan Review – With FAQ’s

By Ashal Jauhari | 14th April 2013 | AsanIdeasforWealth.com

In this article we are going to share SBI Maxgain Home Loan review with you. Now a days many home loan borrowers are opting a particular type of home loan from State Bank of India which is called Max Gain because it has many advantages compared to other kind of home loan scheme’s. In this SBI Max Gain home loan, an Overdraft (OD) account is assigned to the customer’s home loan & any amount parked by customer is treated as loan repayment for the purpose of interest calculation, for the days, the amount stays there in that OD account. As on date following banks are offering similar types of home loan to their customers SBI, IDBI, CITI, HSBC & Standard Chartered. Punjab National Bank can also be added in this list but it’s offering a combo of normal loan + Overdraft. In this article, we are going to discuss only SBI Max Gain as in OD linked home loan, the maximum business is with SBI & the most discussed topic on Jagoinvestor Forum is also related to SBI Max Gain Scheme

What is an Overdraft account?

Before we discuss Max Gain, first understand, what is an Over Draft Account? All of us are well aware of functioning of an ordinary saving bank (SB) account. Here account operates between zero to positive & positive to zero. As we deposit our money, it’s used by bank & we get interest on our money from bank. In case of an OD account, bank first ask for a security & then assign a credit limit on the basis of the market value of that security. This security may be Fixed Deposits, Insurance Policies, National Saving Certificates, Shares, Mutual Fund units, house/commercial property etc. Now when we are using this assigned credit limit, the amount is going from zero to negative zone & when we are repaying, it’s coming from negative to zero. As we are using bank’s money in this case, the interest ‘ll be paid by us to bank. That’s how an OD account works.

So what is the correlation between Max Gain home loan & Over Draft account?

For Max Gain borrowers, State bank of India opens an Over Draft account where the Credit limit as discussed above is equal to the loan value assigned to the borrower. Here underlying security is the home you have purchased or constructed from that loan amount. Now as & when you are parking any surplus amount into this OD account, the parked amount is treated as payment towards loan (effectively you are bringing down your loan liability from negative towards zero position) and thus the interest ‘ll be charged only on the difference amount i.e. total loan amount – parked surplus amount.

What is the primary benefit of SBI Max Gain Scheme?

Well the primary benefit of MG is to keep your liquidity intact & still bringing down your interest outgo. To understand it better, please imagine a situation you are running a home loan of 30L Rs. & now you do have 2L Rs. with you to prepay. In normal home loan, your 2L Rs. ‘ll be accepted by bank & adjusted towards home loan & your amount is gone forever so no liquidity for you of that 2L Rs. amount. On the other hand, if you are MG customer, simply park those 2L Rs. in your MG account & your interest outgo ‘ll be lower from that month itself till those 2L Rs. or a part of it is there as surplus in MG account.

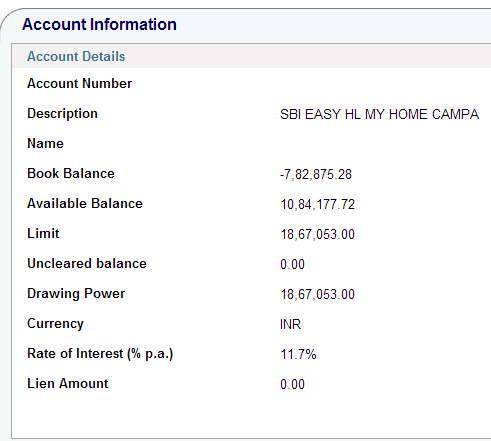

What is Drawing Power ?

Drawing Power is nothing but your as on date actual outstanding loan amount. Before final disbursal or start of loan repayment, it’s your sanctioned loan amount. Once your EMI starts, it’s your as on date actual outstanding loan amount. Please check Image below, Drawing Power here is 1867053 Rs. as on date.

What is Available balance?

Before final disbursal, it’s the sum of undisbursed amount + parked surplus & post final disbursal, it’s your parked surplus amount which is available to withdraw. Please check Image below, Available Balance here is 1084177.72 Rs. as on date.

What is book balance?

It’s the adjusted loan amount arrived after deducting the Available Balance amount from Drawing Power. In your account statements it’s shown with a negative sign. Please check Image below, Book Balance here is – 782875.28 Rs. as on date.

