Tagged: SBI Max Gain

ATM :: 7 home loan repayment options to choose from

By Sunil Dhawan | ET Online | Updated: May 05, 2018, 12.32 PM IST | Economic Times

Buying that dream home can be rather tedious process that involves a lot of research and running around.

First of all you will have to visit several builders across various locations around the city to zero in on a house you want to buy. After that comes the time to finance the purchase of your house, for which you will most probably borrow a portion of the total cost from a lender like a bank or a home finance company.

However, scouting for a home loan is generally not a well thought-out process and most of us will typically consider the home loan interest rate, processing fees, and the documentary trail that will get us the required financing with minimum effort. There is one more important factor you should consider while taking a home loan and that is the type of loan. There are different options that come with various repayment options.

Other than the plain vanilla home loan scheme, here are a few other repayment options you can consider.

I. Home loan with delayed start of EMI payments

Banks like the State Bank of India (SBI) offer this option to its home loan borrowers where the payment of equated monthly instalments (EMIs) begins at a later date. SBI’s Flexipay home loan comes with an option to go for a moratorium period (time during the loan term when the borrower is not required to make any repayment) of anywhere between 36 months and 60 months during which the borrower need not pay any EMI but only the pre-EMI interest is to be paid. Once the moratorium period ends, the EMI begins and will be increased during the subsequent years at a pre- agreed rate.

Compared to a normal home loan, in this loan one can also get a higher loan amount of up to 20 percent. This kind of loan is available only to salaried and working professionals aged between 21 years and 45 years.

Watch outs: Although initially the burden is lower, servicing an increasing EMI in the later years, especially during middle age or nearing retirement, requires a highly secure job along with decent annual increments. Therefore, you should carefully opt for such a repayment option only if there’s a need as the major portion of the EMI in the initial years represents the interest.

II. Home loan by linking idle savings in bank account

Few home loan offers such as SBI Maxgain, ICICI Bank’s home loan ‘Overdraft Facility’ and IDBI Bank’s ‘Home Loan Interest Saver’ allows you to link your home loan account with your current account that is opened along with. The interest liability of your home loan comes down to the extent of surplus funds parked in the current account. You will be allowed to withdraw or deposit funds from the current account as and when required. The interest rate on the home loan will be calculated on the outstanding balance of loan minus balance in the current account.

For example, on a Rs 50 lakh loan at 8.5 percent interest rate for 20 years, with a monthly take home income of say Rs 1.5 lakh, the total interest outgo for a plain vanilla loan is about Rs 54,13,875. Whereas, for a loan linked to your bank account, it will be about Rs 52,61,242, translating into a savings of about Rs 1.53 lakh during the tenure of the loan.

Watch outs: Although the interest burden gets reduced considerably, banks will ask you to pay that extra interest rate for such loans, which translates into higher EMIs.

III. Home loan with increasing EMIs

If one is looking for a home loan in which the EMI keeps increasing after the initial few years, then you can consider something like the Housing Development Finance Corporation’s (HDFC) Step Up Repayment Facility (SURF) or ICICI Bank’s Step Up Home Loans.

In such loans, you can avail a higher loan amount and pay lower EMIs in the initial years. Subsequently, the repayment is accelerated proportionately with the assumed increase in your income. There is no moratorium period in this loan and the actual EMI begins from the first day. Paying increasing EMI helps in reducing the interest burden as the loan gets closed earlier.

Watch outs: The repayment schedule is linked to the expected growth in one’s income. If the salary increase falters in the years ahead, the repayment may become difficult.

IV. Home loan with decreasing EMIs

HDFC’s Flexible Loan Installments Plan (FLIP) is one such plan in which the loan is structured in a way that the EMI is higher during the initial years and subsequently decreases in the later years.

Watch outs: Interest portion in EMI is as it is higher in the initial years. Higher EMI means more interest outgo in the initial years. Have a prepayment plan ready to clear the loan as early as possible once the EMI starts decreasing.

