Tagged: Affordable Housing

NTH :: Affordable home-loans next threat to banks:Moody’s-ICRA report

PTI | Updated: Jan 9, 2018, 16:01 IST | Times of India

MUMBAI: Even as a lot of thrust is being given to the affordable housing segment, a report has flagged concerns about the growing delinquencies in this segment, which are expected to continue in 2018.

Competitive pressures and larger exposure to the self-employed are the prime reasons for the build-up of stress in the segment, a joint report by Moody’s and its domestic affiliate Icra said today.

“While asset quality is expected to remain stable in the traditional housing segment, delinquencies could further build up in the affordable segment in the calendar year of 2018,” Icra’s structured finances head Vibhor Mittal said.

In a note on asset backed securities (ABS) co-written with its parent Moody’s, the report said gross-nonperforming assets in the affordable housing segment have inched up to 1.8 per cent as of September 2017.

The average cum 90+ days past due level for affordable housing was nearly seven times the level observed for traditional housing loan pools, it said.

Going into the reasons for the higher stress in the low ticket size loans, Mittal said, “this would be driven by factors like intensifying competition– resulting in some easing in lending standards — and a higher share of lending to the self-employed segment.”

It can be noted that the Modi government is targeting to ensure that there is a house for all by 2022 and has provided a lot of incentives for the affordable housing segment, including making it as a priority sector lending for banks and huge interest subvention and direct cash subsidy.

However, housing loans continue to be seen as the best performing retail loan asset class in the country, demonstrating low and stable delinquencies over the years, in 2018, it said.

This is possible because of the underlying collateral, which is self-occupied residential property, absence of steep correction in property prices and moderate loan to value ratios, the report said.

Moody’s said the impact of demonetisation and the implementation of the goods and services tax (GST) will lead to higher delinquencies in ABS for loans against property (LAP) to small and medium enterprises.

“Introduction of a GST in July 2017 and demonetization have placed stress on the SME sector,” Icra’s assistant vice- president Dipanshu Rustagi said.

The report also said auto ABS-backed by commercial vehicles loans will remain stable on the back of healthy domestic economic growth.

Icra said the microlending segment is on a “road to resurgence” after the note-ban setback with an increase in repayment rates to 94 per cent in September from the low of 87 per cent seen during December 2016 during the peak of the note-ban move.

Source:

Interviews :: Home prices, loan rates unlikely to fall in 2018; time to buy: Harshil Mehta

Several cities under the Smart Cities initiative hold a distinct advantage and can be safe bets for ‘smart’ real estate investments, say Mehta.

Sarbajeet Sen | Retrived on 1st Jan 2018 | MoneyControl.com

The real estate sector has seen some major changes in 2017 including ushering in of RERA. It also had to bear the impact of demonetisation, which slowed down sales. In an interview to Moneycontrol, Harshil Mehta, Joint MD & CEO, DHFL, tells how he sees property prices and home loan rates moving in the New Year.

Year 2017 saw the Real Estate Regulation Act (RERA) coming into play. How has the new Act impacted the real estate market?

RERA is a well-timed effort by the government and a good step towards accomplishment of ‘Housing for All by 2022’ and other housing and housing-development related initiatives. Several states have implemented RERA and has positively impacted buyer sentiments as a result of the mandatory disclosures of project details and strict adherence to project deliverables such as the area, legality, amenities and the quality. It has also ushered a more transparent ecosystem for developers and housing finance companies. DHFL has also undertaken a drive to assist developers in various states to help them understand the regulatory implications of RERA and become RERA compliant.

How do you see home prices moving in 2018, especially in the affordable segment?

We do not foresee any reduction in prices in the affordable housing segment because of the increasing demand and the limited supply to meet this demand. To attract buyers and maintain sales volume, developers are launching attractive offers and other benefits to encourage customers to fulfill their aspiration of owning their dream home.

Home loan rates have come down substantially. Do you think there is a likelihood of further lowering of rates by lenders?

Owing to the last few monetary policies, home loan rates have stabilised and we do not foresee any further reduction.

So, for those waiting to buy property, do you think this is a good time?

Yes, it is a good time for the buyer.

What is the loan bracket that you are seeing the largest offtake?

We have been seeing a steady offtake in the affordable housing segment that ranges from Rs 15-30 lakhs. The affordable category has received a strong boost led by the government’s various incentives and efforts to stimulate the industry. All these efforts have started to show visible impact on the ground. Benefits from the recent Credit-Linked Subsidy Scheme (CLSS) under PMAY and lower interest rates have further given a boost to the consumer’s loan eligibility.

What is the home price segment DHFL is targeting?

Since inception, DHFL has always targeted the affordable housing finance segment catering to the low and middle income in the semi urban and Tier-2 and Tier-3 towns. This has remained unchanged for the last 33 years. As we mentioned earlier, we are witnessing strong uptake in the affordable finance segment driven by the incentives and conducive industry dynamics particularly from Tier 2 and 3 towns and cities which are emerging as India’s new growth engines.

Is government’s push for affordable housing having a bearing on loan offtake?

The Indian housing finance industry and, in particular, the affordable housing segment, is witnessing one of the most exciting times. Over the last few months, the Government has been taking several significant, growth-oriented steps to develop demand as well as generate greater supply through impacting policy frameworks towards greater financial inclusion. Granting infrastructure status to the real estate industry, announcing the extended CLSS to include MIG 1 & 2 and most recent announcement on RERA, are some commendable efforts to stimulate demand of affordable housing. These customer friendly measures and efforts have definitely given a strong fillip to loan offtake.

What are the market and sub-markets where you are seeing a high demand for home loan?

Affordable Housing has clearly been a central growth agenda for the Government. Initiatives such as ‘Housing for All by 2020’, PMAY, CLSS, home loan rate cuts and housing regulations such as RERA has considerably sparked interest for affordable housing options across the consumer pyramid. Most of the first-time home buyers fund their property purchase through home loans. As a result, there has been a surge in home loan demand across India specifically the Tier-2 and Tier-3 markets.

What according to you are the best emerging real estate investment destinations across the country?

Post the launch of the Smart Cities Mission in 2015, the Government shortlisted cities from all regions of India having high economic and industrial potential. Smart cities will become catalysts in improving the quality of life and give a major fillip to the real estate in urban locations. Considering the upcoming infrastructure projects and other growth drivers, several cities under the Smart Cities initiative hold a distinct advantage and can be safe bets for ‘smart’ real estate investments.

What more, according to you, needs to be done to boost the housing sector?

For all the benefits to make real impact, customer centricity is becoming key. Financial institutions and HFCs need to focus on making the entire experience of home purchase more seamless and customer friendly. Companies need to think how we can address their financial needs across their whole financial life cycle through customised products.

To further boost the affordable housing sector, external commercial borrowings (ECB) should be extended to housing finance companies to enable onward lending to developers in the segment. Also, single-window clearances is another step towards increasing development in the affordable segment and ensuring timely delivery.

Source: https://goo.gl/S2NiV6

Interviews :: Home loans slowdown driven by RERA will reverse in 8 months: ICICI Bank honcho Ravi Narayanan

Interview: Ravi Narayanan, senior general manager and head – retail secured assets, ICICI Bank.

By: Shritama Bose | Updated: November 28, 2017 12:20 PM | Financial Express

The home-loan market seems to have slowed down, first because of some postponement of demand with demonetisation, and then with the implementation of RERA. Where do you see things going from here?

The supply in the system had anyway started reducing in the last two years. Between September 2016 and September 2017, supply has dropped by over 10-12% in residential real estate in the top 40-45 cities. Till a year back, the inventory overhang used to be about 18-20 quarters in the industry. Along with supply, absorption of units was also coming down because of various reasons, one of which could be demonetisation. People expected a price correction. With RERA coming in, my estimate is that the supplies will go down still further because the act has put in various guardrails as to how the builder must manage the finances available for the project. This augurs well because inventory overhang should not be so much. The second outcome of RERA will be a rise in customer confidence. So once this whole dust settles, we will see pick-ups rising. So there will be a decrease in inventory and an increase in sales and that should be good for the industry.

Won’t that also cause asset prices to rise?

It will follow a pattern. There is an oversupply right now. If the demand-and-supply gap comes down drastically, then the prices will go up. In the next six to eight months, a lot of consolidation might happen in projects underway, which may not be amenable for prices to go up. Prices will remain, more or less, at the same level or there may be some fall in prices. Also, in the last six-seven years, real estate has seen a slight downturn. Typically, the industry follows an eight-to nine-year cycle. So in my opinion, 2018 will again see a rise in sales.

A development that followed demonetisation was the expansion of the credit-linked subsidy scheme (CLSS) for housing. Are you seeing supply and offtake picking up in that category?

