Tagged: Home Insurance

ATM :: Why it makes more sense to switch your home loan after this interest rate cut

By Sunil Dhawan | ECONOMICTIMES.COM| Updated: Jan 04, 2017, 11.23 AM IST

The start of the new year may have something to cheer for the home loan borrowers. Several banks have significantly reduced the interest rates charged on these loans.

The State Bank of India (SBI) has lowered its home loan rate from 9.10 per cent to 8.60 per cent and ICICI Bank from 9.10 percent to 8.65 percent, HDFC at 8.7 per cent, with other banks set to follow suit. Effectively, home loan rate has come down by an average of about 0.4-0.5 per cent after these announcements.

Noticeably, SBI’s one-year MCLR is at 8 per cent which makes the spread on its home loan 0.6 per cent. So, even though the MCLR of banks have fallen, the actual home loans are not at MCLR. Still, the writing on the wall is clear – there is more room to cut home loan rates by the banks.

Borrowers on base rate should switch now

If not all then at least the old borrowers who have been servicing their EMI’s based on the erstwhile base rate system of lending, stand to benefit. Even though bank’s base rate hasn’t come down as much, they now have a stronger reason to switch to the current MCLR-based lending. With the recent interest rate cuts on loans by banks the differential between base rate at which old borrowers are servicing their loan and the current MCLR is widening.

For those who had taken loans after July 1, 2010, but before April 1, 2016, the loans are linked to the bank’s base rate. And for most of these borrowers, the home loan interest rate is around 10 per cent. After the recent rate cuts announced by banks, the average MCLR has fallen to about 8.75 percent or even lower. This differential of 1-1.25 percent in base rate and MCLR will help old borrowers to switch to MCLR and save on total interest outgo.

Why to switch now

The primary reason to switch from base rate to MCLR has to be the sluggishness seen in banks’ passing on the benefits of RBI rate cuts to borrowers. RBI’s repo rate cuts were not reflecting in the bank’s base rate but are a part of the factors that goes into calculating the bank’s MCLR so, the moment repo rate changed, MCLR was impacted.

Further, the MCLR takes into account the marginal cost of funds which includes the rate at which the bank raises deposits and other cost of borrowings. With banks flush with funds post demonetisation, the bank’s CASA deposits (current account-savings account) have swelled and have given the banks the leeway to go for such major rate cuts.

The base rate, on the other hand, has seen only marginal reduction since last 24 months. Post demonetisation, banks are expected to wait and see the impact once the restrictions on cash withdrawals are removed. If the funds don’t move out from the banking system in significant amounts, further rate cut is expected.

MCLR based borrowers

For the new home loan borrowers who have taken loan after April 1, 2016, there’s not much immediate benefit from the recent rate cuts. For most MCLR-linked home loan contracts, the banks reset the interest rate after 12 months for their home loan borrowers. So, if someone has taken home loan from a bank say in May, 2016, the next re-set date will be in May, 2017. Any revisions by RBI or banks will not impact their EMIs or the loan till the reset date

What’s MCLR mode of lending

A new method of bank lending called marginal cost of funds based lending rate (MCLR) was put in place for all loans, including home loans, given after April 1, 2016. Under the MCLR mode, the banks have to review and declare overnight, one month, three months, six months, one year, two years, three years rates each month.

Watchouts

In a falling interest rate scenario, quarterly or half-yearly could be a better option, provided the bank agrees. But when the interest rate cycle turns, the borrower will be at a disadvantage. After moving to the MCLR system, there is always the risk of any upward movement of interest rates before you reach the reset period. If the RBI raises repo rates, MCLR too, will move up.

Options for base rate borrowers

When the interest rate on your loan goes down banks, on their own, typically reduce the tenure automatically (instead of reducing EMI amount) and thereby, transfer the benefit of lower rate to the customers.

The base rate borrowers now have two options – switch to MCLR based lending with the same bank or else transfer i.e. get the loan refinanced from another bank on MCLR mode. One may also continue the loan on base rate, especially if the loan term is nearing the end.

The RBI has made it clear that banks should allow base rate borrowers to switch to MCLR. The existing loans can run till maturity or borrowers can switch to MCLR on mutually agreed terms.

Switching from base rate to MCLR within the same bank

It makes sense to switch if the difference between what you are paying and what the bank is offering now as MCLR is significant. And also in cases where the time for the home loan to finish is not near.

Switching loan from base rate to MCLR with another bank (refinancing)

If your bank is offering a high home loan interest rate (MCLR plus spread) then look for refinancing. Get the loan refinanced from a bank offering a lower interest rate. You may have to incur processing fees. However, banks are not allowed to charge foreclosure or full repayment charges. Other charges may include lawyer’s fees, mortgage charges, etc. Remember, the bank may ask you to buy a home loan insurance cover plan, which is not mandatory. Get the loan insured through a pure term insurance instead, in addition to any insurance that you already have.

Conclusion

Switching to MCLR in itself should help you save a substantial amount. In addition to switching the loan from base rate-linked to MCLR and thereby saving interest, prepare a systematic partial prepayment plan to further reduce the interest burden. It’s after all better to up your home-equity rather than making it a highly leveraged buy-out.

Source: https://goo.gl/6R5mh0

ATM :: Risk cover for your home loan

BALAJI RAO | The Hindu

A term assurance provides financial stability in case of unforeseen events and ensures that EMIs are paid.

Rangan is 35 years old, married, has twins aged three years. His wife, Ragini, is a home-maker. She teaches music to a few young aspirants and earns a small amount of money every month that takes care of her personal expenses. But Rangan is the main earning member of the family. He works for an IT company, earns well, has a home loan which still has another 17 years of repayment (Rs.50 lakh more to be paid including principal and interest), has a car loan to be paid for another three years, and has to take care of his children’s education over the next 20 years.

Rangan is bit worried about unforeseen events such as accidents, illness, loss of job and premature death. He has a beautiful house on which he had spent quite a bit of his savings and also taken a hefty loan. He also wants to secure his family financially.

What could Rangan do that ensures his family is not into any financial mess if some unforeseen event occurs? The one solution for all these is insuring the risks adequately. There is a general confusion due to lack of financial education and awareness that insurance plans are purchased to meet life’s events, whereas the purpose of insurance is to protect against unforeseen events leading to financial risk. Financial goals and risks should not be mixed; it would be a bad marriage.

Segregate goals, risks

Rangan should segregate his financial goals and financial risks. His goals are to meet his children’s education expenses, their marriage, expenses upon retirement some 25 years from today, vacations, upgrading of house, upgrading of car, pre-closing his home loan, etc. His financial risks are losing his job, health scare leading to hospitalisation, and premature death that could risk his house (not being able to pay the EMIs).