V. Home loan with lump sum payment in under-construction property

If you purchase an under construction property, you are generally required to service only the interest on the loan amount drawn till the final disbursement and pay the EMIs thereafter. In case you wish to start principal repayment immediately, you can opt to start paying EMIs on the cumulative amounts disbursed. The amount paid will be first adjusted for interest and the balance will go towards principal repayment. HDFC’s Tranche Based EMI plan is one such offering.

For example, on a Rs 50 lakh loan, if the EMI is xx, by starting to pay the EMI, the total outstanding will stand reduced to about Rs 36 lakh by the time the property gets completed after 36 months. The new EMI will be lower than what you had paid over previous 36 months.

Watch outs: There is no tax benefit on principal paid during the construction period. However, interest paid gets the tax benefit post occupancy of the home.

VI. Home loan with longer repayment tenure

ICICI Bank’s home loan product called ‘Extraa Home Loans’ allows borrowers to enhance their loan eligibility amount up to 20 per cent and also provide an option to extend the repayment period up to 67 years of age (as against normal retirement age) and are for loans up to Rs 75 lakh.

These are the three variants of ‘Extraa’.

a) For middle aged, salaried customers: This variant is suitable for salaried borrowers up to 48 years of age. While in a regular home loan, the borrowers will get a repayment schedule till their age of retirement, with this facility they can extend their loan tenure till 65 years of age.

b) For young, salaried customers: The salaried borrowers up to 37 years of age are eligible to avail a 30 year home loan with repayment tenure till 67 years of age.

c) Self-employed or freelancers : There are many self-employed customers who earn higher income in some months of the year, given the seasonality of the business they are in. This variant will take the borrower’s higher seasonal income into account while sanctioning those loans.

Watch outs: The enhancement of loan limit and the extension of age come at a cost. The bank will charge a fee of 1-2 per cent of total loan amount as the loan guarantee is provided by India Mortgage Guarantee Corporation (IMGC). The risk of enhanced limit and of increasing the tenure essentially is taken over by IMGC.

VII. Home loan with waiver of EMI

Axis Bank offers a repayment option called ‘Fast Forward Home Loans’ where 12 EMIs can be waived off if all other instalments have been paid regularly. Here. six months EMIs are waived on completion of 10 years, and another 6 months on completion of 15 years from the first disbursement. The interest rate is the same as that for a normal loan but the loan tenure has to be 20 years in this scheme. The minimum loan amount is fixed at Rs 30 lakh.

The bank also offers ‘Shubh Aarambh Home Loan’ with a maximum loan amount of Rs 30 lakh, in which 12 EMIs are waived off at no extra cost on regular payment of EMIs – 4 EMIs waived off at the end of the 4th, 8th and 12th year. The interest rate is the same as normal loan but the loan tenure has to be 20 years in this loan scheme.

Watch outs: Keep a tab on any specific conditions and the processing fee and see if it’s in line with other lenders. Keep a prepayment plan ready and try to finish the loan as early as possible.

Nature of home loans

Effective from April 1, 2016, all loans including home loans are linked to a bank’s marginal cost-based lending rate (MCLR). Someone looking to get a home loan should keep in mind that MCLR is only one part of the story. As a home loan borrower, there are three other important factors you need to evaluate when choosing a bank to take the loan from – interest rate on the loan, the markup, and the reset period.

What you should do

It’s better to opt for a plain-vanilla home loan as they don’t come with any strings attached. However, if you are facing a specific financial situation that may require a different approach, then you could consider any of the above variants. Sit with your banker, discuss your financial position, make a reasonable forecast of income over the next few years and decide on the loan type. Don’t forget to look at the total interest burden over the loan tenure. Whichever loan you finally decide on, make sure you have a plan to repay the entire outstanding amount as early as possible. After all, a home with 100 per cent of your own equity is a place you can call your own.

