Tagged: LTCG

Interview :: Worst over for the market, top 10 stocks to bet on in FY19

Interview with Gaurav Jain, Director at Hem Securities.

Uttaresh Venkateshwaran, Sunil Matkar | Apr 06, 2018 03:19 PM IST | Source: Moneycontrol.com

While the market may have fallen around 10 percent from its peak, experts such as Gaurav Jain, Director, Hem Securities believe that the worst may be over now.

“In the next quarter, the market should settle and then a pullback is likely,” Jain told Moneycontrol’s Uttaresh Venkateshwaran & Sunil Shankar Matkar. He expects largecaps to move ahead and midcaps will play catch-up.

He expects a broad-based pick up in the market going ahead. “In the past few days, a few stocks have risen, which have pushed the market. We should start seeing a pick-up in many more stocks. Essentially, people are not in a panic stage, while retail investors have looked to book profits and are not in a hurry to invest,” Jain further added. Edited excerpts:

The market has been trading off the previous high points. What is the outlook for D-Street going ahead?

Over the last quarter, we saw events such as the Union Budget, which introduced taxes on long term capital gains (LTCG). Global markets reacted negatively, while big IPOs also sucked liquidity from the market, among other factors. As such, the market had a good run up in the past two three quarters.

In the next quarter, the market should settle and then there could be a pullback. Next quarter should be of accumulation and positive movement.

So, what kind of returns are you expecting from this market?

We are in an election year. So, the market could behave differently with results coming on. Overall, for FY18 we are looking at 8-10 percent returns.

What can be seen as triggers for this market?

Firstly, many companies’ results were affected in one quarter on the back of Goods and Services Tax (GST). With new GST Bill coming in full flow, it should give positive flow for most sectors. Even as the e-way bill is introduced, some companies could face some issues at the start and then gradually get comfortable with it.

Secondly, look at growth visibility in the Sensex and Nifty. Several managements are hinting at positive cues. Earnings could improve and several companies have done their expansions on their side.

Lastly, we have to wait for how monsoon pans out. So, overall there is positive momentum and investors are quite bullish on India even at this point.

Does that mean we could go back to the record high levels?

Probably…

What are you hearing on private capex plans? Are they willing to spend on that front as well?

Most companies, the big ones especially, have done their share of capital expenditure. One important reason why this is happening is due to change in technology that is erupting. For instance, look at telecom sector. In case Reliance Jio comes up with a new technology, rivals also tend to counter those. In case of textiles, many things have happened and firms are adding up more technology and machines. With changing technology, fast-growing companies need to adapt to it and they are deploying resources in those areas.

Could you throw some light on the state of midcaps? How do you expect them to perform going forward?

Largecaps should start moving first, going forward, followed by midcaps. Investors currently are playing conservative as they saw their stocks bleeding all through the last quarter. Hence, the money is going into largecaps right now.

But what about valuations for several segments in the market…how did the IPO market perform in FY18?

Look at the number of IPOs that came up with multiples of 30 and 40 times. Fund managers that we spoke to are talking about large systematic investment plans (SIPs) that have to be deployed into such stocks and that is probably why such high multiples were seen.

In FY17, we saw around 37 IPOs hitting the market and this figure could be higher this fiscal, looking at the prospectuses filed and information available from merchant bankers. Also, IPO sizes are a lot larger now.

But will investors have the appetite going forward?

Institutional investors will have it. They will always look at beaten down stocks and they also do not have issues with funds.

Currently, retail investors are investing less. If they have Rs 100 with them, they are looking to invest Rs 20 right now. In fact, many retail investors have booked profits in the past quarter.

Is there much downside from the current market levels?

I don’t think so. The worst should already be over. In the past few days, a few stocks have risen, which have pushed the market. We should start seeing a pick-up in many more stocks. Essentially, people are not in a panic stage, while retail investors have looked to book profits and are not in a hurry to invest.

So, what will your advice be to a 35-40-year old investor?

They must invest in mutual funds. But you could also do it making money by directly investing in equity markets as well.

What sectors are you looking at currently?

We expect pharmaceuticals to perform, while it could be a challenge in case of information technology names.

You can look at infrastructure sector as well. These companies are flooded with orders.

On banks, it is clearly not the case that all PSU banks are bad. Right now, people are not trusting PSU banks and private banks are usually considered more transparent.

It is a play on perception and that could be seen in cases of a recent listing such as Bandhan Bank. The IPO came at a very good multiple and still listed at good returns. These are companies with professional management which are growing along with having fast execution and chasing for business. As such, we were seeing a shift to private sector banks, but currently investors also do not know about hidden concerns in PSU banks too.

LTCG tax on equities has become a reality now. Are you getting queries about it and what are you telling them?