Over 60% of new home launches in the industry in the first half of FY18 had ticket sizes under Rs 25 lakh. Because of this scheme under the Pradhan Mantri Awas Yojana, a lot of projects have started coming up in this category. Builders are also entitled to certain benefits if a part of their projects are of sizes below a certain threshold.

So is the phenomenon of builders allocating more space to smaller units a countrywide one?

This is happening primarily in Mumbai and Pune. Some of it is happening in Chennai and Bangalore. But, it is not happening across the country as yet. That’s partly because you have to keep operating costs and land cost under control to be in affordable housing. It is a very price-sensitive market. However, given the focus on this sector from this government, there’s bound to be more players flocking to it.

In mortgages, banks have continuously been losing market share to housing finance companies (HFCs). Have they actually weaned away bank customers for their growth?

No, because the mortgage industry is really big. The mortgage book of the country is now at Rs 15 lakh crore; over the next few years, at a CAGR (compound annual growth rate) of 20%, it should go up to Rs 50 lakh crore. When the pie is so large, everyone will have a share. It’s just a question of how each player orients themselves. Today, most banks are focused on the metros, while HFCs are operating in the peripheries (of cities). So we are not meeting each other much. But very soon, it will all become one playground. Banks venturing into the peripheries will be much faster because we anyway have branches.

ATM :: Planning to invest in home? Here is how you can raise your down payment

With interest rate-cuts and increased liquidity with banks following the demonetisation, loan products have more accessible.

Adhil Shetty | Published: May 11, 2017 4:02 PM | Financial Express

Consumers with healthy credit scores today would be receiving loan offers aplenty. With interest rate-cuts and increased liquidity with banks following the demonetisation, loan products have more accessible. Yet availing a home loan for the very first time remains a complex experience that loan seekers view with trepidation.

There are often misconceptions about what a home loan can do, and what it costs. For instance, you may be of the belief that the loan granted will match the property price. That is untrue, as financial establishments expect you to pay the margin amount.

The margin amount is another term for down payment for your new home. It could be anything between 15% and 20% of the home’s net value. For a first time home buyer, it is no easy task raising this money.

Here are some ways to help.

1. Strategic savings

Nothing beats strategic savings and for this you need to start your planning early. It involves you visualizing your long-term fund needs—including the need to buy a home—and beginning to save and invest accordingly. Begin with simple and accessible investment tools such as mutual funds or recurring deposits. Slowly and surely, you’ll be able to build your deposit over time. You can be efficient at this by locking in your savings at the start of the month. The earlier you start, the sooner you build this fund for your down payment.

2. Take loans but exercise restraint

There could be a situation where you are in urgent need of funds for the down payment. You could consider taking a personal loan to meet the need. Yet, you need to do this in a controlled manner. Having an existing loan will reduce your ability to take on, and repay, additional loans such as a home loan. You would find your finances stretched as you attempt to pay two EMIs at once. This isn’t an ideal situation to be in and is recipe for a financial disaster, in case you were to temporarily lose your ability to generate income. Therefore any loans for down payments need to be taken thoughtfully, and settled as soon as possible to reduce monthly EMI liabilities.

3. Mortgage another property

If you are confident that your current income can take care of EMIs of more than one loan, you could consider a loan against property. You can claim this loan against several options. For example, an existing property or home could be mortgaged. You could also claim it against assets such as shares, jewelry, PPF account, and LIC policies. There also exists the option of taking a loan against rent.

4. Withdraw from your PF account

As per the new EPFO norms, you are now allowed to withdraw up to 90% of your EPF corpus. Not just that, you could also withdraw from this corpus to pay for your EMIs. This scheme was recently implemented keeping in line with the Housing For All initiative of the central government. A word of caution: your PF corpus is meant to help you generate a pension income in retirement, so if you intend to redeem it for a property purchase, you must replenish it soon, or create a backup pension fund to meet your future needs.

5. Deferred down payment

You have the option of requesting a deferred down payment when purchasing a house from a well-known property developer. Under this, you will have the choice of dividing the down payment into multiple instalments. These instalments can be paid over a jointly agreed period of time. Let us say that you have to make a down payment of Rs. 10 lakh. Ask the builder for a time frame of five months to pay Rs. 2 lakh per month.

6. Liquidate your investments

Before you decide to make a property purchase, take stock of your savings, investments and assets. Anything from a vehicle to a part of a property you own can be liquidated for a down payment. Bank deposits, gold, mutual funds, shares etc. can be disposed. This should be carefully done so as to not disturb other financial objectives.

7. Approach an NBFC/ HFC

Non-Banking Financial Companies (NBFCs) and House Finance Companies (HFCs) provide loans that can help you cover a larger part of your fund requirement. For example, they may provide a loan to cover your registration and home repair costs as well. The entitlement of the loan, of course, will be calculated on the basis of your ability to repay.

Always remember to not act in a hurry. Think long and wise about the route you are taking to raise the down payment for your house. It is also advisable to wait and let an offer go if you cannot make the down payment, as there will always be another good offer in the future.

(The writer is CEO, BankBazaar.com)

Source : https://goo.gl/8ixiEW

ATM :: How to withdraw 90% of your provident fund to buy a house

May 12, 2017 | 11:39 IST | SOURCE : Economic Times | Retrieved from Timesnow.tv

In an effort to make its ‘Housing for all by 2022’ a success, the government has allowed for EPFO members to withdraw up to 90 percent of their provident fund (PF) accumulations to make down payments to purchase a house and to pay housing loan EMIs.

Pre-requisites for PF withdrawal

In order to dip into the provident fund saving, the new rule highlights that the PF holder will only be eligible if he/she has been a contributing PF member for at least 3 years, and is buying property in a registered housing society that has at least 10 members.

Further, the property has to be purchased in the member’s name and cannot be purchased jointly with anybody else, except your spouse.

How the money can be used

The money withdrawn can only be used for an outright purchase, as a down payment for a home loan, for buying plots or for the construction of a house. The transactions can be made through central government, state government and even from a private builder, including promoters or developers.

Can the money be used to buy resale flats as well?

Unfortunately no, EPFO will only make payments directly to a cooperative society, the state government, central government, or any housing agency under any housing scheme, or any promoter or builder, in one or more installments. The rule will not apply to real estate purchases in the secondary market or resale transactions.

Can you withdraw both employee and employer contribution?

An EPFO member can withdraw his own share of PF contribution plus interest as well as the employer’s share of contribution plus interest.

Can you EMI payment through PF?

A PF member can use his PF contribution to pay full or part EMIs for a home loan taken in the member’s name. The EMI will be directly paid by EPFO to the government, housing agency or the bank.

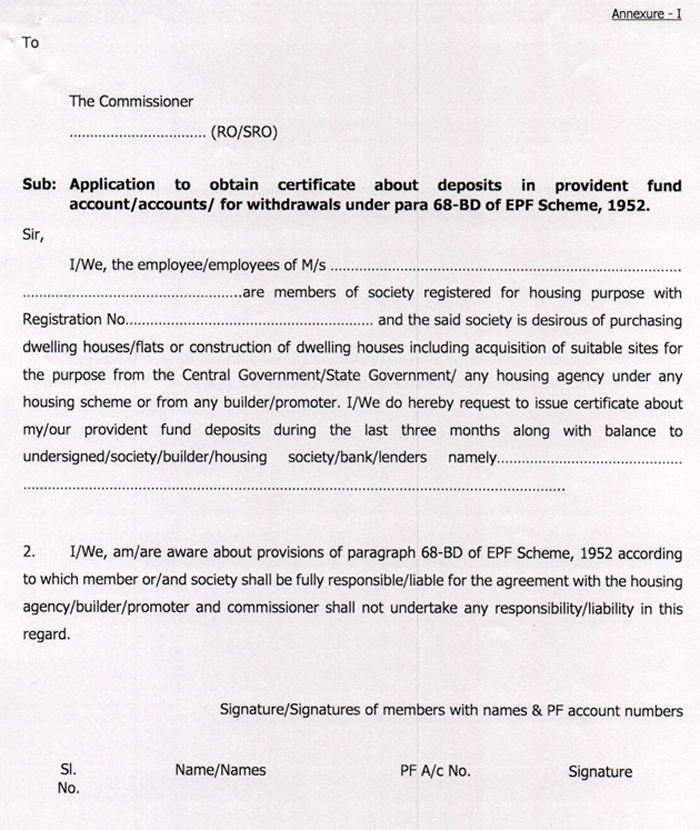

How to apply

A PF member can apply individually or jointly through a housing society to get a certificate from the EPFO.

Through Annexure I form, an employee can ask for the balance and the deposits made in the last three months before applying. This will help the EPFO determine how much EMI can be arrived at.