Source: https://bit.ly/2wjnSId

ATM :: SBI MaxGain Home Loan Review – With FAQ’s

By Ashal Jauhari | 14th April 2013 | AsanIdeasforWealth.com

In this article we are going to share SBI Maxgain Home Loan review with you. Now a days many home loan borrowers are opting a particular type of home loan from State Bank of India which is called Max Gain because it has many advantages compared to other kind of home loan scheme’s. In this SBI Max Gain home loan, an Overdraft (OD) account is assigned to the customer’s home loan & any amount parked by customer is treated as loan repayment for the purpose of interest calculation, for the days, the amount stays there in that OD account. As on date following banks are offering similar types of home loan to their customers SBI, IDBI, CITI, HSBC & Standard Chartered. Punjab National Bank can also be added in this list but it’s offering a combo of normal loan + Overdraft. In this article, we are going to discuss only SBI Max Gain as in OD linked home loan, the maximum business is with SBI & the most discussed topic on Jagoinvestor Forum is also related to SBI Max Gain Scheme

What is an Overdraft account?

Before we discuss Max Gain, first understand, what is an Over Draft Account? All of us are well aware of functioning of an ordinary saving bank (SB) account. Here account operates between zero to positive & positive to zero. As we deposit our money, it’s used by bank & we get interest on our money from bank. In case of an OD account, bank first ask for a security & then assign a credit limit on the basis of the market value of that security. This security may be Fixed Deposits, Insurance Policies, National Saving Certificates, Shares, Mutual Fund units, house/commercial property etc. Now when we are using this assigned credit limit, the amount is going from zero to negative zone & when we are repaying, it’s coming from negative to zero. As we are using bank’s money in this case, the interest ‘ll be paid by us to bank. That’s how an OD account works.

So what is the correlation between Max Gain home loan & Over Draft account?

For Max Gain borrowers, State bank of India opens an Over Draft account where the Credit limit as discussed above is equal to the loan value assigned to the borrower. Here underlying security is the home you have purchased or constructed from that loan amount. Now as & when you are parking any surplus amount into this OD account, the parked amount is treated as payment towards loan (effectively you are bringing down your loan liability from negative towards zero position) and thus the interest ‘ll be charged only on the difference amount i.e. total loan amount – parked surplus amount.

What is the primary benefit of SBI Max Gain Scheme?

Well the primary benefit of MG is to keep your liquidity intact & still bringing down your interest outgo. To understand it better, please imagine a situation you are running a home loan of 30L Rs. & now you do have 2L Rs. with you to prepay. In normal home loan, your 2L Rs. ‘ll be accepted by bank & adjusted towards home loan & your amount is gone forever so no liquidity for you of that 2L Rs. amount. On the other hand, if you are MG customer, simply park those 2L Rs. in your MG account & your interest outgo ‘ll be lower from that month itself till those 2L Rs. or a part of it is there as surplus in MG account.

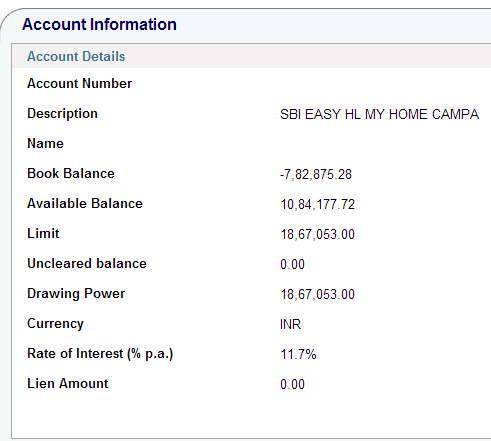

What is Drawing Power ?

Drawing Power is nothing but your as on date actual outstanding loan amount. Before final disbursal or start of loan repayment, it’s your sanctioned loan amount. Once your EMI starts, it’s your as on date actual outstanding loan amount. Please check Image below, Drawing Power here is 1867053 Rs. as on date.

What is Available balance?