Is there any extra interest for Max Gain?

No, the interest for home loan is same in SBI be it for normal home loan or for Max Gain.

I’m an existing SBI home loan customer. Can I convert my old term loan to Max Gain?

Yes, you can. Please contact your loan serving branch or RACPC for the required paperwork to be done. This may be an outdated info so please do check with your loan serving branch for current day rules on conversion.

I have taken the Max Gain for an Under Construction Property. Can I park surplus amount to save on interest outgo?

The answer is yes & no both. Yes you can park your surplus during under construction phase but do remember SBI is disbursing partially at this juncture & in case due to any emergency you want to liquidate your surplus, SBI ‘l not allow the same. so park only that much surplus, you feel you ‘ll not need even in an extreme emergency.

If I’m parking some money on monthly basis or in lump sum, will my loan term come down or EMI go down?

No. Neither your EMI ‘ll come down nor your loan term. The only saving is in terms of interest outgo. To understand it better, Let’s assume a test case of loan amount 30L Rs. @ 10% Rate of Interest for 20Y term. The normal EMI for these nos. ‘ll be 28951 Rs. The break up of your EMI for first month ‘ll be 25000 Rs. interest & 3951 Rs. for principal repayment.

Now if you do have 2L Rs. surplus in the very first month & prepay the same as below –

Case – 1 Normal home loan

Your 2L Rs. is gone & outstanding loan amount ‘ll come to 2796049 & interest outgo ‘ll still be 25000 Rs. but the no. of months ‘ll come down from original 240 to 198 months.

Case – 2 Max Gain home loan

Your 2L Rs. are parked in that OD account & the interest for the very first month ‘ll be calculated on 28L Rs. & thus it ‘ll be 23334 & thus there‘ll be an interest saving of 1667 Rs. which‘ll remain available in your OD account as surplus along with your parked surplus 2L Rs. so for next month, the parked surplus amount ‘ll be 201667 Rs.

Please do note in case 2 above, Your loan term is still 240 months but the saving of interest ‘ll keep on increasing on mly basis from the parked surplus & of course the liquidity of those 2L Rs. is there.

How can I calculate my saving in Max Gain?

To know your actual saving, first of all please demand a loan amortization schedule from your loan serving branch & now for each month compare the scheduled interest outgo as per your loan amount. schedule & the actual interest outgo.

What should I do to maximize the savings in Max Gain?

If you are paying your EMIs from SBI’s SB account, you can maximize your benefits. How? here it goes. Say 15th is the EMi date on which EMi amount is debited from your SB acct. Now in a normal home loan, people ‘ll keep at least 2-3 months’ EMI amount as buffer in SB account. but in case of Max Gain, you do not need to keep buffer in SB account. Keep this buffer amount also in your MG account along with your routine surplus amount. now use the power of net-banking of SBI for your own good & create a schedule transaction of your EMI amount 28951 Rs. (in the above example) to be transferred on 13th of every month from MG account to SB account. At a time you can schedule for next 12 months by using standard instruction. So it’s technology that’s helping you.

I can transfer to MG account from my existing net-banking enabled SB account but reverse is not happening. why?

The answer lies in the fact that Net-banking transaction rights on your MG account is not enabled yet by your loan serving branch. if final disbursal is done, you can apply for transaction rights. if only partial disbursement has been done, sorry, you can’t apply for transaction rights till final disbursal.

Is it mandatory to purchase property insurance & life insurance along with Max Gain?

Having property insurance as well as sufficient life insurance is compulsory but purchasing the same from SBI’s sister cos. like SBI General ins. & SBI Life Ins. is not at all mandatory. if you feel that policies are being cross sold to you to exploit your position (home loan seeker), please contact the AGM of your local RACPC where your loan application is under processing.

Is SBI charging higher processing fee for Max Gain?

No, as on date there is no differentiation in fee for term loan & Max Gain but SBi reserves the rights to charge different fee.

Can I claim section 80C principal repayment benefit for the surplus amount parked in Max Gain?

The answer is NO. Only the regular principal repaid by you from your EMI as part of your loan amortization schedule is available for tax benefit under section 80C. the parked surplus amount is liquid money & you can withdraw it any time, hence it’s not considered as actual repayment of loan & thus not eligible for tax benefit.