Also, the employee has to mention the name and details of the bank or housing society to whom such certificate is to be issued.

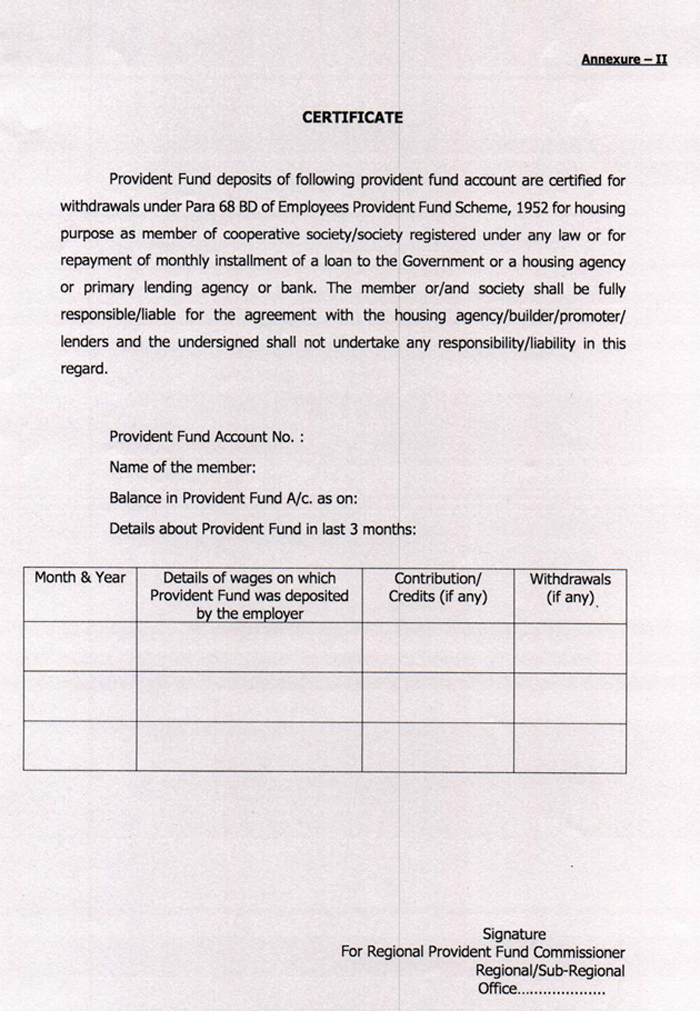

The EPFO then issues a certificate showing the outstanding balance and last three month’s deposit in the account. Alternatively, members can take printouts of their PF passbook downloaded from the EPFO website and submit it to housing agencies or banks.

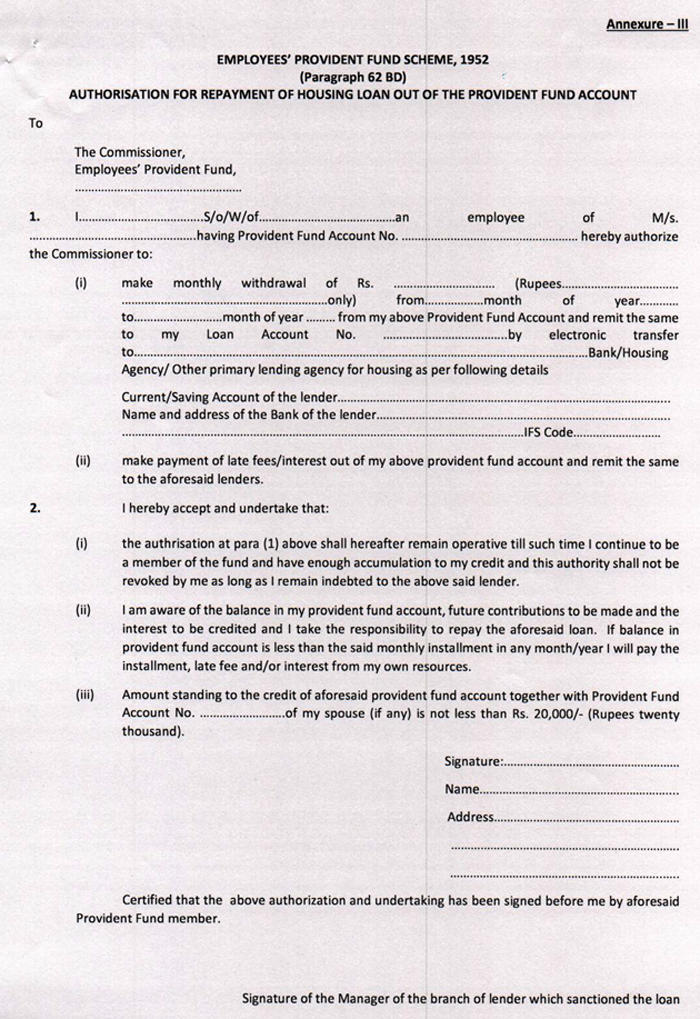

If a member wishes to use PF money to meet EMI’s, then in addition to Annexure I, an authorisation by the member is to be filled in a prescribed format. It will carry details such as PF amount, PF and loan account number, lender name, address etc. One has to get this form authorised from the lender i.e. branch manager of the lender who has sanctioned the loan. Once approved, EPFO will start transferring EMI’s online to the lender’s account.

What if an employee leaves his/her job?

The EPFO has made it clear that under no circumstances would it be liable for any default of payments to the lender. The EPFO will not be party to any agreement made between an EPFO member and a society or builder.

In case a member quits his job, the responsibility of repaying the loan would rest with the employee and not the EPFO.

Conclusion

While dipping into your PF account to make a down payment makes your life easier, it is important to remember, your PF is meant to take care of your post retirement needs, and depleting it may jeopardise your retirement.

So make sure you have a backup plan to meet postretirement needs through equity mutual funds or PPF.

Source: https://goo.gl/egUXjH

ATM :: Now is the time to book your dream home as property prices are set to head north

Real estate experts feel that home prices have bottomed out and they are likely to move higher in the new financial year. They say that this could be one of the best times to buy your home since loan rates, too, are attractive.

Sarbajeet K Sen | Source: Moneycontrol.com | Retrieved on 6th Apr 2017

The real estate sector has seen one of the worst times post-demonetisation with sales falling across the country, bringing down home prices. With the financial system having been successfully remonetised to a large extent, what is the outlook for the sector in the coming financial year?

Will activity in the real estate sector pick up 2017-18? Will sales pick up? How will home prices move in the coming fiscal? What will the factors driving real estate be post April 1?

The Confederation of Real Estate Developers Association of India (Credai) is optimistic that the new financial year would be good for the real estate sector and rising sales will lead to home prices moving up.

“The outlook for real estate in 2017-18 is very positive. The recent flurry of reforms and policy initiatives have set the tone for the future growth of the sector. This growth will be driven by efficient implementation of the initiatives and the subsequent rise in demand. We will see the residential sector take center-stage and be the driving force of the sector,” Getamber Anand, President, Credai told Moneycontrol.

Anand says that residential real estate prices have bottomed out and they would move up in coming months. He says those planning to buy homes should finalise the deal now.

“Prices in most markets have bottomed out and stabilised. Imbalance between demand and supply will result in an increase in property prices in the main markets. The recent policy moves have also restored consumer faith in the sector and the fence-sitters are slowly realising the timing is right for a purchase,” Anand said.

He also pointed out the loan rates are some of the lowest now. “With Pradhan Mantri Awas Yojana (PMAY) and the exemptions provided on housing loan in the Income Tax Act, the effective rate of interest for a home loan of about Rs 35 lakhs works out to about 5 percent only which improves the affordability factor and will further elevate the demand in the sector,” Anand said.

Surendra Hiranandani, Chairman & Managing Director, House of Hiranandani, agrees that low loan rates would push demand. “Post-demonetisation, interest rates have been reduced significantly on the back of huge inflows of deposits in the banking system making home loans cheaper. The various reforms undertaken by the government will address concerns faced by home buyers. Increased transparency and credibility will make it more attractive for consumes to invest in real estate,” Hiranandani said.

He also feels that homebuyers should seize the opportunity. “Homebuyers must use this opportunity and invest in properties that are available at attractive prices. They can purchase homes of their choice by full cheque payment. Those looking to buy resale properties can now avail higher finance through banks as the entire payment will happen through cheque,” Hiranandani said.

Hiranandani also feels home prices will move up after the turn of the financial year. “Home prices are expected to pick up in the second quarter of 2017 as the overall economy improves after demonetisation. Also, with Real Estate Regulation and Development Act (RERA), GST and other regulatory changes coming into effect in the coming months there is bound to be better transparency and credibility in the sector.