While Rangan is investing in financial instruments such as debt and equity to meet his financial goals he has inadequate cover to meet his financial risks. He should split his risks in such a way that he manages them diligently with low investments. Let’s see how Rangan can do it.

Three elements

He should buy three separate pure risk covers by way of term assurances. For the home loan outstanding, he should buy a term assurance which could cost him Rs.5,000 per annum (approx.) for a period of 17 years. In case of premature death the insurance company would pay his legal successor the sum assured which could be utilised to repay the home loan and retain the house.

For the children’s education he should buy another term assurance plan for Rs.1 crore for a period of 20 years which could cost him Rs.6,500 per annum (approx.). In case of his untimely death, the sum assured would be paid by the insurance company to cover the children’s education-related expenses.

For his life risk until retirement, he can choose another Rs.50 lakh to Rs.1 crore as sum assured under term assurance for 25 years which could cost him Rs.5,500 to Rs.6,500 per annum (approx.) that would take care of all other financial risks.

In case no untoward incident (such as his untimely death) happens, at the end of 17 years during the repayment of his home loan the premium payment will stop. Similarly, 20 years from today the premium payment for education too stops; only the overall risk-related premium payment would continue till he is 60 years old.

This is by far the best method of addressing financial risks. People make the mistake of buying traditional plans such as endowment, money back and whole-life policies which are highly expensive and impractical to cover the entire financial risks across different stages and requirements of life.

Health insurance

Rangan should also buy health insurance. Though he argues that his company has medically covered him and he will not need another insurance cover, this has no rationale because if he quits his job, his company-covered insurance would become invalid. Even if he works till his retirement, post-retirement his insurance cover would cease to exist. Hence, he should buy a health cover worth at least Rs.15 lakh which could cost him approx. Rs.15,000 per annum.

Source : http://goo.gl/xXVEqh

ATM :: Beware of these hidden charges on your home loan

HARSH ROONGTA | Tue, 29 Mar 2016-09:22am | dna

Shrinking interest rate margins have made several lenders to insert hidden charges to increase their margins by stealth.

The home loan industry has come a long way from the time when the only charges that you had to watch out for were the processing charges taken under various heads and pre-payment charges. Regulation has ensured that there are no pre-payment charges and competition has ensured that there is a greater degree of transparency around the processing fee, legal fee, valuation fee or technical charges. Competition has also ensured that there is hardly any difference in the interest rates charged by various home loan lenders. Unfortunately, the shrinking interest rate margins have made several lenders to insert hidden charges to increase this margin by stealth.

Here is a list of these charges:

Charge interest on the loan which is disbursed late – This is a common practice. The lender prepares a cheque, but it is not to be handed over till certain documents are received from the borrower and/or the seller. These documents normally may take a few days to a few weeks, and meanwhile, the interest meter is ticking for the borrower. This is not as small as it looks. On a loan of Rs 1 crore, the interest @9.50% works out to Rs 2,600 daily.

The cost of a 10-day delay in handing over the cheque (which is pretty common) means an additional cost of Rs 26,000 or 0.26% of the loan amount. You should negotiate with the lender that you will only pay interest from the day the cheque is actually handed over to the seller and not from the date mentioned on the cheque.

Advancing the EMI payment date – The EMI amount is calculated assuming that the payment will be made at the end of 30 days from the date of disbursement. If this EMI is paid earlier than 30 days, the cost becomes much higher than the stated cost. An example will illustrate this. If the disbursement is made on February 15, 2016, and the EMI is payable on the first of every month then typically you should pay interest equivalent to 15 days’ interest (from February 15, 2016, to March 1, 2016) and the EMI should start from April 1, 2016, only. However, most lenders will start off the EMI from March 1, 201, and still charge you for a full month’s interest. Again, the difference is not as small as it sounds. 15 days’ extra interest for a Rs 1 crore loan @9.50% works out to Rs 39,000 or 0.39% of the loan amount. Again, you can negotiate with the lender to make sure that this additional hidden interest is not charged to you. Unlike the first point which is easily understood, this point is technical and the lender can run loops through the borrower while explaining how the EMI is calculated.

Forcing borrowers to buy expensive insurance products – Lenders have tied up with life and general insurance companies to provide life, disability and property insurance to borrowers and they force you to take these policies. The lenders earn fat commissions on the sale of these insurance policies and even though officially not permitted, they force the borrowers to sign up for these policies. It is a good practise to have such type of insurance policies when you take a loan, but the problem is that the policies being hawked by the lenders are hugely overpriced, reflecting the captive base of borrowers and the fat commissions for the lender inbuilt in such policies. To avoid having to pay for these overpriced policies, you can negotiate with the lender that you will buy these policies on your own. In all probability, you will get the exact same policy from the same insurance provider as what the lender is pushing at a fraction of the cost that the lender will charge.

Forcing borrowers to take a credit card or some other add-on products – In most cases this is offered for free while not stating that it is free only for the first year and would have an annual fee every year after that. You can easily negotiate your way out of this one.

Whilst these are the “extra” charges that lenders take from borrowers, there is a charge that they are unfairly accused of taking. For example, in Maharashtra, you have to pay a stamp duty of 0.20% of the loan amount on the document creating the security in favour of the lender. It is obvious that this charge will be recovered from the borrower (it is also mentioned in the loan agreement as recoverable from the borrower), but I have heard many borrowers complain that this is a hidden charge sprung upon them. This document is in favour of the borrower as it is conclusive proof that documents have been handed over to the lender. This is extremely useful when the loan period ends because there have been increasing the number of cases where the lenders have misplaced the title deeds and claim that these were never deposited with them in the first place. A stamped and registered document will prevent the lender from making any such claims.

In this new age, the lenders depend on the borrowers lack of attention to slip in the extra charges. It makes eminent sense for the borrowers to take the help of professionals to help them navigate through this process. The fee payable to such professionals will be more than made up by the savings in these “extra” charges.

Source : http://goo.gl/ImwYEb

ATM :: Stealing from your wallet? 7 entrapments from banks that you should be aware of

By Sangita Mehta, ET Bureau | 13 May, 2015, 10.48AM IST | Economic Times

A bank’s facilities typically come loaded. For the unsuspecting customer, it could just be a question of filling out a fixed deposit form or being granted a home loan. But there are some entrapments the bank will slip in that you need to be aware of, says Sangita Mehta.