I think the sentiment around it has been already digested in the market. People are taking in the transition in stock market. I feel that this is not an issue at this point.

How much of a risk is political scenario for the market?

The market tends to be very volatile on political instability. As soon as there are chances of dent to existing government, it starts reacting. The question is not about which government, but about a stable one. This is important from a foreign investor perspective. These would have regular impact but not larger level…the market will make a comeback once the elections are over.

As we move into end of this year (and closer to general elections), investors may hold for couple of months to understand what is happening (on the political front).

On the global front, any statement from the US with respect to protection of its own trade boundaries is a major risk for the market.

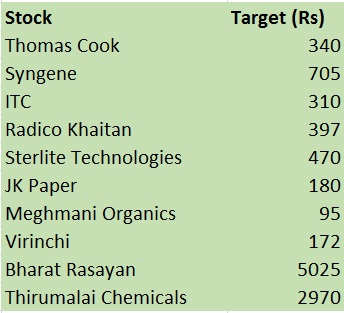

Lastly, what are your top stock picks for FY19?

Disclosure: Reliance Industries Ltd. is the sole beneficiary of Independent Media Trust which controls Network18 Media & Investments Ltd.

Interviews :: Alpha generation in large-cap funds would compress going ahead

Mahesh Patil, Co-CIO, Aditya Birla Sun Life AMC on how he is creating alpha in the large cap space, his contra calls and more.

By Morningstar Analysts | 27-12-17 |

The asset size of Aditya Birla Sun Life Frontline Equity Fund has crossed Rs 20,000 crore. Do you see size posing an issue to manage this fund going forward?

We maintain a good diversification in this fund by having exposure across sectors. We aim to beat the benchmark consistently and incrementally rather than taking very large sectoral bets. Given that the fund invests at least 80% of its assets in large cap stocks, we don’t see size posing as a challenge. Besides, the core of the portfolio has very long term holdings. That said, as the fund size increases it becomes slightly more difficult to build or unwind positions in stocks and needs more effort. But it is part of the process and does not affect the performance significantly.

We have a large number of stocks (60-70) in the portfolio as compared to other similar funds in the industry. Before deciding the quantum of exposure warranted in any stock, we take a close look at the liquidity of the stocks. This strategy allows us to manage large size.

It is becoming difficult for managers to generate alpha in the large cap space. How do you overcome this challenge?

We are seeing a huge rally in the mid and small cap stocks and large cap funds obviously can’t take exposure to such stocks. So multi-cap funds have been able to generate decent alpha by maneuvering where the opportunities are.

As markets mature and price discovery happens across stocks its going to become difficult to generate alpha in large caps. The alpha generation which we saw in the last three to four years would compress going ahead. This is because the alpha was high as compared to the historical average, especially during calendar year 2014-16.

We never target to generate superlative alpha in large cap funds. Instead, we endeavor to find some new stock ideas every year which keeps the portfolio fresh. If there is a serious underperformance, we are nimble enough to take corrective action. While everything is fairly priced in the market at this juncture, we try to continuously look out for undervalued companies. Some amount of contrarian investing and moving away from the crowd helps to spot early turning points in stocks/sectors. Similarly, we maintain a discipline to trim exposure in certain stocks that have overshot their valuation target. This strategy enables us to buy stocks which are relatively cheap in terms of valuation. So some amount of active management is also required at this juncture to generate alpha in the large cap space.

In which sectors/themes are you deploying the steady inflows coming in equity and balanced funds?

We have been overweight on banking and financial services. Financial services sector has had a good run and the valuations have moved up. Hence we are more discrete now in choosing the right segments that offer better growth. While we prefer private retail banks, we are slowly warming up to corporate banks because of some clarity emerging on resolutions of bad debts and a cyclical recovery in economy.

Besides, we are positive on consumer discretionary space. We are seeing a higher demand for discretionary consumption as the per capita income is moving up in India. Further, the implementation of GST will benefit players in the building material, consumer durables and retail space. Rural consumption is also starting to improve with normal monsoons and government focus on stepping up rural spending.

We are fairly overweight on metals. Metal prices are steady as China is cutting down capacity on the back of environmental issues which is supporting price. Indian companies are also deleveraging which will increase their equity value.

Another sector where we are taking a contrarian call is telecom. We are seeing consolidation happening faster than we expected in this sector. While there is still some pain for a few quarters, over a three-year time frame it could be a good time to look at some leading telecom companies.

We are selective in the infrastructure space. Road, railways and urban transport are some pockets where there is significant traction. Companies positioned in this sector are expected to see good increase in their order books.

Post SEBI’s diktat on scheme categorization, how are you restructuring your funds? Are you planning to merge smaller schemes?

Fortunately, we have been working on consolidating schemes much before the SEBI circular came out. Most of our equity funds are aligned as per SEBI categorization. We would look to merge some thematic funds.