However, new launches would get impacted due to the implementation of these rules, so the demand for available inventory and ready-to-move-in homes will increase. The rise in demand will ensure that prices will move up again in good quality projects. This is the perfect time to buy a property,” he said.

Source: https://goo.gl/eB9J31

NTH :: EMIs for house in an urban area to shrink if bought under PM Awas Yojna

PM had announced interest subsidy of 4% on housing loans of up to Rs 9 lakh of those with annual income of Rs 12 lakh and of 3% on housing loans of up to Rs 12 lakh of those earning Rs 18 lakh per year.EMIs for house in an urban area to shrink if bought under PM Awas Yojna

TNN | Mar 23, 2017, 02.31 AM IST | Times of India

NEW DELHI: Your monthly home loan installment or EMI for a new property will come down by around Rs 2,000 if you are buying your first home in a city or town under the PM Awas Yojna (PMAY) and if your annual household income is in the range of Rs 12-18 lakh.

The government is offering an interest subsidy of 3-4% on borrowings of Rs 9 lakh to Rs 12 lakh even if the overall loan is higher. Loans availed from January are entitled for the subsidy announced by PM Narendra Modi as part of the post-demonetisation package.

On Wednesday, 70 lending institutions including 45 housing finance companies, 15 scheduled banks, regional rural and cooperative banks signed MoUs with National Housing Bank for implementation of the scheme for the middle class in urban areas.

Union housing and urban development minister M Venkaiah Naidu said that middle income groups (MIGs) make substantial contribution to the economic growth of the country besides paying taxes and deserved support to fulfill the dream of owning a house which is a basic and genuine aspiration. He urged banks and other lending institution to adopt pro-active approach to deliver the benefits to people.

The benefit will be extended to families as comprising of wife, husband and unmarried daughters and son. Moreover, unmarried and earning young adults buying their first house will be eligible to avail the benefit.

Though PM Narendra Modi had announced these subsidies on December 31to meet the aspiration of owning a pucca house for the tax paying large middle class, the operational guidelines could not be notified because of election code of conduct. TOI on February 15 had first reported about the interest subsidy scheme kicking off from January 1.

PM had announced interest subsidy of 4% on housing loans of up to Rs 9 lakh of those with annual income of Rs 12 lakh and of 3% on housing loans of up to Rs 12 lakh of those earning Rs 18 lakh per year.

“Those who have been sanctioned housing loans and whose applications are under consideration since January first this year are also eligible for interest subsidy,” a housing ministry spokesperson said.

As per the scheme, the tenure of loan has been stipulated to be 20 years or that preferred by the beneficiary, whichever is lower. The total interest subsidy accruing on these loan amounts will be paid to the beneficiaries upfront in one go thereby reducing the burden of EMI.

Sriram Kalyanaraman, managing director and CEO of National Housing Bank said the interest subsidy of 4% will bring down EMI of beneficiaries by Rs 2,062 per month on a housing loan of Rs 9 lakh and interest subsidy of 3% will bring down EMI by Rs 2,019 on a loan of Rs 12 lakh, considering normal housing loan interest rate as 8.65%.

He added said during 2015-16, against total new bookings of 28.9 lakh units with loans of up to Rs 10 lakhs each, public sector banks and housing finance banks advanced loans of Rs 9.5 lakh crore and accounted for 64% of total bookings.

Source : https://goo.gl/SfohoV

NTH :: Interest subsidy on housing loan applicable from January 1, 2017

By Dipak K. Dash, TNN| Updated: Feb 15, 2017, 02.37 PM IST | Economic Times

The rebate in interest rate is likely to push housing demand in urban areas and thereby help the sector to revive.

Anyone who has applied and got a home loan sanctioned after January 1 and has less than Rs 18 lakh annual income, will be eligible for interest subsidy of 3-4%. Prime Minister Narendra Modi had announced the interest subsidy on December 31, though the annual income criteria was not announced.

This benefit interest subsidy can also be availed by unmarried and earning young adults for acquisition/ construction of a new house including repurchase. Moreover, flats measuring up to 960 sq ft and 1,184 sq ft will be eligible for 3% and 4% interest subsidy respectively for the specified income group.

TOI on January 4 had first reported that the housing ministry had moved a proposal to provide 4% rebate on interest rate for loans up to Rs 9 lakh and this can be availed by those who earn up to Rs 12 lakh annually in urban areas. Similarly, people earning up to Rs 18 lakh annually will be eligible to avail 3% rebate on interest for loans up to Rs 12 lakh.

Sources in housing finance sector said that though the government had finalised the policy, it has not yet announced it because of election code of conduct. In fact, the ministry had held a meeting with banks and housing finance companies where the operational guidelines for “credit linked subsidy scheme for middle-income groups (CLSS-MIG)” was discussed.

The rebate in interest rate is likely to push housing demand in urban areas and thereby help the sector to revive.

Source: https://goo.gl/XAtj5v

ATM :: Real Estate is dead – long live Real estate

By Harsh Roongta | Facebook post

Ok – I admit that the headline is to grab your attention. But in this budget the finance minister has proposed several clever changes in the tax laws that will discourage investments in multiple properties yet at the same time encourage first time home buyers to buy their homes rather than live on rent.

Currently 4 factors drive investments in multiple real estate properties. First- Real estate is the only asset class left that still easily allows laundering of large unaccounted “black” income. Second – most investors have the ability to take loans for buying a residential property. Third – these loans are very cheap as the interest paid on these loans is fully tax deductible and the resultant loss can be set off against business income or salary income. Fourth- the “capital gains” on sale after 3 years are treated in a concessional manner and can be completely tax free if reinvested in another property and become fully laundered after the second round of investment.

The proposed changes hit at the first and the third factors. The restrictions on receiving any cash in excess of Rs. 3 lakhs is bound to create difficulties in paying and/or accepting large sums of cash that are typically required on these kinds of property purchases. Another factor is the effective removal of the tax deductibility of home loan interest on multiple properties makes the home loans much more expensive. I think these 2 factors will have a far greater negative impact then the small positive factor of making the long term capital gain period at 2 years instead of 3 years earlier. These kind of properties are rarely held for decades and hence the other positive factor of change in indexation date will have no impact on holding of multiple properties.

Once the impact of these factors sink into the market it will have a further adverse effect on the already low demand for high value properties. Meanwhile the government has already announced a slew of measures to encourage the buying of reasonably sized (650 sq ft carpet area or around 1000 sq ft – saleable area or a decently sized 2 BHK flat) affordable homes in urban areas. Full details of the new subsidy scheme are still awaited. If newspaper reports are to be believed then households having income of upto Rs. 18 lakhs per year will also be eligible for a one time subsidy of around Rs. 2.20 lakhs through their home loan lender. The existing subsidy scheme is well designed with no restriction on sale of the houses bought under the scheme nor is there a limit on the value of the houses or the loan amount. The limits are only on household income and flat size. It also requires that it should be the first purchase for the household and the women of the house should be the owner or joint owner and the house should be in an approved project. It’s a scheme that is already working well for lower income households (income upto Rs. 6 lakhs per annum) and there is no reason it will not work equally well for the wide swathe of middle income households that are expected to be covered. Developers are also given tax benefits on profits from affordable home projects. Both these things can create a massive demand for “affordable” homes. Hence Real Estate is dead. Long live Real estate.

Source: https://goo.gl/MAzzoZ

NTH :: Consumers expect fall in home prices; may hamper property sales

By Saikat Das, ET Bureau | Updated: Dec 26, 2016, 09.16 AM IST | Economic Times

MUMBAI: Housing finance firms downplayed stress in the real estate sector as fallout of the sudden demonetisation early last month in meetings with regulator National Housing Bank, but fear consumer sentiment expects prices to fall, and that could hamper home sales in the coming months, crimping growth, multiple sources familiar with the matter told ET.

In the past two weeks, NHB has held three meetings in Delhi, Mumbai and Chennai with 81 housing finance companies to assess the impact of demonetisation.”We have held regional level conferences of housing finance companies (HFC) assessing the situation in light of demonetisation,” Sriram Kalyanaraman, CEO of NHB, told ET. “We also discussed the challenges and opportunities in this sector and also how the HFCs can work more towards fulfilling the Housing-for-All goal (by 2022).”

Kalyanaraman did not elaborate on the challenges but some participants said they drew the regulator’s attention to escalating consumer expectations on falling prices. Rental yield and mortgage loan yields have fallen to about 3.4% (tax adjusted), which could be a key trigger to rake up housing demand from home buyers living in rented accommodation now, a head of a large HFC said.

Findings-

Many consumers are holding back their decision as they expect sharp fall in prices.This could hurt home loan demand, they said, seeking NHB’s intervention to scotch such speculation. The regulator believes that there could be some short term corrections (10-15%) in home prices but it would eventually rise when genuine tax payers line up for transparent deals.