HOME LOAN: Double Trouble

Watch out: When you apply for a home loan, the bank will sell you property insurance — which covers damage to property — and mortgage protection term insurance, which covers the loan in the event of the borrower’s death

What you should know: The housing society may already have property insurance. You don’t have to opt for an insurer the bank has a tie-up with. Ensure the premium is not clubbed with the loan, in which case, you will have to pay interest

CREDIT CARD: Take it or Leave it

Watch out: Banks often sell credit cards with the promise that for the first year, they will not charge any fee and the customer can discontinue it from the second year. However, at the end of the second year, the card company sends an innocuous mail stating they will renew the card for a fee unless the customer explicitly rejects it.

What you should know: The Reserve Bank of India has banned banks from giving such negative options. Customers should ideally use the credit card of a bank they do not have a savings bank with. In case of a dispute, banks often debit money from the borrower’s account

DEPOSITS: Auto Route

Watch out: When you’re opening a fixed deposit, watch out for ‘auto renewal’ in the fine print

What you should know: If you do not opt for auto renewal, the money is transferred to the savings account after maturity, where the bank offers about 4% interest as against 7-9% on FDs. You may forget to renew the deposit and the bank won’t remind you. When you tick that ‘auto renewal’ box, the bank cannot charge you a penalty on premature withdrawal of the deposit

ATM, CYBER FRAUD: Cry ‘Thief’

Watch out: If you find a fraudulent transaction in your account, immediately notify the bank

What you should know: If you are the unfortunate victim of an ATM or e-transaction fraud, watch out: the bank is liable to prove its innocence. If the bank is not notified, the maximum loss to you is `10,000 Postnotifi cation, the customer is not liable to bear any cost

LOCKER FACILITY: Keep your Freedom

Watch out: Banks put a price tag on a ‘scarce’ commodity like the bank locker

What you should know: Your bank may ask you to invest in fi xed deposits or mutual funds or even third party insurance, with the bank locker, even though they are not allowed to to do so by the RBI. You anyway need to pay an annual rental

PERSONAL LOANS: Don’t Rush to Pre-pay

Watch out: Banks have stiff conditions on prepayment of personal loans

What you should know: The RBI has mandated banks to not charge a penalty for pre-payment of a home loan if the interest is on a floating rate. But the rule does not apply for other personal loans. Some banks charge as much as 5-10% on pre-payment of loans. Some banks don’t even permit you to repay the loan for the fi rst six months or one year

PROCESSING FEES: No Free Lunches

Watch out for: For every home loan, auto loan and personal loan, banks charge a processing fee, which can be steep

What you should know: This fee is mostly at the discretion of the bank and can be as high as 1 percentage point, which itself will infl ate your outgo. If any bank says they have a lower rate, ensure the processing fee is also low.

Source : http://goo.gl/r0S6eK

ATM :: SBI MaxGain Home Loan Review – With FAQ’s

By Ashal Jauhari | 14th April 2013 | AsanIdeasforWealth.com

In this article we are going to share SBI Maxgain Home Loan review with you. Now a days many home loan borrowers are opting a particular type of home loan from State Bank of India which is called Max Gain because it has many advantages compared to other kind of home loan scheme’s. In this SBI Max Gain home loan, an Overdraft (OD) account is assigned to the customer’s home loan & any amount parked by customer is treated as loan repayment for the purpose of interest calculation, for the days, the amount stays there in that OD account. As on date following banks are offering similar types of home loan to their customers SBI, IDBI, CITI, HSBC & Standard Chartered. Punjab National Bank can also be added in this list but it’s offering a combo of normal loan + Overdraft. In this article, we are going to discuss only SBI Max Gain as in OD linked home loan, the maximum business is with SBI & the most discussed topic on Jagoinvestor Forum is also related to SBI Max Gain Scheme

What is an Overdraft account?

Before we discuss Max Gain, first understand, what is an Over Draft Account? All of us are well aware of functioning of an ordinary saving bank (SB) account. Here account operates between zero to positive & positive to zero. As we deposit our money, it’s used by bank & we get interest on our money from bank. In case of an OD account, bank first ask for a security & then assign a credit limit on the basis of the market value of that security. This security may be Fixed Deposits, Insurance Policies, National Saving Certificates, Shares, Mutual Fund units, house/commercial property etc. Now when we are using this assigned credit limit, the amount is going from zero to negative zone & when we are repaying, it’s coming from negative to zero. As we are using bank’s money in this case, the interest ‘ll be paid by us to bank. That’s how an OD account works.

So what is the correlation between Max Gain home loan & Over Draft account?

For Max Gain borrowers, State bank of India opens an Over Draft account where the Credit limit as discussed above is equal to the loan value assigned to the borrower. Here underlying security is the home you have purchased or constructed from that loan amount. Now as & when you are parking any surplus amount into this OD account, the parked amount is treated as payment towards loan (effectively you are bringing down your loan liability from negative towards zero position) and thus the interest ‘ll be charged only on the difference amount i.e. total loan amount – parked surplus amount.

What is the primary benefit of SBI Max Gain Scheme?

Well the primary benefit of MG is to keep your liquidity intact & still bringing down your interest outgo. To understand it better, please imagine a situation you are running a home loan of 30L Rs. & now you do have 2L Rs. with you to prepay. In normal home loan, your 2L Rs. ‘ll be accepted by bank & adjusted towards home loan & your amount is gone forever so no liquidity for you of that 2L Rs. amount. On the other hand, if you are MG customer, simply park those 2L Rs. in your MG account & your interest outgo ‘ll be lower from that month itself till those 2L Rs. or a part of it is there as surplus in MG account.

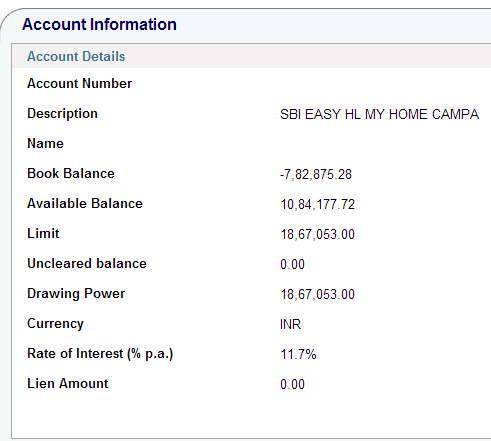

What is Drawing Power ?

Drawing Power is nothing but your as on date actual outstanding loan amount. Before final disbursal or start of loan repayment, it’s your sanctioned loan amount. Once your EMI starts, it’s your as on date actual outstanding loan amount. Please check Image below, Drawing Power here is 1867053 Rs. as on date.

What is Available balance?

Before final disbursal, it’s the sum of undisbursed amount + parked surplus & post final disbursal, it’s your parked surplus amount which is available to withdraw. Please check Image below, Available Balance here is 1084177.72 Rs. as on date.

What is book balance?