Before final disbursal, it’s the sum of undisbursed amount + parked surplus & post final disbursal, it’s your parked surplus amount which is available to withdraw. Please check Image below, Available Balance here is 1084177.72 Rs. as on date.

What is book balance?

It’s the adjusted loan amount arrived after deducting the Available Balance amount from Drawing Power. In your account statements it’s shown with a negative sign. Please check Image below, Book Balance here is – 782875.28 Rs. as on date.

Is there any extra interest for Max Gain?

No, the interest for home loan is same in SBI be it for normal home loan or for Max Gain.

I’m an existing SBI home loan customer. Can I convert my old term loan to Max Gain?

Yes, you can. Please contact your loan serving branch or RACPC for the required paperwork to be done. This may be an outdated info so please do check with your loan serving branch for current day rules on conversion.

I have taken the Max Gain for an Under Construction Property. Can I park surplus amount to save on interest outgo?

The answer is yes & no both. Yes you can park your surplus during under construction phase but do remember SBI is disbursing partially at this juncture & in case due to any emergency you want to liquidate your surplus, SBI ‘l not allow the same. so park only that much surplus, you feel you ‘ll not need even in an extreme emergency.

If I’m parking some money on monthly basis or in lump sum, will my loan term come down or EMI go down?

No. Neither your EMI ‘ll come down nor your loan term. The only saving is in terms of interest outgo. To understand it better, Let’s assume a test case of loan amount 30L Rs. @ 10% Rate of Interest for 20Y term. The normal EMI for these nos. ‘ll be 28951 Rs. The break up of your EMI for first month ‘ll be 25000 Rs. interest & 3951 Rs. for principal repayment.

Now if you do have 2L Rs. surplus in the very first month & prepay the same as below –

Case – 1 Normal home loan

Your 2L Rs. is gone & outstanding loan amount ‘ll come to 2796049 & interest outgo ‘ll still be 25000 Rs. but the no. of months ‘ll come down from original 240 to 198 months.

Case – 2 Max Gain home loan

Your 2L Rs. are parked in that OD account & the interest for the very first month ‘ll be calculated on 28L Rs. & thus it ‘ll be 23334 & thus there‘ll be an interest saving of 1667 Rs. which‘ll remain available in your OD account as surplus along with your parked surplus 2L Rs. so for next month, the parked surplus amount ‘ll be 201667 Rs.

Please do note in case 2 above, Your loan term is still 240 months but the saving of interest ‘ll keep on increasing on mly basis from the parked surplus & of course the liquidity of those 2L Rs. is there.

How can I calculate my saving in Max Gain?

To know your actual saving, first of all please demand a loan amortization schedule from your loan serving branch & now for each month compare the scheduled interest outgo as per your loan amount. schedule & the actual interest outgo.

What should I do to maximize the savings in Max Gain?

If you are paying your EMIs from SBI’s SB account, you can maximize your benefits. How? here it goes. Say 15th is the EMi date on which EMi amount is debited from your SB acct. Now in a normal home loan, people ‘ll keep at least 2-3 months’ EMI amount as buffer in SB account. but in case of Max Gain, you do not need to keep buffer in SB account. Keep this buffer amount also in your MG account along with your routine surplus amount. now use the power of net-banking of SBI for your own good & create a schedule transaction of your EMI amount 28951 Rs. (in the above example) to be transferred on 13th of every month from MG account to SB account. At a time you can schedule for next 12 months by using standard instruction. So it’s technology that’s helping you.

I can transfer to MG account from my existing net-banking enabled SB account but reverse is not happening. why?

The answer lies in the fact that Net-banking transaction rights on your MG account is not enabled yet by your loan serving branch. if final disbursal is done, you can apply for transaction rights. if only partial disbursement has been done, sorry, you can’t apply for transaction rights till final disbursal.

Is it mandatory to purchase property insurance & life insurance along with Max Gain?