The regulator encouraged HFCs to promote small value affordable housing finance loans to coax salaried people being keen on buying homes. “We do expect a surge in affordable housing both on supply and financing side,” said Kalyanaraman, thanks to falling interest rates, higher transparency with RERA (Real Estate Regulation Act) and expected lower land prices.

Source: https://goo.gl/9i5Sig

ATM :: Why property is likely to be cheaper after demonetisation

By Sanket Dhanorkar | ET Bureau on 21st Nov 2016 | Economic Times

For many city dwellers, owning a home is always a distant dream. Unaffordable real estate prices compel them to stay in rented properties instead. However, several events and trends taking shape now could soon turn that dream into a reality.

The government’s surprise move to clamp down on black money hoarders through the ban on Rs 500 and Rs 1,000 currency notes is expected to have a cooling effect on certain pockets of the residential market in the country. The housing market is a hot-bed for the indiscriminate use of black money. Many developers, resellers and homebuyers insist on having hard cash as a component of payment in real estate deals.

The recent ban on high value currency notes is expected to deal a body blow to this practice. Another likely side effect of the move is a down ward pressure on the interest rate structure. This would come as a relief to people who cannot afford the high EMIs on housing loans. In addition to these factors, many developers are also aggressively turning towards the affordable housing segment. This effectively opens up another avenue for those who find themselves priced out of the housing market in metropolitan cities.

Further, with many states likely to enforce the buyer friendly provisions of the Real Estate Regulatory Act, homebuyers can expect more transparency. This would also provide them protection from delays in construction and handover, as well as other unscrupulous practices employed by developers. In the following pages, we will outline the opportunities these developments are likely to present for homebuyers, and delve into the emergence of the affordable housing segment.

Fewer new homes in the market

Number of new projects declined in top 9 cities

All cities have witnessed a drop in launches

What awaits housing?

Industry experts believe that the housing market will experience a lull in the coming months, as these developments take their toll. Homebuyers can expect property prices to come down in certain pockets, which would provide an opportunity for them to make their move.

Rohit Gera, MD, Gera Developments, asserts, “There is no doubt that sales which involve the exchange of cash will be affected. This will impact land prices too. If land prices crash on this account, there will be a likelihood of property prices coming down as well.”

As CARE Ratings points out in its report, developers are already grappling with the problem of slow sales, which is leading to rising inventory levels in all major micro markets. Given the growing uncertainty and negative impact on demand caused by demonetisation,people are likely to postpone their plans to buy property, which would lead to further increase in inventory levels. As a result of this, developers and sellers could be compelled to cut down prices to drive sales. Most experts are of the opinion that the secondary market will be visibly impacted, since it deals with a significant amount of cash. ..

Ashwinder Raj Singh, CEO, Residential Services, JLL India, says, “The real estate sector will definitely be affected by the demonetisation exercise, as it has traditionally seen a very high involvement of black money and cash transactions. However, almost all such incidences have been in the secondary sales market, where cash components have traditionally been a ‘must’.” He further states that projects undertaken by reputed and credible developers in the top eight Indian cities will remain more or less unaffected.

This is because buyers who invest in such projects take the home loan route, and all transactions are carried out through legal channels. Hence, the primary market is likely to remain relatively untouched by the radical step. However, home buyers can look forward to better pricing in the secondary or resale market.

“For buyers, this could be a great opportunity to get a deal, especially in ready to move-in projects, as real estate prices are likely to face a downward pressure and a few sellers may be more willing to negotiate and lower the prices of housing units,” says Khurshed Gandhi, Managing Director, Consulting Services, India, Cushman & Wakefield.

Excess inventory build up in this segment has already put a lid on prices, making existing possession-ready properties a more viable option for buyers. For those who are keen on buying directly from the developer, the options might be limited.

However, the demonetisation move could prove to be a boon for those who have been looking for deals in the high-end or luxury housing segment. According to Rohit Poddar, MD, Poddar Housing and Development, this segment could face a big impact in terms of pricing. “A large cash component is the norm in the luxury housing segment, as many buyers insist on using cash.

But with the government clampdown, sales in this segment are likely to dip, leading to price cuts. Some developers have already slashed prices.” The affordable luxury segment, which is priced within the reach of buyers slightly below the HNI category, may offer good opportunies in the coming months.

Home loan rates will soften

If you have been putting off buying your dream home because you’re not ready for the high EMIs, you can expect to have more breathing room now. This is because lending rates are likely to come down further. Due to demonetisation, a large amount of cash in circulation will be brought within the purview of the formal banking system through low-cost current account and saving account deposits. Since this will reduce the dependence of banks on higher cost borrowings, banks are likely to slash the marginal cost of funds based lending rate (MCLR). This will accelerate the fall in home loan interest rates, since CASA ratio is used in computing MCLR.

Fixed deposit rates have dropped across banks

Increased liquidity has brought down deposit rates, which would in turn lower lending rates.

If home loan rates are cut by 25 BPS

The surge in low-cost deposits is likely to bring down bank deposit rates and ultimately lead to a drop in lending rates as well. Here’s how a decline in home loan rates will impact borrowers.

If you have a loan of Rs 50 lakh at 9.5% for 20 Years : A 25 basis point cut will reduce the EMI by Rs 812 per month.

Rs 46,606 Old EMI at 9.5% : Rs 45,793 New EMI at 9.25%

Lenders usually leave the EMI amount unchanged and reduce the loan term when rates are cut. The extent of reduction will depend on the balance tenure of the loan. The longer the remaining tenure, the greater the impact.

Balance loan tenure at 9.5% : 5 Years

Number of EMIS reduced at 9.25% : 1 EMI

Balance loan tenure at 9.5%: 10 Years

Number of EMIS reduced at 9.25%: 2 EMI

Balance loan tenure at 9.5% : 15 Years

Number of EMIS reduced at 9.25% : 5 EMI

Balance loan tenure at 9.5%: 20 Years

Number of EMIS reduced at 9.25% : 12 EMI

MCLR rates change

The 15-20 bps reduction in Axis Bank’s MCLR shows the emerging trend

While the currency notes ban has left less cash in the hands of consumers, thus driving down consumption for the time being,taking older Rs 500 and Rs 1000 notes out of circulation is also expected to have a longer term deflationary impact on the economy. It will bring about a slowdown in highticket purchases such as white goods, jewellery, high-end retail and of course, real estate.

“Banks that have excess liquidity will look to sanction more loans going forward, and will probably effect another round of interest rate cuts on home loans,” says Adhil Shetty, CEO, BankBazaar.

“The sudden decline in money supply and simultaneous increase in bank deposits is going to adversely impact consumption demand in the economy in the short term. This coupled with the adverse impact on real estate and informal sectors, may lead to the slowing of GDP growth,” says Sunil Kumar Sinha, Principal Economist and Director -Public Finance, India Ratings & Research.

This will probably lead to a softening in inflation, which may prompt the RBI to carry out interest rate cuts and give more leeway for banks to lower their lending rates. “With this move, we also expect that the RBI will reduce rates, which will have a direct impact on home loan interest rates, thus giving consumers more cash flow to invest in real estate,” says Brotin Banerjee, MD & CEO Tata Housing Development Company. Several major banks like SBI, HDFC and ICICI, have only recently slashed home loan rates

SBI continues to offer the lowest interest rates under its recent festival offer of 9.15% for loans of up to Rs 75 lakh sanctioned in November and December this year. Private lenders HDFC and ICICI Bank now offer interest rates at 9.2% for home loans of up to Rs 75 lakh, down from 9.35%. Experts predict another 10-15 bps reduction in interest rate soon.

Budget-friendly alternative

Until recently, developers were more focused on offering solutions in the premium and upper-mid range segments, since they expected high demand in this space. However, there has instead been a visible shift in demand from big ticket purchases mostly led by investors, to purchases by end-use customers, who now constitute almost 90% of aspiring home buyers. As a result of this, builders are increasingly shifting their attention to the affordable housing segment.

“Not only are prices down in most cities, but developers have also introduced schemes and incentives to make deals more lucrative.” Anuj Puri Chairman & Country Head, JLL India

Data from Cushman & Wakefield, a real estate consultancy firm, shows that the number of launches in this segment in the first half of the year has doubled from the same period last year. In the top eight cities alone, 17,000 new affordable housing units were launched, out of a total of 60,000.

Pune saw the highest supply, with 4,170 new units being launched. Bengaluru came a close second with 4,155 units. Affordable housing is distinct from low-cost housing, which is meant for the economically weaker section and is equipped with only basic housing facilities.