It’s the adjusted loan amount arrived after deducting the Available Balance amount from Drawing Power. In your account statements it’s shown with a negative sign. Please check Image below, Book Balance here is – 782875.28 Rs. as on date.

Is there any extra interest for Max Gain?

No, the interest for home loan is same in SBI be it for normal home loan or for Max Gain.

I’m an existing SBI home loan customer. Can I convert my old term loan to Max Gain?

Yes, you can. Please contact your loan serving branch or RACPC for the required paperwork to be done. This may be an outdated info so please do check with your loan serving branch for current day rules on conversion.

I have taken the Max Gain for an Under Construction Property. Can I park surplus amount to save on interest outgo?

The answer is yes & no both. Yes you can park your surplus during under construction phase but do remember SBI is disbursing partially at this juncture & in case due to any emergency you want to liquidate your surplus, SBI ‘l not allow the same. so park only that much surplus, you feel you ‘ll not need even in an extreme emergency.

If I’m parking some money on monthly basis or in lump sum, will my loan term come down or EMI go down?

No. Neither your EMI ‘ll come down nor your loan term. The only saving is in terms of interest outgo. To understand it better, Let’s assume a test case of loan amount 30L Rs. @ 10% Rate of Interest for 20Y term. The normal EMI for these nos. ‘ll be 28951 Rs. The break up of your EMI for first month ‘ll be 25000 Rs. interest & 3951 Rs. for principal repayment.

Now if you do have 2L Rs. surplus in the very first month & prepay the same as below –

Case – 1 Normal home loan

Your 2L Rs. is gone & outstanding loan amount ‘ll come to 2796049 & interest outgo ‘ll still be 25000 Rs. but the no. of months ‘ll come down from original 240 to 198 months.

Case – 2 Max Gain home loan

Your 2L Rs. are parked in that OD account & the interest for the very first month ‘ll be calculated on 28L Rs. & thus it ‘ll be 23334 & thus there‘ll be an interest saving of 1667 Rs. which‘ll remain available in your OD account as surplus along with your parked surplus 2L Rs. so for next month, the parked surplus amount ‘ll be 201667 Rs.

Please do note in case 2 above, Your loan term is still 240 months but the saving of interest ‘ll keep on increasing on mly basis from the parked surplus & of course the liquidity of those 2L Rs. is there.

How can I calculate my saving in Max Gain?

To know your actual saving, first of all please demand a loan amortization schedule from your loan serving branch & now for each month compare the scheduled interest outgo as per your loan amount. schedule & the actual interest outgo.

What should I do to maximize the savings in Max Gain?

If you are paying your EMIs from SBI’s SB account, you can maximize your benefits. How? here it goes. Say 15th is the EMi date on which EMi amount is debited from your SB acct. Now in a normal home loan, people ‘ll keep at least 2-3 months’ EMI amount as buffer in SB account. but in case of Max Gain, you do not need to keep buffer in SB account. Keep this buffer amount also in your MG account along with your routine surplus amount. now use the power of net-banking of SBI for your own good & create a schedule transaction of your EMI amount 28951 Rs. (in the above example) to be transferred on 13th of every month from MG account to SB account. At a time you can schedule for next 12 months by using standard instruction. So it’s technology that’s helping you.

I can transfer to MG account from my existing net-banking enabled SB account but reverse is not happening. why?

The answer lies in the fact that Net-banking transaction rights on your MG account is not enabled yet by your loan serving branch. if final disbursal is done, you can apply for transaction rights. if only partial disbursement has been done, sorry, you can’t apply for transaction rights till final disbursal.

Is it mandatory to purchase property insurance & life insurance along with Max Gain?

Having property insurance as well as sufficient life insurance is compulsory but purchasing the same from SBI’s sister cos. like SBI General ins. & SBI Life Ins. is not at all mandatory. if you feel that policies are being cross sold to you to exploit your position (home loan seeker), please contact the AGM of your local RACPC where your loan application is under processing.

Is SBI charging higher processing fee for Max Gain?

No, as on date there is no differentiation in fee for term loan & Max Gain but SBi reserves the rights to charge different fee.

Can I claim section 80C principal repayment benefit for the surplus amount parked in Max Gain?

The answer is NO. Only the regular principal repaid by you from your EMI as part of your loan amortization schedule is available for tax benefit under section 80C. the parked surplus amount is liquid money & you can withdraw it any time, hence it’s not considered as actual repayment of loan & thus not eligible for tax benefit.

Can I avail cheque book & ATM card for my Max Gain account?

Yes, as & when you‘ll demand these, SBI ‘ll offer you the same. In case you are already holding an SBI SB acct. linked ATM card, you have the option to link your MG acct. also with this existing ATM card.

Can I enroll my MF SIPs in Max Gain?

Yes but do note, there should be a surplus balance i.e. available balance on the date of SIP, else your ECS or SI mandate ‘ll bounce.

Can i pay for my utility bills, credit card payments, online shopping from Max Gain?

Yes, you can do all this & more. In fact it’s in your best interest that you treat your MG account as your primary money parking account & route all your transactions through it so that money is lying there for maximum possible time & thus helping you to bring down your interest outgo.

I used my MG account ATM card to withdraw cash from other bank’s ATM & I was charged the money very first time in the month. Why?

The reason is, as per RBI’s circular 5 transactions on other banks’ ATM are free only for SB account & in this case, you forget the point that your MG account is not SB account. it’s an overdraft account.

For an imaginary situation, my loan amount is 30L Rs. & parked surplus amount is also 30L Rs. Does it mean, my loan is closed & I can claim my property papers from SBI?

No, your loan is not closed. Only interest outgo ‘ll become zero & EMi ‘ll remain continue as it is. Yes the interest part of your EMI ‘ll keep on accumulating in your MG account. If you want to close your loan at this point, you w’d have to inform SBI in written & now SBI ‘ll adjust your parked surplus amount towards the outstanding loan amount. you ‘ll lose the liquidity of your money but loan ‘ll be over & now you can get your property papers back.

How can I transfer my loan from other banks to SBI Max Gain?

For loan transfer, first of all contact your existing lender & ask for following things.

1. Loan Account statement from day one.

2. List of Documents, which were submitted by you at the time of availing original loan. In day to day language of bankers, it’s called LOD.

3. As on date outstanding loan balance with applicable interest, penalty & any other fee to close the loan.

Now contact, the nearest SBI Branch (if you do have an existing SB account with SBI, it’s advisable to contact there for ease of operation). Inform in that branch that you want to transfer your loan from existing bank to SBI Max Gain. fill the application form, submit the necessary papers & SBI’s RACPC ‘ll do the back ground job.