Overseas fund of funds category is seeing continuous outflows. What are the reasons for the waning demand for this category.

The awareness level about this category is low. Domestic market has been doing well so people are preferring to invest in India. Overseas fund of funds have done well though.

As markets mature and you see enough ownership of domestic funds, people would look to invest outside India. There are a lot of new generation companies which investors can take exposure through these funds.

Though taxation of this category is an issue, you need to realize that if you are making good returns it should not be a problem. HNIs who already have a high exposure to India can look at these funds. Also, those wish to send their children overseas for education can consider these funds because the underlying returns are dollar based. To some extent, you are taking the currency hedge through these funds.

When do you see private-sector investment picking up?

Private sector investment has been elusive. But there are a couple of factors which indicate that investment will pick up one year down the line. Firstly, capacity utilization has bottomed out and is showing early signs of improving. Secondly, while a lot of large corporates in metals and infra space are saddled with high debt were are seeing the deleveraging cycle has started for some companies. Corporate debt to GDP which peaked out in 2016 is starting to come off. Finally, bank recapitalization would enable corporates to re-leverage and begin the next capex cycle. Sectors like Steel, Oil and Gas, fertilizer and auto are the first to see a revival.

During every budget we get to hear about suggestions to reinstate long-term capital gains (LTCG) tax on equity investments. Some say that exemption of LTCGT can lead to market manipulation. What are your views? If the government introduces LTCGT what would be the impact on markets?

The exemption of LTCGT has helped attract investors in equities. But that’s not the only reason why people invest in equities. They invest because they expect better returns. If there is money to be made in markets, I don’t think it would deter investors from this asset class. So introduction of LTCGT would not have an impact on long term investors. However, it could hurt the sentiments in the short run. We could see some curb in short term speculative money moving in stocks having weak fundamentals.

How has your investment philosophy evolved over the years?

While our broad philosophy has remained the same, we have started giving more attention to management quality while evaluating companies. Our time horizon of owning stocks has also increased and we are evaluating companies with a three-year perspective. There is a larger focus on how companies are generating free cash flows and how it is being utilized. These factors impact the PE multiples. So we are willing to pay a premium if these factors are favorable. To sum up, we have been incorporating these factors in our philosophy.

Your favorite book

One book which I found interesting is ‘Good to Great’ authored by Jim Collins. The book gives good insights into building an organization and focuses on what really matters to not only to survive and endure but to excel.

Source: https://goo.gl/i9ro1V

ATM :: Home loan interest is tax exempt after construction is over

There is no specific requirement to disclose the fact in the ITR form

Parizad Sirwalla | Wed, Oct 01 2014. 06 39 PM IST | LiveMint.com

I have come to know that one can take exemption for interest paid on second home loan only after the construction is over and the benefit is available in five instalments starting the year when the construction is complete. During the period when the house is under construction, do we have to mention the amount of interest anywhere (Schedule CFL) in the income tax return (ITR) form? I am filing ITR 2. —Amit

Yes, your understanding is correct. The deduction towards interest paid on housing loan taken against an under-construction property can be availed only from the year in which the construction of the property is completed.

There is no specific requirement to disclose the fact in the ITR form that you are paying the interest on housing loan availed against the under-construction property.

I purchased an apartment in Gurgaon four years back and now plan to sell it. Will the sale proceeds attract short-term capital gains or long-term capital gains (LTCG)? Are there re-investment options to save tax? —Aravind Narayanam

The capital gains, if any, arising from sale of a residential property held for more than 36 months from the date of acquisition shall be termed as LTCG.

The aforesaid LTCG can be claimed as exempt from tax by re-investing in one new residential property in India within the specified time frames (i.e. within one year prior to sale date or two years from the sale date or within three years for an under-construction property) as per section 54.

Alternatively, the LTCG can be invested in specified bonds issued by the National Highways Authority of India or Rural Electric Corp. Ltd under section 54EC within a period of six months from the date of sale of property subject to the cap of Rs.50 lakh subject to specified conditions.

The investment in a new property or specified bonds has a lock-in period of three years. Accordingly, if the new property is sold or the bonds are converted into cash within a period of three years, the exemption shall be revoked. If you take any loan or advance against the security of the said bonds, the same shall be deemed to be converted into cash.

The amount invested in a residential property or specified bonds shall be claimed as exempt from tax and the balance amount, if any, shall be taxable at a flat rate of 20.6% (including education cess). Further, if your taxable income during the financial year 2014-15 exceeds Rs.1 crore, you will be liable to pay surcharge at 10% on the basic tax rate.

While calculating LTCG, the cost of acquisition and improvement has to be adjusted by applying the cost inflation index notified by the tax authorities in the year of purchase and sale, respectively.

Source : http://goo.gl/bZnrWs