These units are typically up to 300 square ft. in size, and priced up to Rs 15 lakh. Affordable housing, on the other hand, is mostly meant for the middle-income families who can afford to spend Rs 30-50 lakh. These are mostly located on the peripheries of the bigger cities. Anuj Puri, Chairman & Country head, JLL India, says, “Constraints like the nonavailability of land and high costs often make housing within primary city boundaries unaffordable. Therefore, affordable housing projects are largely located in the outer peripheries of these cities.”

However, these provide all basic amenities, and some large projects even have social amenities such as landscaped gardens, schools and shopping centres. “Staying on the outskirts is no more considered to be an inconvenience. Additionally, these newer locations are well planned and offer a lot of green spaces as compared to city centers,” Banerjee points out. However, to keep costs under check and improve affordability for the buyer, developers typically offer units in 1RK and 1BHK size, with a reduced saleable area of up to 350 square ft. for 1RKs and up to 500 square ft. for 1BHKs.

The average size of affordable housing units launched in the first quarter of 2016 was reduced by 11% from those launched in the corresponding period in 2014. In Delhi NCR, this reduction was to the tune of 8%. Many projects in this segment are coming up in the form of integrated townships, which attempt to provide maximum value for money to buyers. With more serious developers entering the segment, there has been a distinct improvement in product quality. “The sales of smaller builders are being cannibalised by branded developers, who offer a better quality of lifestyle,” Poddar observes.

Homes are getting smaller with time

Apartment sizes sold in top 9 cities

Bengaluru, Mumbai and Pune are driving sales for smaller sized units

Is it right for you?

If you resent shelling out large amounts of rent, but have been afraid of taking on the burden of high EMIs, affordable housing could be your way out. “Thanks to the recent spate of price declines driven by the market realities, affordable housing has never been more accessible to the common man. Not only are prices down in most cities, but developers have also introduced various schemes and incentives to make the deals more lucrative,” Puri adds.

Further, in recent times, the government has also introduced various special incentives in terms of tax benefit to both the developer and homebuyer. There are also several schemes aimed at promoting public-private partnerships for the development of affordable housing projects, in order to realise the government’s vision of ‘Housing for All’ by 2022.

Units lie unsold across segments

Noida and Mumbai together account for 41% of unsold inventory in this segment

The Budget 2016 directive allowing 100% deduction on profits earned by developers of affordable housing projects provides an added incentive to builders. It is also likely to lower the chances of delays in the construction and handing over of possession, which has become the norm in recent years. This is because the budget has put the onus on the builders to finish houses within three years of starting work, if they are to avail of the exemption for affordable homes.

“The affordable housing policy has been drafted to incentivise timely delivery, and will motivate developers to finish their projects and handovers according to set timelines. Further, with the Real Estate Regulatory Authority coming in soon, timely delivery will become a norm,” says Jayashree Kurup, Head, Content and Research, Magicbricks.

Old inventory remains unsold

NCR accounts for nearly 30% of unsold inventory aged more than 2 years

The government’s move to exempt service tax on the construction of affordable houses of up to 60 square metres will also fuel interest in this segment, and keep prices low. There is also a cost benefit for developers in building these units. The project completion time is much shorter in this segment, and sales are realised much more quickly than for mid-and-high range properties.

Further, for first-time homebuyers, the government offers an added tax deduction of Rs 50,000 per annum on interest payment for housing loans of up to Rs 35 lakh, for properties valued at under Rs 50 lakh. This is over and above the Rs 2 lakh deduction allowed on interest payment on any housing loan under the Income Tax Act.

According to experts, affordable housing is better suited for end use, than it is for investment. Since the scope for price appreciation is limited in the segment owing to smaller unit size and remote locations, homebuyers should consider various aspects before opting for affordable housing project, asserts Gulam Zia, Executive Director, Advisory, Retail and Hospitality, Knight Frank India.

According to Puri, focusing only on the price tag is a bad idea, as this can trick the buyer into investing in an inferior project, or one located in an area with little connectivity. “Since most affordable housing projects are ough background check of the developer before putting the money into any project is crucial. “Buyers should verify the developer’s credentials based on their project completion timelines, reputation in the market, customer feedback, and how much experience they have in the construction business,” cautions A.S. Sivaramakrishnan, Head, Residential Services, India, CBRE South Asia.

Better than renting

Given the conditions at present, Kurup advises that young couples who pay rent should consider buying ready-to-move-in apartments which have EMIs of up to 25% more than their monthly rent. However, it is important to ensure that the distance to their workplaces does not increase so significantly that the expense it adds to their monthly outflow. “Buy according to your current needs, and ensure that the price fits into your budget. Over the next five years or so, your property value will go up, and then you can sell it and use the proceeds to upgrade,” Kurup adds.

Puri believes the market is currently very well suited for young working couples and professionals. “The ideal strategy for them is to invest in a well-located ‘starter home’ in a project by a reputed developer, with a view to upgrading in the future.

“Affordable housing is better suited for end use than for investment, given the limited scope of price appreciation in the segment.” Gulam Zia Executive Director – Advisory, Retail and Hospitality, Knight Frank India

By then, suburbs which are currently in the initial stages of development would have sufficient infrastructure to support constructed in remote locations, in order to take advantage of the availability of cheaper land, the most important criteria for selecting the right project is availability of transportation facilities in the vicinity, and its connectivity with the city centre,” Zia adds.

“The buyer should also evaluate if the lifestyle offered by the affordable home is in line with their aspirations,” Gandhi adds. Social infrastructure, like education centres and healthcare facilities, should also be within a reasonable distance from the housing project. Most importantly, conducting a thora decent lifestyle.” He points out that Navi Mumbai, Bengaluru, Chennai and Pune are obvious investment destinations because of their accelerated growth and employment opportunities.

“Cities which have a robust economy and multiple employment opportunities are the best options for homebuyers in the affordable segment. Cities like Mumbai, Pune, Bangalore and Hyderabad are therefore likely to witness sustained demand for affordable housing projects in the future,” Gandhi concludes.

Grey market interest rates down to 5%

Interest rates have dropped to 5% from as high as 30% in the grey market, where a flourishing under-the-counter lending business has been stifled by demonetisation. Under grey market lending schemes, investors pool in money that is lent to real estate developers, small companies and people in distress at high interest rates. These loans are given in cash without written agreements.

Now loans can’t be given or repaid in the demonetised Rs 500 and Rs 1,000 notes, which were the most widely used. “The interest rates charged were anywhere from 18% to 30% per annum,” said an investor who is part such an arrangement. “Those who were to return money borrowed earlier are offering it in high denomination notes, and we ourselves are stuck with these. Interest rates have come down to minimum, about 5% per annum or even less,” he added.

Affordable projects coming up

The launch of affordable housing projects has doubled in the first half of 2016-17, far ahead of other segments.

More launches across cities

Ahmedabad and Delhi saw the highest proportion of launches in affordable housing segment in recent times.

Source: Cushman & Wakefield

Infrastructure adds advantage

Planned infrastructure projects that promise better connectivity can boost affordable housing in some pockets.

Source: https://goo.gl/Ymg4YU

ATM :: Cash no longer king, realty prices may drop

Prabhakar Sinha | TNN | Nov 9, 2016, 05.58 AM IST | Times of India

NEW DELHI: The government’s decision to withdraw existing currency notes of Rs 500 and Rs 1,000 from circulation will severely impact the real estate sector, especially secondary market transactions where 60:40 – the ratio of legal to black money – had become a norm of sorts.

The primary market, where one buys a house in a project directly from a developer, will not be directly impacted by the measure. But market players said that the impact on the secondary market is set to hit the overall sentiment, which has remained subdued for the past few years.

“The effects of the currency measure will be far reaching and immediate, and will shake up the sector in no uncertain way,” said chairman and country head of JLL India, Anuj Puri.

President of the Confederation of Real Estate Developers’ Associations (Credai) Getambar Anand, however, argued that most of the houses in the primary market are sold on bank finance. “Therefore, the black money element will not have any impact. As the values of units are publicly known, they cannot sell other units at a discounted price in white and the rest on cash payment,” the head of the industry lobby group said. But given the widespread use of cash when it comes to payments to local authorities and politicians in office, a lot of the transactions by developers are conducted in cash, some of which “managing” their own books.

As PM Narendra Modi said, real estate and land purchases are seen as one of the most prominent segments of the cash economy.

In most developed areas in metro cities, the initial transaction is through legal channels. But when it comes to a resale or a secondary market transaction, the seller often seeks cash payment to save on capital gains tax. For the buy er, the attraction of cash deals is that they can report a lower value to the registration office and reduce the stamp duty burden. In addition, this is an outlet of cash lying idle with buyers which cannot be parked in the banking or financial sectors to reap returns.

Because of black money, the value of real estate in many markets in metros have appreciated sharply.