Once SBI is ready to accept the transfer, it ‘ll issue you a sanction letter of the loan amount & ‘ll ask you to go for loan related agreement documentation work with SBI. If you are not having property insurance, SBI may ask to purchase one. Same ‘ll be the case for your life insurance. Once legal documentation is over, the cheque of the loan balance ‘ll be issued directly into the name of the bank in question. After the amount is credited to your existing bank, within next 20-30 days, you ‘ll get the original documents submitted by you, from the existing bank. Now you w’d have to submit these documents to SBI. In some states like Gujarat, Maharashtra, Karnataka, SBI may ask to go for registration of mortgage deed on your property in the office where your property was originally registered in your name.

|

SBI Max Gain |

Normal Home Loan |

|

Liquidity of your part prepayments is there |

No Liquidity. Money is gone for ever, once you prepay. |

|

A bit complex to understand |

Easy to understand |

|

For people who can generate regular surplus amounts |

For people who can only manage regular EMIs |

Source : http://goo.gl/5q11YV

ATM :: 11 Aspects of your Home Loan that Can’t Be ignored!

Sukanya Kumar, Founder and Director, RetailLending.com | Mumbai | January 27, 2015 16:34 IST | IndiaInfoline.com

For most people, applying for a home loan can tedious and stressful period, and in the process, prospective borrowers may end of ignoring certain aspects of their mortgage in a rush to get the process completed. These aspects may end up being a cause of great anxiety in the future, and it is better to be aware and abreast at the outset of the process. Let’s take a closer look at things you just cannot ignore while applying for a mortgage!

How did you compute the Amortization Schedule?

Everyone, who has in-depth knowledge of mortgages, should be able to explain to you how the equated monthly installment (EMI) is calculated and the relevance of an amortization schedule. It is just not another excel spreadsheet which is shared with all new trainees so that they can forward the same to you to win your business over! This is important for you, as you must understand the ratio in which the principal & interest is spread over the sheet. This will help you decide your interest paid every financial year & save tax. Not saving correctly is a loss and constitutes as a ‘charge’.

Is this loan a Daily Reducing or Monthly Reducing Balance?

Many years ago, when there were only a couple of lenders in mortgage industry, annual reducing rate was the only choice. This meant whatever principal you pay throughout the entire year will be deducted from your principal after completing one year! This meant paying interest on the paid loan amount too! The same is the difference between daily & monthly reducing balance. Are you getting the principal repaid amount adjusted the very next day of your making the payment, or after your next monthly payment date? Paying interest for already paid loan amount is terrible. Don’t you think you should find that out before you choose your lender to save this cost? You sure do.

How does part pre-closure happen in your bank? If I prepay 500 Grand’s on 22nd Jan, when do you reduce my outstanding principal?

Many a times you will find that while closing down your loan, you are forced to pay interest till the next EMI date, or sometimes the closure amount claimed by the lender specified in their foreclosure letter is- “Same for the next 15 days”. Well, how can that be? The closure amount should be different for different dates as interests are calculated daily. Your closure amount cannot be same on 16th & 30th of the same month. Then what you are paying on 16th must be including the next 15 days’ interest. Isn’t it?

When does my EMI start if I draw down my loan on middle of a month?

This is a very interesting question, please do calculate and check how many days of interest are you paying before your actual EMI starts! For example, if you are drawing down your loan on 25th of January, ideally you will be asked to pay simple interest (Pre-EMI) for balance 6 days of the month and then your EMI should start. Question is when does your EMI start? If it starts in February, then how much of that EMI is principal and how much is interest? Some lenders will start EMI from March. So, how is that math done? You need complete transparency on this one!

How do you calculate Pre-EMI for an under-construction property? When does the lender issue the pay-order & when does your developer receive it? If delayed, who pays for the delay in delivering it?

Please note that it is you who always ‘pay’. It is neither the lender nor the developer in any circumstance. So, it should be planned enough, for you not to lose any of it. The Pre-EMI (simple interest) is calculated on the number of days you remain drawn down, before you actually start the EMI. On the other hand, if the amount is not delivered in time to the builder, you may face consequences of delay-penalty, losing builder-subvention interest or something more. So, the gap between the pay-order being prepared by your lender (when your clock starts) to the delivery to developer needs to be monitored by you or your adviser, so that you do not pay interest just like that which is an unnecessary ‘cost’ to you!

What are the charges for switching loan from Fixed to Floating option or vice-versa? Or, switching between different mortgage products?

In India, the loan rates are extremely volatile. We have experienced a range between 7 – 13.50% within 6 years on a home loan! One might laugh saying ‘why didn’t you do something about it on your own mortgage!!’, the answer is- “This is exactly what has given me the life’s bitter experience to be able to advise today.” 🙂 I was asked to pay a 2% switch fee to be able to shift between products. Floating to Fixed, or simply Floating Standard to Floating Overdraft! Please do not make the mistake I made, of not asking your lender’s rep or adviser on this ‘hidden’ fact.

Is there any Documentation Charge in any stage?

Often lenders ask you to do fresh ECS or sign new loan kit while altering rate/margin/product/product-variant, out of the turn. This might involve a fee. Not knowing about it in advance will constitute it to be termed as ‘hidden’. This is generally a very nominal cost, but in my opinion, lenders can easily do away with it.

Does your company follow same rate norms for new & old borrowers? What is the past two-year trend on the differential rate, if any, and why is the difference?

Lenders reduce the offer rate in the market by two ways-(a) By reduction in their base rate or prime lending rate (PLR) and (b) by fluctuating the margin for the new borrowers. Wherein the first one is always welcome as it offers transparency to the existing borrowers, you may sometimes just get a shock to find that the new borrowers from the same lender is getting a better rate than yours. Studying the history of the lender will help you understand the trend with the particular one. The lender who is prompt in reducing base/PLR should be your choice. Servicing loan at a higher rate for even one month is going to matter and obviously it is an outflow from your pocket, hence a ‘hidden charge’.

What are the associated fees like legal, valuation, documentation, administrative, mortgage origination, intimation of registration etc.?

Lenders generally speak about the fees levied directly by them like processing fee. You will find advertisements claiming ‘nil processing fee’ during festive seasons, year-end closure for the lenders or may be while wanting steep rise in portfolio etc. Please understand that processing fee isn’t the only fee you pay for acquiring your Mortgage. Seek complete transparency in all ‘charges’ even if the lending institution does not levy it directly. So, a lawyer fee, technical evaluation fee, Govt. levy, other charges & expenses should be clearly explained to you before you land up thinking ‘I don’t mind paying, but why was I not told?”

Does your chosen lender give Provisional Tax Certificate in advance?