Can I avail cheque book & ATM card for my Max Gain account?

Yes, as & when you‘ll demand these, SBI ‘ll offer you the same. In case you are already holding an SBI SB acct. linked ATM card, you have the option to link your MG acct. also with this existing ATM card.

Can I enroll my MF SIPs in Max Gain?

Yes but do note, there should be a surplus balance i.e. available balance on the date of SIP, else your ECS or SI mandate ‘ll bounce.

Can i pay for my utility bills, credit card payments, online shopping from Max Gain?

Yes, you can do all this & more. In fact it’s in your best interest that you treat your MG account as your primary money parking account & route all your transactions through it so that money is lying there for maximum possible time & thus helping you to bring down your interest outgo.

I used my MG account ATM card to withdraw cash from other bank’s ATM & I was charged the money very first time in the month. Why?

The reason is, as per RBI’s circular 5 transactions on other banks’ ATM are free only for SB account & in this case, you forget the point that your MG account is not SB account. it’s an overdraft account.

For an imaginary situation, my loan amount is 30L Rs. & parked surplus amount is also 30L Rs. Does it mean, my loan is closed & I can claim my property papers from SBI?

No, your loan is not closed. Only interest outgo ‘ll become zero & EMi ‘ll remain continue as it is. Yes the interest part of your EMI ‘ll keep on accumulating in your MG account. If you want to close your loan at this point, you w’d have to inform SBI in written & now SBI ‘ll adjust your parked surplus amount towards the outstanding loan amount. you ‘ll lose the liquidity of your money but loan ‘ll be over & now you can get your property papers back.

How can I transfer my loan from other banks to SBI Max Gain?

For loan transfer, first of all contact your existing lender & ask for following things.

1. Loan Account statement from day one.

2. List of Documents, which were submitted by you at the time of availing original loan. In day to day language of bankers, it’s called LOD.

3. As on date outstanding loan balance with applicable interest, penalty & any other fee to close the loan.

Now contact, the nearest SBI Branch (if you do have an existing SB account with SBI, it’s advisable to contact there for ease of operation). Inform in that branch that you want to transfer your loan from existing bank to SBI Max Gain. fill the application form, submit the necessary papers & SBI’s RACPC ‘ll do the back ground job.

Once SBI is ready to accept the transfer, it ‘ll issue you a sanction letter of the loan amount & ‘ll ask you to go for loan related agreement documentation work with SBI. If you are not having property insurance, SBI may ask to purchase one. Same ‘ll be the case for your life insurance. Once legal documentation is over, the cheque of the loan balance ‘ll be issued directly into the name of the bank in question. After the amount is credited to your existing bank, within next 20-30 days, you ‘ll get the original documents submitted by you, from the existing bank. Now you w’d have to submit these documents to SBI. In some states like Gujarat, Maharashtra, Karnataka, SBI may ask to go for registration of mortgage deed on your property in the office where your property was originally registered in your name.

|

SBI Max Gain |

Normal Home Loan |

|

Liquidity of your part prepayments is there |

No Liquidity. Money is gone for ever, once you prepay. |

|

A bit complex to understand |

Easy to understand |

|

For people who can generate regular surplus amounts |

For people who can only manage regular EMIs |

Source : http://goo.gl/5q11YV

NTH :: Life insurance most preferred investment for affluent Indians

PTI | Jan 30, 2015, 12.34 PM IST | Times of India

MUMBAI: Life insurance has emerged as the most preferred investment option for Indian households with an income up to Rs 25 lakh, says a survey.

Seventy per cent of affluent population of the country, who hold investments other than cash, have put their money in life insurance, while 64 per cent among them have gone for fixed deposits, according to the DSP BlackRock India Investor Pulse Survey.

It is followed by their investments in other financial instruments like shares (46 per cent), equity mutual funds (33 per cent), fixed maturity plans (27 per cent), tax-free bonds (25 per cent) and so on, it said.

“Even though the larger current ownership is in insurance and fixed deposits, there is a growing awareness among the educated affluent category of investors in the country to move more money from cash and deposits to other form of investments like mutual fund and bond,” said DSP BlackRock Executive Vice President, Head (Sales) and Co-Head (Marketing), Ajit Menon, while unveiling the survey report here today.