Having property insurance as well as sufficient life insurance is compulsory but purchasing the same from SBI’s sister cos. like SBI General ins. & SBI Life Ins. is not at all mandatory. if you feel that policies are being cross sold to you to exploit your position (home loan seeker), please contact the AGM of your local RACPC where your loan application is under processing.

Is SBI charging higher processing fee for Max Gain?

No, as on date there is no differentiation in fee for term loan & Max Gain but SBi reserves the rights to charge different fee.

Can I claim section 80C principal repayment benefit for the surplus amount parked in Max Gain?

The answer is NO. Only the regular principal repaid by you from your EMI as part of your loan amortization schedule is available for tax benefit under section 80C. the parked surplus amount is liquid money & you can withdraw it any time, hence it’s not considered as actual repayment of loan & thus not eligible for tax benefit.

Can I avail cheque book & ATM card for my Max Gain account?

Yes, as & when you‘ll demand these, SBI ‘ll offer you the same. In case you are already holding an SBI SB acct. linked ATM card, you have the option to link your MG acct. also with this existing ATM card.

Can I enroll my MF SIPs in Max Gain?

Yes but do note, there should be a surplus balance i.e. available balance on the date of SIP, else your ECS or SI mandate ‘ll bounce.

Can i pay for my utility bills, credit card payments, online shopping from Max Gain?

Yes, you can do all this & more. In fact it’s in your best interest that you treat your MG account as your primary money parking account & route all your transactions through it so that money is lying there for maximum possible time & thus helping you to bring down your interest outgo.

I used my MG account ATM card to withdraw cash from other bank’s ATM & I was charged the money very first time in the month. Why?

The reason is, as per RBI’s circular 5 transactions on other banks’ ATM are free only for SB account & in this case, you forget the point that your MG account is not SB account. it’s an overdraft account.

For an imaginary situation, my loan amount is 30L Rs. & parked surplus amount is also 30L Rs. Does it mean, my loan is closed & I can claim my property papers from SBI?

No, your loan is not closed. Only interest outgo ‘ll become zero & EMi ‘ll remain continue as it is. Yes the interest part of your EMI ‘ll keep on accumulating in your MG account. If you want to close your loan at this point, you w’d have to inform SBI in written & now SBI ‘ll adjust your parked surplus amount towards the outstanding loan amount. you ‘ll lose the liquidity of your money but loan ‘ll be over & now you can get your property papers back.

How can I transfer my loan from other banks to SBI Max Gain?

For loan transfer, first of all contact your existing lender & ask for following things.

1. Loan Account statement from day one.

2. List of Documents, which were submitted by you at the time of availing original loan. In day to day language of bankers, it’s called LOD.

3. As on date outstanding loan balance with applicable interest, penalty & any other fee to close the loan.

Now contact, the nearest SBI Branch (if you do have an existing SB account with SBI, it’s advisable to contact there for ease of operation). Inform in that branch that you want to transfer your loan from existing bank to SBI Max Gain. fill the application form, submit the necessary papers & SBI’s RACPC ‘ll do the back ground job.

Once SBI is ready to accept the transfer, it ‘ll issue you a sanction letter of the loan amount & ‘ll ask you to go for loan related agreement documentation work with SBI. If you are not having property insurance, SBI may ask to purchase one. Same ‘ll be the case for your life insurance. Once legal documentation is over, the cheque of the loan balance ‘ll be issued directly into the name of the bank in question. After the amount is credited to your existing bank, within next 20-30 days, you ‘ll get the original documents submitted by you, from the existing bank. Now you w’d have to submit these documents to SBI. In some states like Gujarat, Maharashtra, Karnataka, SBI may ask to go for registration of mortgage deed on your property in the office where your property was originally registered in your name.

|

SBI Max Gain |

Normal Home Loan |

|

Liquidity of your part prepayments is there |

No Liquidity. Money is gone for ever, once you prepay. |

|

A bit complex to understand |

Easy to understand |

|

For people who can generate regular surplus amounts |

For people who can only manage regular EMIs |

Source : http://goo.gl/5q11YV