Not receiving provisional tax certificate means you will have to allow your employer to keep deducting tax every month from your pay & when you receive it from your lender at the fag end of the financial year, submission date to your office may be over. All you can do now is to wait for tax refund after filing your ITR. To avoid is craziness, your lender should give you the provisional projected interest and principal outflow statement in advance, which you should submit, in your office immediately to avoid getting deduction on your pay slip every month. The final tax certificate, if has any differential amount, will only have to be paid by you, without having to wait for any refund. Not receiving it upfront will be a ‘costly’ affair!

Cost of stress, having to follow up, coordinating between lender, builder/seller and you, worrying day-in-and-out also costs!

Your business is to get a stress-free mortgage and ours is to make sure you get that. If you are the one is picking up the phone every-time to call the lender or your adviser to know what is happening on your loan application, and not being responded to, I can imagine what is happening on your work-life and how stressed you are even at home! Please do not ignore the ‘price’ you pay for not getting any service. Choose a lender who has good market reputation of customer-orientation and choose the adviser and service-provider that has knowledge, experience & an infrastructure to support you every time you need service.

There are plenty individual loan agents floating in the market who sell all types of loans, credit cards, insurance, holiday package……all at a time! Think before you engage them for a promise of a good ‘deal’. You may not find him after your application gets logged in his code in the bank or he may even not have a direct agreement with the bank at all and working with another person of an agency! The agency may not even know this guy and you can’t even report him! The signs will be: he will be desperate for your business, will offer you the moon, will always assure you that he will do ‘whatever you want, sir’.

The stress of not having a good mortgage-lender and adviser can be as bad as not having a supporting partner. Ultimately, you are getting into a 15-20 years of commitment! It should be from both sides. Isn’t it?

Source : http://goo.gl/FeCIJa

ATM :: Don’t only insure your life, ensure your home loan is paid!

By: CreditVidya | December 26, 2014 9:24 pm | Financial Express

Introduction:

It is one thing to get a home loan and a different ball game to repay the loan, the tenure of which may run over a decade. With such long period of commitments, it is bound to put a person in an insecure mode as anything can happen to the loan holder. To ease yourself of the worries, it is important to take an insurance to protect your life to cover this loan burden in case of any casualty. That way your family inherits your home and not your loan burden.

Story:

Buying a house is a big deal today simply because of the high expenses one has to incur while buying. It can be overwhelming in many cases, because you will have to literally pull out all your savings to get it. These days a lot of funding burden has been reduced thanks to the home loans. The lenders also offer you an insurance policy to cover your home loan in case something happens to your life. You have the choice to choose any insurance policy from any company and can say no the bundled offer which in most cases will be from a group company and might come to you at a higher premium.

When UR Simha, a Pune-based techie bought his house, he took a loan from HDFC. He also bought an insurance policy that was offered at the time of signing the loan documents. What he did not realize was that the insurance tenure was for five years and where as his loan was for 20 years.

“I did not even think of securing my life until they offered this insurance. It came at the last minute, so I did not think twice. I bought it anyways. Later, I got to know the details and features of competing insurance products were much better. I wish I had done some study before I paid the premium,” he said.

So what are the terms and conditions you should look for in such policies? Following are a list of features available:

Cover: Ensure that the term covers the entire loan value. Some of them cover applicant and the co-applicant. Choose what suits you the best.

Tenure: It always makes sense to buy a term insurance that covers entire life span of the loan

Premium: Enquire with all the insurance providers. Do not fall for the marketing gimmick of your lender who is trying to cross-sell a product.

You might find a competitor offering you similar terms for lesser amount.

Unemployment benefits: Some of these insurance policies also offer certain benefits in case of a job loss. They pay your EMI if you have been retrenched in your company. But please note that this is for a few months only and you have to provide a proof of being asked to leave along with the reason. So, if you have a job, which is prone to downsizing, it is a good idea to consider this kind of a policy.

Critical care benefits: Some policies also cover your home loan if you end up being in an accident and are bed ridden for life. In such cases the loan outstanding will be waived off. The premium might be a little higher but the benefits are proportional.

Covering the house: Most policies also cover your house and some of them give you additional benefit of covering the contents in your house. But the cover is subject to certain terms and conditions. So make sure you know what you are paying for.

Source : http://goo.gl/OKzYch

POW :: 5 things to know about Home Loan Protection Plan

Dec 9, 2013, 08.00AM IST| Economic Times

Here are five things to know about Home loan protection plan (HLPP):

1. HLPP is an insurance plan which provides a lump sum benefit on the death of the insured. This can be used to repay the outstanding home loan.

2. The cover in an HLPP is usually the same as the loan taken. The premium for HLPP can be paid as a single premium in advance or on an annual basis.

3. Insurance companies also offer an option where the annual premium is clubbed with the Home loan EMI paid by the borrower.

4. Since the value of the outstanding loan reduces over time, the premium for HLPP is lower than that of a life cover for a similar amount.

5. Like a term plan, HLPP does not offer any maturity or survival benefits.

Source: http://goo.gl/VP83u9

ATM :: Hedge your house

The Hindu|Balaji Rao|June 28, 2013

Insuring our home loan is not something we do instinctively, but it’s a smart way to protect our investment

It does not seem like an important or urgent decision, so you either put it off or don’t do it at all. But this is one expense that might well be an investment — home loan insurance.

Since the tenure of home loans is longest compared to other kinds of loans, we could all be vulnerable to mishap in some form, such as illness or death of one of the chief earning members of the household while one is in the middle of repaying the loan. That’s why it makes prudent sense to cover the risk by insuring it.

There are two ways of insuring the loan, and should be ideally done at the time of availing the loan itself. The first is to buy a term assurance policy for the specific tenure of the loan, and pay the premiums through the tenure. The second is to opt for a single premium plan.

For example, if you are 30 years old, and have taken a home loan of Rs. 30 lakh for a period of 20 years, then you should take a pure risk cover for a sum assured of Rs. 30 lakh. The annual premium will be in the range of Rs.6,000 per annum, payable through the tenure of the policy (Rs. 6,000 x 20 years). In case of untimely death of the insured person, the insurance company will reimburse the sum assured to the legal successor or nominee, and it can be used to clear the loan outstanding as on that year.

The second option, which comes highly recommended, is to avail a Home Loan Protection Plan. Offered by most insurance companies, it ensures that the outstanding loan, up to the amount insured, is repaid in the unfortunate event of the death of the borrower. Unlike the previous plan where the premiums are paid throughout the policy term, here it is a ‘single premium decreasing term assurance plan’ where, as the loan outstanding reduces, the sum assured also reduces in the same proportion. This means the insured person only pays premiums for the amount outstanding and does not keep paying premiums for the entire amount.

The one-time premium amount will be based on the age of the borrower, loan amount and loan tenure. For the above quoted example, the premium could be around Rs. 80,000.