After the PM’s announcement, the expectation is that use of cash will nearly vanish, at least for the next few months, resulting in a sharp drop in prices in the secondary market. This will have an effect on the primary market as well.

Suorce: https://goo.gl/BEXmIr

ATM :: Six things about home loan incentives you didn’t know about

Chandralekha Mukerji | ET Bureau | October 5, 2016

2016 is looking to be one of the best years for home buyers.

More tax benefits, rate cuts on loans, stagnant property prices, new launches in the ‘affordable’ segment with freebies and attractive payment schemes.

Many of you will be looking to take advantage of these benefits and buy a house.

While hunting for a house at the right price, you’ll be haggling with the bank to cut a loan deal too.

Even if you get a discount on both, your tax bill can burn a hole unless you know the rules well. Here goes a list of six lesser known and often-missed tax benefits on home loan.

You can claim tax benefit on interest paid even if you missed an EMI

Unlike the deduction on property taxes or principal repayment of home loan, which are available on ‘paid’ basis, the deduction on interest is available on accrual basis.

Meaning, even if you have missed a few EMIs during a financial year, you would still be eligible to claim deduction on the interest part of the EMI for the entire year.

“Section 24 clearly mentions the words “paid or payable” in respect of interest payment on housing loan.Hence, it can be claimed as a deduction so long as the interest liability is there,” says Kuldip Kumar, partner-tax, PwC India .

However, retain the documents showing the deduction so that you can substantiate if questioned by tax authorities. The principal repayment deduction under Section 80C, however, is available only on actual repayments.

Processing fee is tax deductible

Most taxpayers are unaware that charges related to their loan qualify for tax deduction.

As per law, these charges are considered as interest and therefore deduction on the same can be claimed.

“Under the Income Tax Act, Section 2(28a) defines the term interest as ‘interest payable in any manner in respect of any money borrowed or debt incurred (including a deposit, claim or other similar right or obligation)’.

” This includes any service fee or other charge in respect of the loan amount,” says Kumar. Moreover, there is a tribunal judgement which held that processing fee is linked to services rendered by the bank in relation to loan granted and is thus covered under service fee.

Therefore, it is eligible for deduction under Section 24 against income from house property .Other charges also come under this category but penal charges do not.

Principal repayment tax benefit is reversed if you sell before 5 years

You score negative tax points if you sell a house within five years from the date of purchase, or, five years from the date of taking the home loan.

“As per rules, any deduction claimed under Section 80C in respect to principal repayment of housing loan, would get reversed and added to your annual taxable income in the year in which the property is sold and you will be taxed at current rate,” says Archit Gupta, CEO, ClearTax.in.

Thankfully , the loan amortisation tables are such that the repayment schedule is interest heavy and the tax-reversal rule only apply to Section 80C.

Loans from relatives and friends is eligible for tax deduction

You can claim a deduction under Section 24 for interest repayment on loans taken from from anyone provided the purpose of the loan is purchase or construction of a property.

You can also claim deduction for money borrowed from individuals for reconstruction and repairs of property .

It does not have to be from a bank. “For tax purposes, the loan is not relevant, the usage is.

” The taxpayer should be able to satisfy the assessing officer how the loan has been utilised for constructing or purchasing a house property and completion of construction was within five years and other conditions are met,” says Gupta.

“The interest charged should be reasonable and a legal certificate of interest should be provided by the lender along with name, address and PAN,” says Gupta.

This rule, however, is only applicable for interest repayment.You will lose all tax benefits for principal repayment if you do not borrow from a scheduled bank or employer. The additional benefit of Rs 50,000 under Section 80EE is also not available.

You may not be eligible for tax break even if you are just a co-borrower

You cannot claim a tax break on a home loan even if you may be the one who is paying the EMI. For one, if your parents own a property for which you are paying the EMIs, you can’t claim breaks unless you co-own the property.

“You have to be both an owner and a borrower to claim benefits. If either of the titles are missing you are not eligible,” says Gupta. Even if you own a property with your spouse, you can’t claim deductions if your name’s not on the loan book as a co-borrower.

You can claim pre-construction period interest for up to 5 years

You know you can start claiming your home loan benefits once the construction is complete and you receive possession.

So, what happens to the installments you made during the construction or before you got the keys to the house? As per rules, you cannot claim principal repayment but interest paid during the period can be accrued and claimed post-possession.

‘The law provides a deferred deduction on the interest payable during pre-construction period. The deduction on such interest is available equally over a period of 5 years starting from the year of possession’, says Vaibhav Sankla, director, H&R Block.

Source: https://goo.gl/TJVT1y

ATM :: Are you eligible for 6.5% home loan subsidy?

Sukanya Kumar (more) Founder & Director, RetailLending.com | Source: Moneycontrol.com

Know all that is required to avail home loan subsidy offered by the government.

Government of India, on 17-Aug ’16 has announced a long-awaited scheme for the urban dwellers, under which a home loan interest subsidy of 6.5% has been announced which reduces burden from the home buyer. A welcome move!

Some pointers and some insights here on this Credit Linked Subsidy Scheme(CLSS):

FOR WHOM:

This subsidy is for economically weaker section (EWS) of people residing in urban areas which even include slum-dwellers. Annual household income should not exceed Rs 3 lakh. The marginalised sections of the society such as disabled, transgender, women, widow, scheduled caste and tribes will get priority. Lower income group(LIG) who has annual household income between Rs 3 and 6 lakh will be eligible.

Those who do not have any other home-ownership in his own or family’s name will qualify.

Your age should not be more than 70 years as on date.

FROM WHERE:

Besides public sector banks (PSU) and home finance companies (HFC), some co-operative banks and microfinance institutions are also extending this offer. The long list of lenders include HDFC, LIC Housing Finance, PNB Housing Finance, Dewan Housing, GIC, ICICI HFC, Tata Capital, L&T Housing Finance, Muthoot Finance, Yes Bank, Indiabulls, Axis Bank, DCB, Federal Bank and almost all PSU banks.

HOW MUCH:

Max subsidy is on a loan amount of Rs 6 Lakh for a maximum loan tenure of 15 years, at an interest of 6.5%. Hence, if the rate of interest by the lender is 10%, then the actual payable by the borrower under the subsidy scheme is 3.5%.

FOR WHAT PURPOSE:

The subsidy is allowed to borrowers buying a home either under-construction from a builder, a ready-to-occupy house, self-construction, or extension (adding new room, kitchen, bathroom etc.)

The maximum size should not exceed 30 sq. mt.(carpet) for EWS, and 60 sq. mt.(carpet) for LIG applicants.

AUTHORITY:

Currently, HUDCO and NHB has been identified by the Govt. as Central Nodal Agencies (CNAs) to tie up with lenders to extend this facility.

PROCESS:

An applicant will apply for a home loan in any of the lenders ( CLSS lender list ) where upon credit appraisal, the specific form supplied by the CNAs will be sent to HUDCO/NHB. They will come back with an approval after due verification and give their nod to the lending company. The disbursed loan will be adjusted with the subsidy, which, thankfully, the government is paying upfront.

Q&A:

Q: How much time will it take for HUDCO/NHB to approve the subsidy?

A: It is said that it will take 30-45 days time post all verifications done by the CNA to check the eligibility criteria.

Q: How much time will it take for the subsidy to arrive to the lender?

A: The lender does not have a clear answer to this. For them, it is just another loan. Once the subsidy is approved and received, they will act on it.

Q: What will happen if the purchase/construction area is more than the specified sq. mt.? Will the subsidy be declined?

A: It is okay to have a higher construction area or loan amount exceeding Rs 6 lakh. The balance area sq. mt. and the additional loan amount will not get the subsidy benefit. For example if your loan amount is Rs 6 Lakh, then the subsidy is on the whole and for a 15 year tenure at 6.5%, it is INR 2,20,187.05 (if the lender’s ROI is 10%). For a Rs 12 lakh loan amount, keeping the tenure and rate same, the subsidy amount will remain unchanged. Subsidy calculator here .

Q: Will there be one EMI for the subsidised as well as non-subsidised portion of the loan (in case of loan amount exceeding Rs 6 lakh) or it will be split?

A: It will not be split. The lender will consider this as one loan.

Q: When will the loan be disbursed? Will it have to wait till the subsidy confirmation comes in?

A: Lenders do not give one answer to this question. It is quite possible that they haven’t yet formed a firm decision over it. Some say they will hold on to the disbursement till the subsidy confirmation comes in, some say, they will disburse the loan anyways and they are just a facilitator and are not worried much as to when or whether it comes along.

Q: Will the builder / seller wait till subsidy confirmation for the borrower comes? Will the borrower be okay for the disbursement of loan without subsidy-confirmation?

A: A self-construction may wait, but a builder or a reseller to wait till the subsidy confirmation comes in, is going to be a long haul. Wonder how practical will it be.