People living in the country invest 25 per cent of their monthly take home pay, which is higher than the global average of 17 per cent, it said.

When it comes specifically to asset allocation, Indians are more likely to invest in property than the global average, it added.

Equities and bonds are also important asset classes accounting for 13 per cent and five per cent of the total value of saving and investment products, the survey said.

Majority of Indians (56 per cent) feel their economy is getting better, way ahead of the global average of 22 per cent. The huge margin of positivity extends to their financial future with 81 per cent of Indian respondents feeling positive as compared to 56 per cent globally, it added.

A large proportion of Indian respondents also feel that they are in control of their finances (75 per cent) as compared to the global average of 55 per cent, second only to China (84 per cent).

Source : http://goo.gl/kYW3BE

ATM :: Home Loan Insurance Vs Term Insurance Policy

India Infoline News Service | Mumbai | December 26, 2014 19:16 IST | IndiaInfoline.com

The financial planners suggest the individuals to pick a term plan so as to cover the loan.

If you are finding the best way to save your home loan, then this article is for you. Here, we will discuss two options, term insurance policy, and home loan insurance.

One of the most important dreams in a person’s life is to buy his or her home. To fulfill a dream, an individual takes a home loan which puts the house on mortgage. The home remains with the lender till the time buyer doesn’t pay the complete loan amount. However, it is important to safeguard the property so that in the event of any accident the home remains with the family. The motive is achieved by a term insurance policy or home loan insurance.

The financial planners suggest the individuals to pick a term plan so as to cover the loan. However, there are other loan protection plans designed and offered by the insurance companies to take care of the outstanding home loans in the event of unforeseeable circumstances.

A loan insurance protection plan covers the balance amount to be paid in case of death of the borrower. The plan is specifically made for high-value mortgages. The premium rates are higher and depend on several factors including the loan amount, age of the borrower, the medical history of the borrower and the loan tenure.

The loan insurance cover acts as a surety to the lenders. The loan cover is bundled with the loan amount. The borrower can either pay the initial premium himself or he can get it funded from the lender. The options come with different tax implications. If the borrower pays the premium, he will be eligible for tax deduction under Section 10(10D) and Section 80C. However, if it is paid by the lender and is included in the loan amount, the borrower will not get any claim deduction.

A vanilla term insurance is a better alternative than a mortgage insurance policy. The term plans are cheaper and also provide high cover to the borrower.

The insurance provided by the loan cover will gradually reduce as the loan gets repaid. However, the insurance cover stays constant in a term plan. It will cover the outstanding home loan and will also meet the other financial requirements of the borrower’s family in case of unfortunate death.

The loan insurance is of little significance once borrower has prepaid loan. It is the same case when the sum assured declines with the time. It is the reason term plan should be considered over loan insurance.

Also, loan cover insurance is associated with a single premium option which implies that if the borrower prepays the loan amount, there will be no impact on insurance cover or premium. There will be other portability issues if borrowers want the loan to be refinanced by another lender.

In case borrower wants to increase the loan tenure due to hike in interest rates, the cover may not be sufficient to fully cover his home loan. Considering all the factors, it is clear that a term loan is better than home loan insurance.

ATM :: Don’t only insure your life, ensure your home loan is paid!

By: CreditVidya | December 26, 2014 9:24 pm | Financial Express

Introduction:

It is one thing to get a home loan and a different ball game to repay the loan, the tenure of which may run over a decade. With such long period of commitments, it is bound to put a person in an insecure mode as anything can happen to the loan holder. To ease yourself of the worries, it is important to take an insurance to protect your life to cover this loan burden in case of any casualty. That way your family inherits your home and not your loan burden.

Story:

Buying a house is a big deal today simply because of the high expenses one has to incur while buying. It can be overwhelming in many cases, because you will have to literally pull out all your savings to get it. These days a lot of funding burden has been reduced thanks to the home loans. The lenders also offer you an insurance policy to cover your home loan in case something happens to your life. You have the choice to choose any insurance policy from any company and can say no the bundled offer which in most cases will be from a group company and might come to you at a higher premium.