Home Loan Protection Plans are often sold along with the housing loan since most HFIs and banks either have in-house insurance agencies or tie-ups with some. Some banks also add the premium charge to the loan itself.

A point to be noted is that under the single premium method, if the borrower dies during the course of repayment, after adjusting the outstanding loan amount, any balance is paid to the nominee or legal successor. Thus, if the loan tenure is 20 years and the outstanding loan amount is Rs. 20 lakh, against an originally borrowed amount of Rs. 30 lakh, then at the end of five years if the borrower dies, the bank will adjust the loan outstanding and the balance of Rs. 10 lakh will be paid to the legal successor.

It is easy to conclude that if death does not occur during the loan repayment tenure, the premiums paid are a waste of money. But the point of insurance is that it is a hedge against risk. Over a period of 20 years, anything can happen and the premium should thus be seen more as an investment. You can avail tax benefits too under Sec. 80C on the premiums paid.

Source : http://goo.gl/j7PSh

ATM :: There’s more to home loan than just interest rates!

By Sanjeev Sinha, ECONOMICTIMES.COM | 17 May, 2013, 02.58PM IST9 comments |Post a Comment

Before opting for a loan, it is advisable to assess impact of taking a loan & subsequent EMI payments on the monthly cash out flows.

Buying a home is an important personal finance decision for every individual, particularly in view of the fact that a home is usually the biggest investment in one’s lifetime. And like anywhere else in the world, home loan or mortgage products have only made it easier for average salaried Indians to own a home they can call their own. One should, however, not forget the long-term liability that needs to be serviced and it would only help to keep some of the following things in mind when taking a home loan:

1. Impact of loan on your personal finance

Before opting for a home loan, it is always advisable to assess the impact of taking a loan and the subsequent EMI payments on the monthly cash out flows. It is a prescribed personal finance practice to get a new monthly budget in place which accommodates the new cash out flow in the form of EMI payments.

“The impact should be analyzed on the monthly available surplus and subsequent savings being done towards achieving other goals. This helps in determining the comfortable EMI payments one can make and respective loan amount one can opt for,” says Nitin B Vyakaranam, founder & CEO of financial planning portal Artha Yantra.

In other words, what you can afford should be determined by your ability to service the re-payments of the liability you undertake with a home loan. This would be governed by the loan amount and the interest rate applicable on your home loan. “You also need to remember that taking a loan with a view of selling the house a few years down the line at a higher price to help you settle your liability may not always work, especially if the property prices start moving downwards or even if they remain static – as we have seen over the last couple of years the world over,” observes Anil Sahgal, director, MAGI Research and Consultants, and co-founder of personal finance consulting portal ‘i-save’.

Therefore, it makes sense to access your affordability and the loan’s impact on your personal finance before opting for a home loan.

2. Know your maximum loan eligibility

As per the current market norms, banks can lend up to 60 times the monthly net salary of an individual. However, while assessing the income criteria, they do not consider some of the salary slip heads for calculating the net monthly income. They only consider the income heads which can be used to repay your loan.

“For example, your LTA and medical allowances are deducted from the monthly net salary you receive. You are expected to spend the amount received under these heads for the specific activities they are being provided for. This is one of the reasons why we generally see a difference in the eligibility amount quoted in the website and actual amount realized once the application is processed,” informs Vyakaranam.

3. Check your CIBIL score

The home loan eligibility depends on credit worthiness of the individual. Credit Information Bureau India Ltd (CIBIL) provides a credit score on a scale of 300 to 900 based on your previous credit card usage, how you maintained your bank accounts, any check bounces, existing loans, uninsured existing loans, loan repayments, how many times you have applied for loan or a credit card. Individuals with a CIBIL score greater than 700 are more likely to get a home loan. All the home loan lenders approach CIBIL for this score whenever you apply for a credit card or any sort of loan.

“Paying the processing fee to know the maximum limit at more than 3 or 4 banks is one of the common mistakes committed by many people. The more times you apply for loan, CIBIL considers it as being credit hungry. So the chances of getting a loan are minimized. CIBIL rating, net salary excluding some variable heads and existing loans and EMIs being paid towards existing loans are the vital components which decide the repayment capacity of the applicant,” says Vyakaranam.

4. Co-application

What you can afford will also be reviewed by the bank that is providing you the loan. This would depend on your past and current financial position and ability to service the loan in the future i.e. ability to pay back the loan with applicable interest.

“In case you want a loan amount higher than what you are being offered as an individual, you may want to have your spouse or parents as co-applicants. This helps you increase the overall limit that the bank can offer since there is more than one person sharing the repayment of loan and the combined limit will obviously be higher. Needless to say, this can only work if the co-applicants have an independent source of income,” says Sahgal.

Having co-applicants can also make sense from a taxation perspective with each applicant being able to avail the tax benefit available on interest payment of an EMI.

5. Duration

Once again, keeping in mind how much you can afford to pay each month, try and keep the duration of the loan as low as possible. With a lower duration of loan, the EMI may be higher but what you would pay as interest over the term of your loan would be substantially lower. If you can’t afford the higher EMI and have to necessarily take a higher duration loan, it would help to try and manage your savings in a way that help you pre-pay the loan with intermediate payments in the initial years itself so as to reduce your overall interest burden.

6. Type of interest rate

The type of interest rate you choose has an impact on the monthly EMIs you pay. It is important that you know the difference between fixed rate home loan and floating rate home loan. For instance, if you opt for fixed rate home loan, the EMIs don’t vary over the loan tenure. So it is beneficial when the interest rates are expected to rise in the near future. In case of floating rate home loan, interest rate is determined based on the prevailing base rates, plus a floating rate. The EMIs vary based on the movement of base rates. It is beneficial when interest rates are expected to fall in near future.

But the choice on this one is not really easy. Fixed interest rate products are usually 1-3% higher than floating interest rate products, but bring a certain level of certainty to your financial planning since you are more or less certain of your monthly outgo. On the other hand, floating interest rate products, though cheaper, are linked to a base rate or benchmark rate and can go up or down with a change in the base rate.

“It would, therefore, make sense to go in for a fixed rate product only if you think the interest rates in the economy are bound to go up over the next few years. Even in this case, if the spread between the fixed and floating rates is fairly high, floating rate options continue to be better. For e.g. if the rate on fixed and floating rate products is 12.5% and 10%, respectively, then as long as the increase in base rates is lower than 2.5%, floating rate products continue to be cheaper,” says Sahgal.

You may also want to check the terms and conditions associated with a fixed rate product. At times, the fixed rate is applicable only for a limited number of years, which in any case will defeat any assumption of certainty that you may want to build into your financial planning.