Q: Govt. says the borrower should not be more than 70 years. Will the lenders comply?

A: Surely enough, the lenders I spoke with did not want to comply. They will stick to their own policy of the maximum age limit while doing a loan. So, if an applicant is 60, some may decline giving a loan to him or her.

Q: How will the subsidy get adjusted with the payable amount by the borrower?

A: The subsidy, as mentioned earlier, will come at one shot from government. The subsidy is basically to give relief to the borrower and instead of paying a monthly EMI of ‘X’ amount, he should pay lesser. However, the lenders are going to straightaway reduce the principal outstanding of the borrower by that Rs 2 lakh odd amount and adjust his tenure! So, his loan may now become a few years lesser, but monthly outflow remaining the same. A few borrowers who are educated and understand mortgage may, and I repeat may, seek an adjustment on the EMI and the lender will oblige. But how many borrowers in this category will actually know that this is an option too?

Q: Is this a real benefit to the borrower?

A: If the monthly outflow does not reduce while acquiring a home, then the benefit is definitely not looking attractive initially. Over the period of time, buy reduction of the tenure, it will bring joy to the borrower’s face, but the tough time is now. isn’t it?

Source: http://goo.gl/wFcIzU

NTH :: Soon, you may be able to dip into the NPS pot for a home loan

K. R. SRIVATS | NEW DELHI | AUGUST 22, 2016 | The Hindu Businessline

Discussion paper likely in a month, says PFRDA member

If you are a National Pension System subscriber, soon you may get to dip into the pot for a home loan and realise the dream of having ‘pension with a house’ on retirement.

The Pension Fund Regulatory & Development Authority (PFRDA) is toying with the idea of allowing NPS funds to be used to support home loan needs of subscribers, said RV Verma, Member, PFRDA.

The regulator feels an NPS subscriber should be allowed to use the NPS corpus either directly or as a collateral for financing the house. This will be an improvement over the current regime, where any premature withdrawal means diminishing of balance.

“We are preparing a discussion paper on ‘Housing for NPS Subscribers’. Rather than allowing NPS contributions to flow into the capital market or specified securities, the same could also be used for supporting home loan needs of NPS subscribers. This discussion paper is expected to be ready in a month,” Verma told told BusinessLine here.

Any move to allow pension funds to be used for financing a home is expected to “reduce homelessness” in the country and is in line with the government’s objective of ‘Housing for All by 2022’. This facility will be available across the entire NPS subscriber universe — both government employees and non-government individual subscribers.

A win-win

This idea of allowing NPS monies to fund home purchase could be a win-win for the government and subscribers. Besides pension and a house, subscribers will get fiscal benefits by way of tax breaks for contributing to the NPS corpus and also for repayment of housing loan principal and interest.

For the government, the benefit comes in terms of reduced allocation from the fisc towards house building advance, Verma said.

As on date, an NPS subscriber is allowed partial withdrawal — capped at 25 per cent of the contribution if he has been with the scheme for at least 10 years.

Source: http://goo.gl/6aGZzV

NTH :: TCHFL unveils low interest home loan at 4% for weaker section

Aug 02, 2016, 10.22 AM | Source: PTI | MoneyControl.com

“By providing home loans at subsidised interest rates from 4 percent, TCHFL will help individuals to realise their dream of buying their own home,” the company said in a release.

Tata Capital Housing Finance (TCHFL) announced a new home loan scheme ‘Prapti’ targeted at low income group under the affordable housing plan.

“By providing home loans at subsidised interest rates from 4 percent, TCHFL will help individuals to realise their dream of buying their own home,” the company said in a release.

Tata Capital said ‘Prapti’ is a step towards government’s Pradhan Mantri Awas Yojana envisaging to provide affordable houses to the urban poor by 2022.

The scheme specifically caters to segments like the lower income group (LIG), economically weaker section (EWS) of society, Scheduled Caste (SC), Scheduled Tribe (ST) and women residing in the peripheries of metros, tier I, II and III cities.

The scheme is applicable for households with an income of up to Rs 6 lakh per annum, the company said.

“Housing Finance is an integral part of Tata Capital’s wide portfolio of retail offerings. This product can reduce the effective cost of interest thereby expanding the opportunity of home ownership,” said Govind Sankaranarayanan, Chief Operating Officer-Retail Business & Housing Finance, Tata Capital.

The ‘Prapti’ home loan scheme, with low interest rates and flexible loan repayment options will equip a larger base of the lower income segment to realize their dream of purchasing their own home, TCHFL Managing Director R Vaithianathan said.

TCHFL, a wholly-owned subsidiary of Tata Capital, provides loans for purchase and construction of residential unit, land purchase, home improvement, home extension and project finance to developers.

Tata Capital is into consumer finance, advisory services, commercial and infrastructure finance, securities, investment banking, private equity advisory, credit cards and travel & forex services.

Source: http://goo.gl/usyGLF

NTH :: Underwriting norms need to improve for cheap home loans

Indian Housing Finance Companies (HFCs) need to work on underwriting standards for affordable home loans to control credit risks, according to Moody’s

Abhijit Lele | Mumbai | July 26, 2016 Last Updated at 00:21 IST | Business Standard

Indian Housing Finance Companies (HFCs) need to work on underwriting standards for affordable home loans to control credit risks, according to Moody’s. The observation becomes crucial, at a time when the government is pushing for an increase in home ownership among underprivileged groups.

Affordable housing loans — which are mortgages for low-income earners — are typically opted for by first-time home buyers, usually self-employed in small unregistered enterprises or working for small companies. Key credit considerations for HFCs while giving such loans include income assessments.

Some HFCs prefer to extend loans to the specific building projects of construction firms that they have pre-approved, Moody’s said.

The affordable housing loan market is forecast to grow to Rs 8 lakh crore by 2022 from Rs 59,300 crore in March 2015, bolstered by government measures. Affordable housing loans accounted for 14 per cent of the total home loan books of HFCs as on 31 March 2015. “This segment presents unique credit risks for lenders, and when securitised, for residential mortgage-backed securities because of the nature of the borrowers,” said Georgina Lee, assistant vice-president at Moody’s.

Many borrowers do not have previous banking transaction records and, for the self-employed, they do not disclose their incomes or file tax returns.

As such, the formal documentation or records needed to verify income and the ability to service loans is absent, similar in some ways to “low-doc” mortgage loans in other jurisdictions.

Source : http://goo.gl/kknWaV

ATM :: DSK’s zero interest home loan offer: Are real estate developers innovating products or rolling out gimmicks?

by Dinesh Unnikrishnan | Jan 4, 2016 08:51 IST | First Post

Real estate developers are known for various marketing tricks to attract buyers. Some offer free cars with luxury apartments, some air-conditioners, gold coins, while a few offer discounts to market rates.

But, one recent advertisement by the Pune-based DSK Group, for their select projects in Pune and Mumbai, instantly caught the attention of both prospective home buyers and competition. The DSK scheme, announced in a tie up with Tata Capital, offered flats for customers with a loan facility from the financier at almost zero rate of interest.

Under the scheme, the buyer of a one bedroom flat can finish the repayment of his Rs 50.7 lakh loan flat in eight years. He needs to just pay the initial contribution of Rs 10.04 lakh (20 percent of property cost) and repay the rest in equated monthly installments (EMIs) of Rs 40,160, while DSK has promised to pay the interest component to Tata Capital on behalf of the customer. In other words, the customer needs to pay only the principal value of the property to own his flat.

For a home loan aspirant, the scheme should be appealing. If the same loan is taken for 20 years under a regular plan, say at an interest rate of 9.5 percent at an EMI of Rs 37,710 for 20 years, the customer ends up paying almost the double value of property taking into account the interest burden on him. In the DSK offer, the customer is practically paying only the flat cost, with almost same EMI amount.

The question here is does this mark the beginning of a trend-setting, innovative housing offer in the Indian home loan market or is it just a gimmick?

DSK scheme

According to a section of real estate analysts, the whole idea behind the DSK scheme is to avail quick, cheaper liquidity to develop their projects. Typically developers get loans from commercial banks at a higher rate of 13-14 percent, while individual buyers get loans at about 9-10 percent.

“It’s a win-win situation for the developer and the buyer. For the developer, it is an easy way to mobilize cheaper funds. For the buyer too, the scheme makes sense since he doesn’t need to bear the interest cost,” said the analyst with a Mumbai-based brokerage, who didn’t want to be named.

But not all share this opinion. Senior banking industry officials are critical of the scheme saying there is an unseen risk involved in this scheme for the customer. “In case the builder defaults on the interest payment at any stage, the customer will have to bear an unexpected financial burden. This is a risk for the consumer,” said Pratip Chaudhury, former chairman of State Bank of India.