You should also remember that different banks offer different interest rates on home loans. Therefore, you must negotiate with them to get the best possible rate.

7. Pre-payment and foreclosure charges

One of the important features that you should consider in your home loan product is the availability of pre-payment facility. While some banks may not allow you to prepay your loans, others could be providing you the facility to prepay a certain percentage of your principal amount every year with or without a penalty charge.

“It would be worth your while to compare this feature across the product options you are evaluating since this flexibility can help you reduce your interest burden if you can manage to close your loan earlier,” says Sahgal.

8. Read the documents carefully before you sign

Don’t let the bunch of home loan documents bog you down and just sign on the dotted lines. Check the documents to ensure that the terms are same as what you negotiated and agreed upon. Read the documents carefully and know the different charges applicable. Importantly, know the processing fee, late payment fee and any charges that are applicable for pre paying the loan.

9. Take cover

Given the long-term nature of the liability, it also makes sense to protect yourself and your family from any unforeseen circumstances. In this case you can consider a life insurance plan.

“A life insurance plan that covers the re-payment of loan in the event of an unfortunate death of the borrower can at least help the family retain their home,” says Anil Sahgal.

10. Loan transfers

Having taken a loan, you may at some stage be tempted to transfer your loan to another bank or lending institution which is offering you a lower interest rate than you currently have. While taking this decision do make sure that you factor in any foreclosure costs associated with your existing loans (charges linked with an early closure of your loan). The bank you are transferring your loan to may also be charging you a processing fees. Do take these costs into account and ensure that the savings you make on lower interest rate are higher than the costs associated with the loan transfer.

11. Implications of delayed payments

Delayed or missed payments can impact you not only financially but can also affect your credit history. On the one hand, you may have to pay a penalty or fees associated with delayed or missed payments, while on the other your credit history will reflect these missed or delayed payments.

You should, therefore, always try to clear your EMIs in time because once you are declared a defaulter or your credit history turns bad, then it will become very difficult for you to take a home loan again from another bank or housing finance company. It will also become very difficult for you to transfer your loan to another bank or lending institution which is offering you a lower interest rate. Not only this, you also won’t be able to take even a personal loan in your entire life. Therefore, it is better to be safe than sorry.

Source: http://goo.gl/kKmaz

ATM :: Insuring your home, valuables may be as important as housing loan cover

By Preeti Kulkarni, ET Bureau | 24 Apr, 2013, 04.00AM IST |

Disasters, natural or man made, often serve as a rude reminder about buying insurance covers. Tremors in Delhi caused by the recent massive earthquake in Iran and the building collapse in Mumbra, near Mumbai, were two such incidents. Sure, the issue is a bit complex in the latter case, but it shouldn’t prevent you from thinking about the importance of buying a home insurance cover. Buying adequate insurance cover for your house, particularly if you have a home loan or keep valuable items at home, is the only solution to keep such unpredictable events from ruining your financial stability.

“The requirement of a home insurance was overlooked and understated in India. However, the scenario has changed over a period of time. Today, there are many convenient options available in the market that help one secure not only the property but also their belongings. The youth are also investing in homes, offices, etc, to ensure that all their assets are protected at the time of crisis,” says Mukesh Kumar, member of executive management and head, strategy planning, HR and Marketing, HDFC ERGO.

Now, most home loan borrowers are familiar with home loan insurance cover, thanks to their lenders and their insurance partners almost forcing them to buy a cover. However, home insurance is quite different. While home loan insurance offers to repay the loan if the policyholder dies before clearing the loan, home insurance comes into play if your property is damaged due to man-made or natural calamities. Such policies offer cover for both the structure as well as the contents in the house.

However, you need to specifically ask for the contents cover if you intend to insure your belongings in the house. You only need to fill up the proposal form listing all the items you want to cover while buying the policy. You will have to furnish first information report (FIR), fire brigade report or other details the insurer may ask for at the time of claim settlement. Coverage is extended against damage due to earthquake, fire, lightning, cyclone, bursting or overflowing of water tanks and so on.

Some policies also offer additional coverage against terror attacks, burglary and theft, while in some cases these are part of the base cover itself. Policyholders receive compensation for the replacement value of their property and contents inside the house. “So, the sum insured for the building should neither be the cost of acquisition nor the current market value of the house, but today’s construction cost because the market value of the building includes cost of land on which the house is built,” advises Sanjay Datta, chief, underwriting and claims, ICICI Lombard.

Similarly, for household appliances, gadgets, jewellery, furniture and other equipment, ascertain the cost of replacing them. In other words, market value of similar products, minus depreciation (depending on the items) will be the sum insured. “However, the claim amount payable would be the amount required to bring the damaged item to the same condition as it was prior to the damage, subject to the adequacy of the sum insured,” he explains.

Loss of jewellery and other valuables are covered, subject to the sub-limits or ceilings mentioned in the brochure. For instance, your policy could specify that the valuables cover will not exceed 25% of the total content sum insured or Rs 1 lakh, whichever is lower. Hospitalization expenses, too, are paid for if you are injured during the incident. Clearly, the utility value of such covers is quite high. In fact, most banks today advise home loan borrowers to buy this cover. Home loan agreements contain a standard clause that requires lenders to insure their house adequately against disasters. However, even otherwise, it is in your interest to get your home insured.

Remember, if your house is destroyed during such mishaps, you will be left with no shelter, but the burden of repaying the home loan will continue. “Even if it is not compulsory as per your banks to buy home insurance, it makes sense to opt for one. Else, the borrower will have to bear the losses in the event of damages caused by earthquakes or other natural disasters,” says VN Kulkarni, chief counsellor with the Bank of India-backed Abhay Credit Counselling.

However, if your bank is keen on selling its insurance partner’s policy to you, compare the features with other products in the market before giving your assent. There is very little variance in product features and premium rates, but choose your policy after a careful comparison. For the structure-only cover, the premium could be in the region of Rs 60 per lakh of sum insured. For example, if your sum insured (built up area in sq ft X cost of construction per sq ft) is Rs 20 lakh, you will have to pay an annual premium of Rs 1,200.

Lastly, do not forget to go through the list of exclusions or claims that won’t be entertained by the insurance company. For instance, your claim will not be admitted if the damage has been caused by natural wear and tear or depreciation. Similarly, you will not be paid if you have deliberately caused harm to your property. Other exclusions include loss due to war, invasion, civil wars, revolution and so on. More importantly, the policy will not come into play if any property or contents are illegally acquired or stored. Also, if you are operating your business from your house, you should not buy this policy, as it is meant only for residential properties. The policy wordings of such covers could also specify a deductible amount — you need to bear this expense out of your own pocket before the insurer chips in with the rest — for certain items.

Source: http://goo.gl/XNiGD